Authored by the expert who managed and guided the team behind the Philippines Property Pack

Yes, the analysis of Manila's property market is included in our pack

Manila's property market presents both significant opportunities and notable risks as of September 2025. While luxury condos in prime business districts face oversupply and stagnating prices, smaller units in emerging areas are delivering strong rental yields of 6-8% and steady appreciation. The market shows clear segmentation, with certain property types and locations outperforming others substantially.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

Manila property prices range from PHP 80,000-300,000 per square meter depending on location and type, with luxury CBD condos showing recent declines while secondary areas maintain 6-8% annual growth.

The best investment opportunities currently lie in smaller condo units (studio to 1BR) in business districts and university areas, offering 6-8% rental yields compared to 4-5% in oversupplied luxury segments.

| Property Type | Average Price Range | Best Areas | Expected Returns |

|---|---|---|---|

| Luxury Condos | PHP 180,000-300,000/sqm | Makati, BGC, Ortigas | 5.0-7.0% rental yield |

| Mid-Range Condos | PHP 80,000-150,000/sqm | Quezon City, Pasig | 6.0-8.0% rental yield |

| Townhouses | PHP 25,000-120,000/sqm | Suburban areas | -3.4% price change (2024) |

| Single Houses | PHP 75,000-115,000/sqm | Outside CBDs | +12.8% price appreciation |

| Studio/1BR Units | PHP 2-6M total | Business districts | 7.0-9.0% rental yield |

| Investment Properties | PHP 80,000-150,000/sqm | Near transit/universities | 6.0-8.0% consistent returns |

| Bay Area Properties | Discounted pricing | Entertainment City | High vacancy risk |

How much does property in Manila cost right now by area and property type?

Manila property prices in September 2025 show significant variation based on location and property type, with luxury condos commanding the highest prices per square meter.

Luxury condos in prime business districts like Makati, BGC, and Ortigas average PHP 180,000-300,000 per square meter, with premium units exceeding PHP 300,000 per square meter. Mid-range condos in areas like Quezon City and Pasig are more affordable at PHP 80,000-150,000 per square meter.

Townhouses range from PHP 25,000-120,000 per square meter with total prices between PHP 792,000-44 million depending on size and location. Single-detached homes cost PHP 75,000-115,000 per square meter, with most units priced between PHP 3.5-27 million total.

The national average condo price stands at PHP 5.2 million or PHP 155,000 per square meter as of 2025. Top locations for price growth include Taguig (Bonifacio Global City), Makati, Ortigas, Quezon City, and emerging areas like Caloocan.

It's something we develop in our Philippines property pack.

How have prices changed in the last 3 to 5 years, and what's the short-term outlook?

Manila property prices have experienced steady growth over the past few years, with the nationwide price index rising 6.7% in 2024 and 7.6% in Q1 2025.

From 2021-2025, Manila has maintained consistent annual growth of 6-8%, though luxury CBD segments recently showed signs of cooling. Luxury condos in prime locations declined 0.7% year-over-year, while growth remains steady or accelerating in secondary and infrastructure-linked areas.

The short-term outlook for 2025-2026 shows modest to stable growth expected in Manila, with particularly strong performance anticipated in secondary (non-core) and infrastructure-linked locations. Luxury CBDs are experiencing growing market stability after recent softening.

Secondary markets and areas benefiting from new infrastructure development continue to show the strongest momentum, while established premium locations face maturity-related slowdown in appreciation rates.

What do most analysts expect for prices in the medium term (5 to 10 years)?

Analysts expect continued growth in Manila property prices over the next 5-10 years, but at a more moderate pace for established CBDs as they reach market maturity.

Manila CBDs like Makati and BGC are expected to see slower appreciation rates as they mature and reach price saturation points. However, emerging and infrastructure-rich zones are projected to experience quicker appreciation as connectivity improves and new business clusters develop.

The medium-term outlook heavily favors properties near new infrastructure projects, including MRT lines and subway developments. Areas connected to these transport improvements are expected to see the strongest value appreciation over the 5-10 year horizon.

Overall market fundamentals remain positive for Manila, with continued urbanization and economic development supporting steady demand, though growth rates will likely be more selective by location and property type compared to the broader growth of recent years.

How have rental yields been performing, and how do they compare across areas?

| Area | Average Rental Yield (1BR/2BR Condos) | Performance Notes |

|---|---|---|

| Metro Manila Average | 5.1-5.3% | Baseline market performance |

| Makati | 5.5-7.0% | Premium market, high demand |

| BGC (Taguig) | 5.0-6.5% | Expat and professional demand |

| Ortigas | 4.5-6.0% | Business district stability |

| Quezon City | 4.0-5.5% | Student and young professional market |

| Manila City | 4.0-5.0% | Traditional business center |

| Mandaluyong/San Juan | 7.0-9.0% | High yields for certain unit sizes |

Don't lose money on your property in Manila

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What is the average time it takes to resell a property in different parts of Manila?

The average resale time for properties in Metro Manila is currently 3-6 months for typical units.

Standard residential properties in established areas with good accessibility and proper pricing typically find buyers within this timeframe. Properties in high-demand locations like Makati and BGC often sell faster when priced competitively.

High-value properties and those in oversupplied areas, particularly luxury condos and Bay Area developments, can take much longer to resell. These properties may remain on the market for 6-12 months or longer due to limited buyer pools and market saturation.

Properties priced above market rates or in areas with high vacancy rates face extended selling periods, while well-located, reasonably-priced units in established neighborhoods maintain shorter resale timeframes.

Which areas are showing the strongest demand for residential living?

BGC (Taguig) and Makati continue to show the strongest residential demand, particularly from expats, professionals, and high-income Filipino families.

These prime business districts attract residents seeking proximity to work, premium amenities, and international-standard living environments. The concentration of multinational companies and high-paying jobs drives consistent demand for quality residential units.

Ortigas and Quezon City demonstrate robust demand from young professionals, students, and BPO workers, particularly for affordable studios and 1-bedroom units. These areas benefit from established business districts and educational institutions.

Caloocan and infrastructure-linked suburban areas are experiencing growing demand from both investors and owner-occupiers due to improving connectivity and more affordable pricing compared to traditional CBDs.

Which areas are attracting investors mainly for rental income?

Ortigas and Quezon City are attracting the most rental-focused investors due to better yields of 6-8% and lower entry costs compared to prime CBDs.

These areas offer attractive returns due to lower purchase prices combined with steady rental demand from the large tenant base of young professionals and students. The combination creates favorable yield calculations for investors.

University districts throughout Metro Manila consistently attract rental investors seeking high occupancy rates and steady 7-8% yields from student housing. These locations provide reliable long-term rental income.

BGC and Makati appeal to investors targeting premium rental markets, though higher entry prices result in lower net yields despite commanding premium rents. Bay Area properties present higher risk due to current high vacancy rates, but offer long-term potential if the market absorbs oversupply.

It's something we develop in our Philippines property pack.

Which property types—condos, townhouses, single houses—are performing best in terms of ROI?

Single detached and attached homes are currently delivering the strongest ROI with +12.8% appreciation in 2024, especially outside prime CBDs.

Duplex houses showed exceptional performance with +85.9% year-over-year growth, though this represents a small market segment with limited transaction volume. These properties benefit from scarcity and specific buyer demand.

Condos posted +5.1% growth in 2024, with smaller units in core locations generally offering the best ROI through rental yield optimization. Studio and 1-bedroom units consistently outperform larger units in terms of rental returns.

Townhouses are currently underperforming with -3.4% decline, indicating market challenges for this property type. The declining performance suggests oversupply or shifting buyer preferences in this segment.

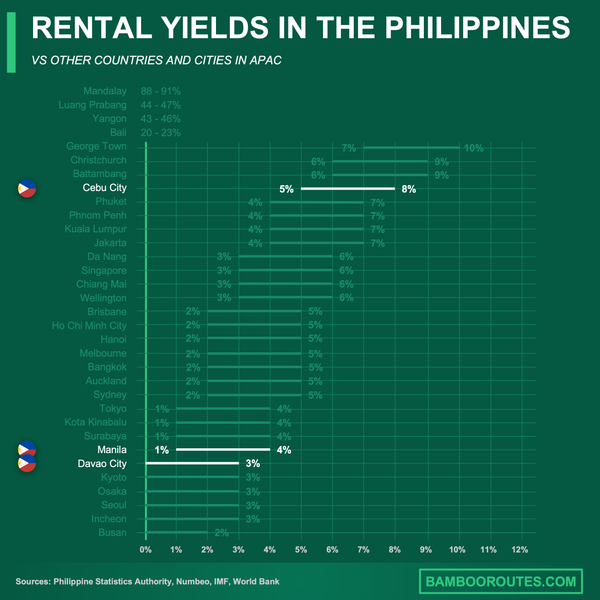

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

What are the risks or downsides of buying in Manila right now?

High vacancy rates present the most significant risk, with residential vacancy in Metro Manila projected at 26% in 2025 due to previous overbuilding.

Luxury and CBD condos face particular challenges with price stagnation or decline and ongoing oversupply risk. These premium segments have been most affected by market saturation and reduced foreign investment.

Bay Area properties continue experiencing high vacancies following the POGO exit, with potential for slow price and rent recovery. This area represents elevated risk for investors despite discounted entry prices.

High transaction costs of 8-10% combined with interest rate and regulatory risks create additional challenges. Possible volatility from changing economic policies and global economic conditions add uncertainty to investment returns.

If you want to buy mainly to live, which budget range and which locations make the most sense today?

A budget of PHP 5-15 million offers good options for mid-range condos in Quezon City, Pasig, Mandaluyong, or suburban settings that provide quality living at reasonable prices.

For owner-occupiers, location priorities should focus on access to workplaces, schools, and transportation networks rather than investment potential. Avoiding oversupplied luxury CBDs ensures better long-term living value.

Single detached houses or townhouses outside core CBDs provide more space and value for families, while condos offer better lifestyle amenities and convenience for professionals. The choice depends on family size and lifestyle preferences.

Areas with established infrastructure and community amenities offer the best long-term living satisfaction, even if they don't promise the highest investment returns.

If your goal is renting out, what kind of unit size, location, and budget are currently giving the best yields?

Studio or 1-bedroom units under 40 square meters near business hubs, universities, or transit lines deliver the highest rental yields.

A budget of PHP 80,000-150,000 per square meter for acquisition in inner city locations typically delivers 6-8% yields with good tenant demand. This price point offers optimal balance between entry cost and rental income potential.

Makati and BGC work well for premium rental markets targeting expat and executive tenants, while Ortigas, Mandaluyong, and Quezon City provide steady yields with high occupancy rates from local professionals.

Properties near new infrastructure corridors, particularly future MRT and subway lines, are likely to see the best value appreciation over 3-7 years while maintaining strong rental demand during development.

It's something we develop in our Philippines property pack.

If you're thinking about resale in the future, where should you position yourself now to maximize long-term gains?

Target emerging or redeveloping districts like Caloocan, infrastructure corridors, and secondary CBDs for the strongest long-term appreciation potential.

Focus on projects with master-planned amenities and those benefiting from upcoming infrastructure development. These locations offer the best combination of current affordability with future growth potential.

A 5-10 year investment timeframe aligns well with infrastructure completion cycles and new demand cluster maturation. This timing allows investors to benefit from development-driven appreciation.

Avoid heavily oversupplied, high-vacancy areas unless purchasing at significant discounts with a very long-term horizon. These areas require patience and deep market knowledge to time correctly.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

Manila's property market in September 2025 presents a tale of two markets: established luxury CBDs facing oversupply challenges while emerging areas and smaller units deliver strong returns.

The strongest opportunities lie in studio and 1-bedroom units in business districts, infrastructure-linked areas, and university zones, offering 6-8% rental yields with good appreciation potential.