Authored by the expert who managed and guided the team behind the Philippines Property Pack

Yes, the analysis of Manila's property market is included in our pack

Manila's property market is experiencing a transitional phase as of September 2025, with moderate price growth and evolving supply dynamics.

The capital city shows resilience amid economic headwinds, though investors should carefully evaluate market segments and timing. Rising construction costs and shifting buyer profiles are reshaping the landscape for both end-users and property investors.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

Manila's residential property market shows moderate growth with condo prices averaging ₱150,000 per sqm and house prices ranging ₱115,000-₱203,000 per sqm in central districts.

New supply is declining significantly with only 8,600 units expected in 2025 compared to historical averages of 13,000 annually, creating potential upward pressure on prices.

| Market Indicator | Current Status | Forecast Trend |

|---|---|---|

| Average Condo Price | ₱150,000/sqm | 5-7% annual growth |

| New Supply 2025 | 8,600 units | Declining to 2,500 by 2027 |

| Rental Yields | ~5% for condos | Stable to slightly improving |

| Vacancy Rate | 24.3% residential | Rising to 26% by end-2025 |

| GDP Growth | 5.5% projected 2025 | Sustained strong growth |

| Interest Rates | 5.25% policy rate | Potential further easing |

| Foreign Investment | Up to 40% of new units | Continued strong interest |

What are the current average prices per square meter for condos and houses in Manila?

As of September 2025, Manila's residential property market shows distinct pricing tiers across different property types and locations.

Condominium prices in Manila average ₱150,000 per square meter, with significant variation based on location. Manila City itself ranges from ₱90,000 to ₱140,000 per sqm, while premium areas like Makati and Bonifacio Global City command up to ₱364,000 per sqm for luxury developments.

House prices in Metro Manila typically range between ₱115,000 and ₱203,000 per square meter in central districts. The broader Philippines average sits around ₱75,000 per sqm, highlighting Manila's premium positioning within the national market.

Over the past 12 months, Metro Manila's overall residential prices have increased by 7.6% year-on-year as of Q1 2025. The National Capital Region, which includes Manila, has driven a 13.9% increase, though this growth rate has moderated compared to the previous year's more aggressive appreciation.

How many new residential units will be completed in Manila over the next few years?

Manila's new residential supply pipeline is experiencing a significant contraction compared to historical levels.

Approximately 8,600 new residential units are scheduled for completion in Metro Manila during 2025. This number drops to 6,200 units in 2026 and further declines to just 2,500 units in 2027.

This represents a dramatic decrease from the 2017-2019 average of 13,000 units completed annually. The current pipeline indicates a tightening supply scenario that could create upward pressure on property prices, particularly in high-demand segments.

Development delays have clustered most new completions between 2026 and 2027, creating an uneven distribution of new inventory. This supply constraint occurs against a backdrop of sustained demand, suggesting favorable conditions for property appreciation in the medium term.

It's something we develop in our Philippines property pack.

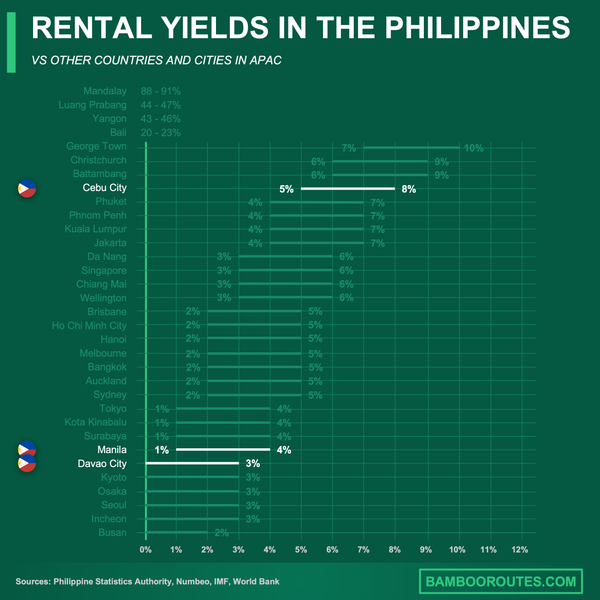

What are the current rental yields in Manila and how do they compare regionally?

Manila offers competitive rental yields that position it favorably within the Southeast Asian property investment landscape.

Current rental yields in Manila average around 5% for condominiums and similar residential properties. Smaller units typically achieve slightly higher yields due to stronger rental demand from young professionals and expatriates.

When compared to regional capitals, Manila's yields remain attractive. Bangkok also averages 4-6% rental yields in central districts, with some suburban areas achieving marginally higher returns. Jakarta presents a more varied picture, with yields ranging from 8-11% in select market niches, though these often come with higher risk profiles.

While Manila's yields are no longer distinctly superior to all peer cities, they offer a balanced risk-return profile that appeals to conservative investors. The stability of the Philippine peso and Manila's status as the economic center provide additional investment security compared to some regional alternatives.

What is the current transaction volume trend in Manila's property market?

Manila's property transaction volume has experienced a moderate decline from peak levels, reflecting broader market recalibration.

Recent data from property consultancies and central bank figures indicate that transaction counts and mortgage loan issuances in Metro Manila have softened slightly. This reflects increased buyer caution as property appreciation rates have moderated from previous highs.

The current volume sits below the five-year average, particularly when compared to the 2021-2022 pandemic recovery surge. However, the overall market maintains resilience, with net absorption in Q1 2025 showing modest improvement for high-demand segments.

This transaction volume decline represents a market normalization rather than distress, as buyers take more time to evaluate opportunities in the evolving price environment. Quality properties in prime locations continue to attract strong interest despite the overall volume reduction.

Don't lose money on your property in Manila

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What are the current occupancy rates for residential and commercial spaces?

Manila's occupancy rates reveal a market dealing with oversupply challenges, particularly in certain residential segments.

The current residential vacancy rate in Metro Manila stands at 24.3%, with projections indicating this could reach 26% by the end of 2025. This elevated vacancy rate is particularly pronounced in areas like the Bay Area, where vacancy rates can exceed 56.5% due to oversupply and slower-than-expected absorption.

Commercial occupancy rates, particularly in the office sector, continue to face challenges but have begun to stabilize. The National Capital Region's office market maintains elevated vacancy levels, though specific submarkets benefiting from BPO expansions and traditional tenant growth show improvement.

These occupancy challenges primarily affect newer developments in secondary locations, while prime central areas maintain healthier occupancy rates. Investors should focus on established neighborhoods with proven rental demand rather than speculative developments in emerging areas.

How much foreign investment is currently flowing into Manila's property market?

Foreign investment continues to play a significant role in Manila's property market, particularly in the condominium segment.

Foreign buyers account for up to 40% of units in new condominium developments, demonstrating sustained international interest in Manila real estate. This high foreign participation rate indicates the city's continued appeal as an investment destination.

The primary sources of foreign investment include East Asian countries, North America, and notably, Overseas Filipino Workers (OFWs) returning to invest in their homeland. While precise country-by-country flows remain opaque in public data, new-build presales consistently attract international buyers, especially for premium locations.

This foreign investment provides crucial market liquidity and price support, though it also means the market can be influenced by external economic conditions and currency fluctuations. The continued strong OFW remittances provide a stable foundation for sustained foreign investment flows.

What are the economic forecasts affecting property demand in Manila?

The Philippines' economic outlook for 2025 presents generally favorable conditions for Manila's property market.

GDP growth is expected to reach 5.5% in 2025, positioning the Philippines as the second-strongest performer in ASEAN. This robust economic expansion supports employment growth and income increases that drive housing demand.

Inflation forecasts range between 1.6% and 3.5% for 2025, remaining well within the government's target range. This controlled inflation environment supports real purchasing power and maintains property affordability for local buyers.

The central bank's policy interest rate currently sits at 5.25%, recently reduced to support economic recovery. Further modest easing remains possible if inflation stays contained, which would improve mortgage affordability and stimulate property demand.

These economic fundamentals create a supportive environment for property investment, with solid growth, manageable inflation, and accommodative monetary policy likely to sustain residential demand throughout 2025 and beyond.

How have construction costs impacted Manila's property prices?

Construction costs in Manila have risen moderately, creating measured pressure on new project pricing.

Average construction costs now stand at approximately ₱11,752 per square meter, representing an increase from the previous year but at a more modest pace compared to global construction cost surges experienced in other major cities.

These cost increases are gradually filtering into new project pricing, making resale and secondary market units relatively more attractive to cost-conscious buyers. The moderate cost inflation has prompted some developers to delay launches or adjust project specifications to maintain target price points.

The construction cost environment particularly constrains new affordable housing projects, potentially widening the gap between supply and demand in the entry-level market segment. Premium developments remain less affected due to their higher margin profiles.

It's something we develop in our Philippines property pack.

What is the current balance between end-users and investors in Manila?

Manila's buyer profile has shifted significantly toward end-user occupancy over recent years.

Previously, Manila's market skewed 50-60% investor-driven, with substantial participation from local speculators and overseas buyers seeking rental income or capital appreciation. However, post-pandemic demand patterns have fundamentally altered this balance.

Current market data indicates that end-users now represent more than 50% of new buyers for city core properties, particularly for move-in ready and mid-market units. This shift reflects increased demand for home-office flexibility and owner-occupation preferences.

The move toward end-user dominance provides market stability, as owner-occupiers are less likely to engage in speculative trading that can create price volatility. This buyer profile change supports sustained demand and reduces the risk of speculative bubbles in the residential market.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

What infrastructure projects are influencing Manila's property values?

Manila benefits from the Philippines government's "Build Better More" infrastructure initiative, which encompasses numerous high-impact projects across Metro Manila and surrounding regions.

| Project Type | Examples | Expected Completion |

|---|---|---|

| Transportation | New MRT lines, expressway extensions | 2026-2030 |

| Flood Protection | Metro Manila drainage systems | 2025-2028 |

| Airport Expansion | NAIA improvements, New Manila International Airport | 2027-2032 |

| Digital Infrastructure | 5G rollout, fiber networks | 2025-2027 |

| Commercial Hubs | New Binondo CBD, Pasig developments | 2026-2030 |

What is the forecasted supply-demand gap for housing in Manila?

Manila faces a significant housing shortage that will intensify over the remainder of the decade.

Nationwide forecasts project a gap of 6-7 million residential units by 2030 if current trends continue, with Metro Manila representing a substantial portion of this unmet demand. This shortage spans all market segments but is most acute in affordable and socialized housing categories.

Urbanization and migration pressures continue to drive population growth in Metro Manila faster than new housing supply can accommodate. The declining new unit pipeline through 2027 will exacerbate this supply-demand imbalance.

This structural shortage supports long-term property value appreciation, as fundamental housing demand will likely outpace supply additions. Investors focusing on affordable to mid-market segments may benefit most from this supply constraint environment.

What are the property price growth projections for Manila?

International agencies and local banks maintain cautiously optimistic forecasts for Manila property price appreciation.

| Forecast Period | Prime Areas Growth | Peripheral Districts |

|---|---|---|

| 1 Year (2025) | 4-7% annually | 3-5% annually |

| 3 Years (2025-2027) | 5-7% annually | 4-6% annually |

| 5 Years (2025-2029) | 5-7% annually | 4-6% annually |

Key drivers supporting these growth projections include infrastructure development, sustained foreign investment, and increasing demand for owner-occupation. However, oversupply in certain segments may limit upside potential in some areas.

The forecasts assume continued economic stability and successful infrastructure project implementation. Any significant changes in interest rates, foreign exchange rates, or regional economic conditions could alter these projections.

It's something we develop in our Philippines property pack.

How do current interest rates affect Manila property investment decisions?

The current interest rate environment in the Philippines provides moderate support for property investment activity.

The Bangko Sentral ng Pilipinas maintains the policy rate at 5.25%, recently reduced from higher levels to support economic recovery. This rate reduction improves mortgage affordability for local buyers while making leveraged property investments more attractive.

Further modest rate cuts remain possible if inflation continues within target ranges, which would provide additional stimulus to property demand. Lower rates reduce the cost of capital for developers and improve project feasibility for new launches.

For foreign investors, the rate environment affects currency carry considerations and relative yield attractiveness compared to other regional markets. The current rate level provides reasonable yield pickup over many developed market alternatives while maintaining relative stability.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

Manila's property market in September 2025 presents a mixed but generally positive outlook for investors and end-users.

The combination of declining new supply, moderate price appreciation, and supportive economic fundamentals creates opportunities for well-positioned property investments, though careful market segment selection remains crucial for success.

Sources

- Manila Average Condo Prices

- Average Price Condo Philippines

- Average House Price Philippines

- Philippine Real Estate Price Growth Analysis

- Property Price Growth Analysis - PhilStar

- JLL Q1 2025 Residential Manila Report

- Cities with Highest Rental Yields

- NCR Residential Vacancy Rate Forecast

- Philippines Interest Rate Data

- Philippine Economy Analysis 2025