Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Buying property as a foreigner in Central Luzon comes with specific rules that are different from many other countries, so understanding what you can and cannot own is essential before you start looking.

This guide covers property prices, ownership rules, visa requirements, mortgages, and taxes for foreign buyers in Central Luzon as of the first half of 2026.

We constantly update this blog post to reflect the latest regulations and market conditions in Central Luzon.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in Central Luzon.

Insights

- Foreigners can own condominium units in Central Luzon, but each condo project has a 40% foreign ownership cap, meaning some buildings in Clark or Angeles City may already be at capacity when you inquire.

- The Philippine Constitution prohibits foreigners from owning land directly, so house-and-lot packages in Bulacan or Pampanga subdivisions are off-limits unless you use a long-term lease structure.

- Long-term leases under the Investors' Lease Act allow foreigners to secure land use rights for up to 50 years with a possible renewal, which is the most common workaround for those wanting a house lifestyle in Central Luzon.

- Mortgage rates for foreigners in Central Luzon in 2026 typically range from 7% to 10% per year, with banks often requiring 30% to 50% down payment from non-resident buyers.

- Buyer closing costs in Central Luzon usually fall between 2.5% and 4.5% of the purchase price, with Documentary Stamp Tax at around 1.5% being the largest single component.

- Annual property tax in Central Luzon provinces is commonly around 2% of assessed value (basic RPT plus Special Education Fund), but since assessed value is lower than market value, expect to budget roughly 0.3% to 0.8% of market value per year.

- Rental income from Central Luzon properties is taxed at a flat 25% on gross for nonresident aliens not engaged in trade or business, making tax planning essential before you buy to rent out.

- The BSP policy rate dropped to 4.5% in December 2025, which has started to ease mortgage pricing slightly, though foreigner rates remain higher due to additional risk adjustments by Philippine banks.

- Clark, Angeles City, and Mabalacat in Pampanga have the highest concentration of condo developments in Central Luzon, making them the primary spots where foreigners can actually buy property in their own name.

What can I legally buy and truly own as a foreigner in Central Luzon?

What property types can foreigners legally buy in Central Luzon right now?

As of early 2026, the only residential property type a foreigner can legally buy and own outright in Central Luzon is a condominium unit, because the Philippine Constitution restricts foreign ownership of land.

The most important limitation is that each condo project in Central Luzon has a 40% cap on foreign ownership, so even if you qualify personally, the specific building you want might already be at its limit.

This means if you are interested in a house-and-lot, townhouse, or vacant residential lot in places like Bulacan, Pampanga, or Bataan, you cannot put the title in your own name as a foreigner.

However, you can still enjoy a house lifestyle in Central Luzon by entering a long-term lease agreement under the Investors' Lease Act, which allows leases of up to 50 years with a possible renewal, giving you use rights without actual land ownership.

Finally, please note that our pack about the property market in Central Luzon is specifically tailored to foreigners.

Can I own land in my own name in Central Luzon right now?

No, as a foreign individual you generally cannot own land in your own name anywhere in Central Luzon because the Philippine Constitution restricts the transfer of private land to qualified Filipinos and certain Philippine entities.

The most clearly legal alternative is a long-term lease under the Investors' Lease Act, which lets you secure use rights to land (including a house on it) for up to 50 years with a renewal option, though you never actually own the land itself.

Some foreigners try to work around the land ban by putting the title in a Filipino partner's or friend's name, but Philippine courts have repeatedly struck down these "nominee" arrangements as unconstitutional, meaning you could lose the property entirely with no legal recourse.

By the way, we cover everything there is to know about the land buying process in Central Luzon here.

As of 2026, what other key foreign-ownership rules or limits should I know in Central Luzon?

As of early 2026, one rule that often catches buyers off guard in Central Luzon is that the 40% foreign ownership cap applies at the project level, not nationally, so you must confirm quota availability with the specific condo corporation or developer before paying anything.

For condos specifically, this quota rule means that even a brand-new development in Clark or Angeles City could run out of foreign-eligible units quickly if the project is popular with overseas buyers.

There is no special government approval or registration requirement just for being foreign when buying a condo in Central Luzon, but you will need a Philippine Tax Identification Number (TIN) for tax payments and title transfer documentation.

As for recent regulatory changes, there have been no major new laws altering the foreign ownership framework in Central Luzon in 2026, though you should always verify developer licensing and DHSUD registration, especially for preselling projects in fast-growing areas like Mabalacat.

What's the biggest ownership mistake foreigners make in Central Luzon right now?

The single biggest ownership mistake foreigners make in Central Luzon is trying to bypass the land ban by using a "nominee" arrangement, where a Filipino friend or partner holds the title while you pay for and control the property.

If you go this route, the likely consequence is that Philippine courts will treat the arrangement as void and unenforceable, meaning you could lose the entire property and have almost no legal way to recover your money.

Other classic pitfalls in Central Luzon include not verifying that a condo's foreign quota still has room before paying a reservation fee, skipping a Certified True Copy title check through the Land Registration Authority, and assuming that special economic zones like Clark allow foreign land ownership when they actually do not.

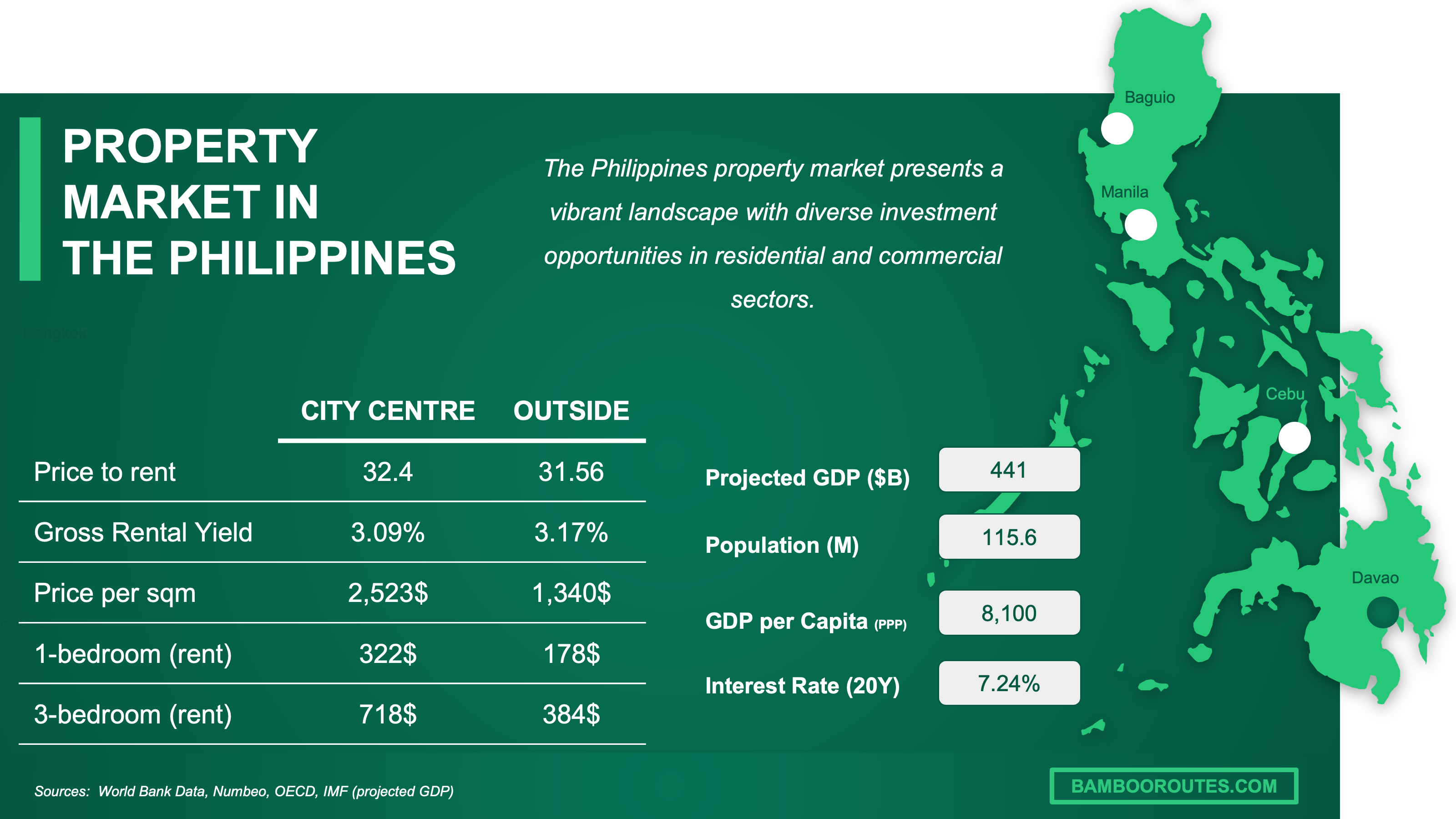

We have made this infographic to give you a quick and clear snapshot of the property market in the Philippines. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Which visa or residency status changes what I can do in Central Luzon?

Do I need a specific visa to buy property in Central Luzon right now?

For a straightforward condo purchase in Central Luzon, you do not legally need a specific long-stay visa, and you can typically transact even if you entered the Philippines on a tourist visa.

However, the most common administrative hurdle for buyers without local residency is that banks, developers, and the Registry of Deeds often require stronger documentation, and if you want a mortgage, banks will usually ask for residency-style paperwork.

You will very often need a Philippine Tax Identification Number (TIN) at some point during the transaction, especially when paying Documentary Stamp Tax or registering the title transfer, so it is smart to apply for one early.

A typical document set for a foreign buyer in Central Luzon includes your passport, TIN, proof of income or funds, and sometimes an Alien Certificate of Registration if you are a long-stay resident.

Does buying property help me get residency and citizenship in Central Luzon in 2026?

As of early 2026, buying property in Central Luzon does not automatically help you get residency or citizenship because the Philippines is not a "buy property, get a visa" country.

Instead, realistic long-stay options are program-based, such as the Special Resident Retiree's Visa (SRRV) through the Philippine Retirement Authority, which requires a deposit but is not directly tied to buying a home.

Another option is the Special Investor's Resident Visa (SIRV), which requires a minimum investment of around $75,000 in qualifying activities, but again this is an investment program, not a property purchase pathway, and citizenship is an entirely separate legal process that takes many years.

We give you all the details you need about the different pathways to get residency and citizenship in Central Luzon here.

Can I legally rent out property on my visa in Central Luzon right now?

Your visa status generally does not prevent you from legally renting out a condo you own in Central Luzon, but you must treat rental income as a real tax and compliance activity with the Bureau of Internal Revenue.

You do not need to live in the Philippines to rent out your property, and many foreign owners manage their Central Luzon condos remotely through a local property manager.

The key thing to know is that rental income from Philippine property is taxed in the Philippines, and if you are classified as a nonresident alien not engaged in trade or business, expect a flat 25% tax on your gross rental income, plus you should check whether your condo's house rules allow short-term rentals before you buy.

We cover everything there is to know about buying and renting out in Central Luzon here.

Get fresh and reliable information about the market in Central Luzon

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.

How does the buying process actually work step-by-step in Central Luzon?

What are the exact steps to buy property in Central Luzon right now?

The standard sequence to buy a condo in Central Luzon is: pick your unit and confirm foreign quota availability, do due diligence on the title, sign the contract (reservation agreement or deed of sale), pay required taxes, get BIR transfer clearance (eCAR), pay local transfer tax, register at the Registry of Deeds, and then update the tax declaration for annual property tax.

You do not have to be physically present for every step since you can use a Special Power of Attorney to authorize someone to sign on your behalf, but many buyers choose to be in Central Luzon for signing and handover to reduce fraud risk.

The step that typically makes the deal legally binding is signing the notarized Deed of Absolute Sale, which is the document that transfers ownership and gets registered with the Registry of Deeds.

From accepted offer to final title registration in Central Luzon, the typical end-to-end timeline is around 2 to 4 months, though delays at the BIR or Registry of Deeds can extend this.

We have a document entirely dedicated to the whole buying process our pack about properties in Central Luzon.

Is it mandatory to get a lawyer or a notary to buy a property in Central Luzon right now?

A notary is effectively mandatory in Central Luzon because the Deed of Absolute Sale must be notarized to be registrable with the Registry of Deeds, but hiring a separate lawyer is not strictly required by law.

The key difference is that a notary in the Philippines authenticates signatures and makes the document legally usable, while a lawyer reviews the contract terms, checks the title, and protects your interests throughout the deal.

If you do hire a lawyer for your Central Luzon purchase, make sure their engagement scope explicitly includes verifying the title through the LRA, reviewing all contract clauses, and coordinating the BIR and Registry of Deeds filings.

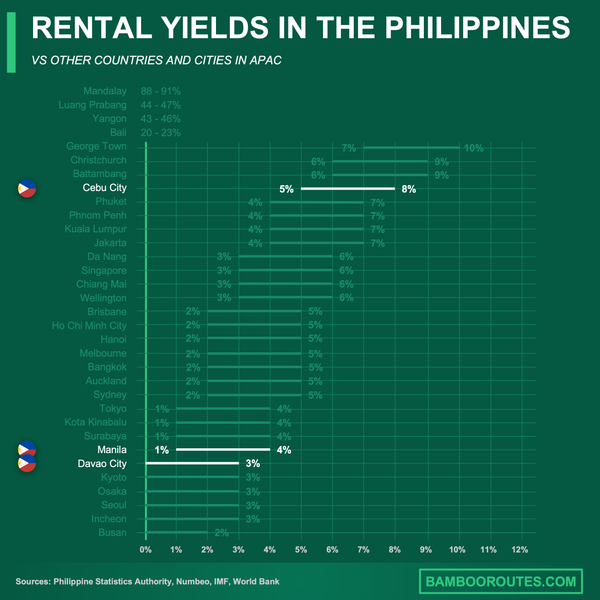

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

What checks should I run so I don't buy a problem property in Central Luzon?

How do I verify title and ownership history in Central Luzon right now?

The official registry you should use to verify title and ownership history in Central Luzon is the Land Registration Authority, and the easiest way to access it is through the LRA eSerbisyo online portal.

The key document to request is a Certified True Copy (CTC) of the title, which shows the registered owner, the technical description of the property, and any annotations like mortgages or court orders.

A realistic look-back period that buyers commonly use in Central Luzon is 10 to 15 years of ownership history, which helps you spot unusual transfers or potential disputes.

One clear red-flag finding that should stop or pause your purchase is any annotation showing an adverse claim, a lis pendens (pending lawsuit), or an unpaid mortgage, because these could mean someone else has a legal interest in the property.

You will find here the list of classic mistakes people make when buying a property in Central Luzon.

How do I confirm there are no liens in Central Luzon right now?

The standard way to confirm there are no liens or encumbrances on a property in Central Luzon is to request a Certified True Copy of the title from the LRA, then carefully review the annotations section on the back of the title.

One common type of lien you should specifically ask about is an existing bank mortgage, because if the seller has not fully paid off their loan, that mortgage stays attached to the property even after you buy it.

The single best written proof of lien status is the annotations section of the Certified True Copy itself, combined with a tax clearance from the local government unit showing that real property taxes are fully paid.

How do I check zoning and permitted use in Central Luzon right now?

The authority you should use to check zoning and permitted use for a property in Central Luzon is the city or municipal planning office of the local government unit where the property is located.

The document that typically confirms zoning classification is the Zoning Certificate or Locational Clearance issued by the planning office, which shows what land uses are allowed on that specific lot.

One common pitfall that foreign buyers miss in Central Luzon is assuming that all condos allow short-term rentals, when in fact many condo corporations in places like Angeles City or Clark have house rules that restrict or ban Airbnb-style rentals.

Buying real estate in Central Luzon can be risky

An increasing number of foreign investors are showing interest. However, 90% of them will make mistakes. Avoid the pitfalls with our comprehensive guide.

Can I get a mortgage as a foreigner in Central Luzon, and on what terms?

Do banks lend to foreigners for homes in Central Luzon in 2026?

As of early 2026, yes, some Philippine banks do lend to foreigners for home purchases in Central Luzon, but lending is more selective and comes with stricter terms than what Filipino citizens receive.

The realistic loan-to-value range that foreign borrowers commonly see in Central Luzon is between 50% and 70%, meaning you should expect to put down at least 30% to 50% of the purchase price as a down payment.

The single most common eligibility requirement is that banks prefer foreigners who have local residency, stable Philippine-sourced income, or are married to a Filipino, because relying solely on overseas income makes approval much harder.

You can also read our latest update about mortgage and interest rates in The Philippines.

Which banks are most foreigner-friendly in Central Luzon in 2026?

As of early 2026, the three most foreigner-friendly banks for mortgages in Central Luzon are BDO, BPI, and Metrobank, because they have the largest branch networks, established housing loan products, and experience processing foreign buyer applications.

What makes these banks more foreigner-friendly is their willingness to consider applications from resident foreigners with documented income, and their branches in Pampanga (especially around Clark and Angeles City) are accustomed to handling overseas buyer paperwork.

However, these banks are generally reluctant to lend to pure non-residents who have no Philippine ties, so if you do not have local residency, local income, or a Filipino spouse, getting approved will be significantly harder.

We actually have a specific document about how to get a mortgage as a foreigner in our pack covering real estate in Central Luzon.

What mortgage rates are foreigners offered in Central Luzon in 2026?

As of early 2026, the typical mortgage interest rate range for foreigners in Central Luzon is around 7% to 10% per year, with most loans offering a fixed rate for the first 1 to 5 years before repricing.

Fixed-rate mortgages in Central Luzon usually start slightly lower (around 7% to 8% for shorter fixing periods) but then reprice based on the bank's prevailing rates, while fully variable rates are less common and tend to start higher due to uncertainty, so most foreign buyers choose a 3-year or 5-year fixed period for predictability.

We made this infographic to show you how property prices in the Philippines compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What will taxes, fees, and ongoing costs look like in Central Luzon?

What are the total closing costs as a percent in Central Luzon in 2026?

For a buyer in Central Luzon in 2026, the typical total closing costs run between 2.5% and 4.5% of the purchase price, depending on the deal structure and whether you add lawyer fees or rush processing charges.

The realistic low-to-high range covers most standard transactions: simpler deals with cooperative sellers land near 2.5%, while more complex purchases or those in cities with higher local transfer tax rates can push past 4%.

The specific fee categories that make up closing costs in Central Luzon include Documentary Stamp Tax (around 1.5%), local transfer tax (0.5% to 0.75% depending on whether you are in a province or city), registration fees, and notarial costs.

The single biggest contributor to closing costs is usually the Documentary Stamp Tax at around 1.5% of the purchase price, which is a national tax collected by the BIR.

If you want to go into more details, we also have a blog article detailing all the property taxes and fees in Central Luzon.

What annual property tax should I budget in Central Luzon in 2026?

As of early 2026, a practical annual property tax budget for a standard home in Central Luzon is roughly 0.3% to 0.8% of the property's market value, which for a condo worth PHP 5 million (around $90,000 or EUR 82,000) means about PHP 15,000 to PHP 40,000 per year.

Property tax in Central Luzon is assessed on the property's assessed value (not market value), with the basic Real Property Tax commonly around 1% of assessed value plus an additional 1% Special Education Fund levy, but since assessed values are typically much lower than market values, the effective rate as a percentage of what you paid is lower.

How is rental income taxed for foreigners in Central Luzon in 2026?

As of early 2026, if you are classified as a nonresident alien not engaged in trade or business in the Philippines, your rental income from Central Luzon property is typically taxed at a flat 25% on gross rental receipts, though your specific classification and any applicable tax treaties could change the outcome.

The basic requirement is that your tenant or property manager withholds this tax and remits it to the BIR on your behalf, and you should get documentation of these withholdings for your records and any foreign tax credit claims in your home country.

What insurance is common and how much in Central Luzon in 2026?

As of early 2026, a typical annual insurance premium for a condo unit in Central Luzon ranges from about PHP 5,000 to PHP 15,000 (roughly $90 to $270 or EUR 80 to EUR 245), depending on coverage level and the value of your unit and contents.

The most common type of property insurance coverage that condo owners carry in Central Luzon is fire insurance, which is often required by the condo corporation, and many owners add typhoon and flood riders given the region's weather exposure.

The single biggest factor that makes insurance premiums higher or lower for the same property type in Central Luzon is the location's flood and typhoon risk, so a condo in a flood-prone barangay near rivers in Bulacan will cost more to insure than one on higher ground in Pampanga.

Get the full checklist for your due diligence in Central Luzon

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about Central Luzon, we always rely on the strongest methodology we can … and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source Name | Why It's Authoritative | How We Used It |

|---|---|---|

| Supreme Court E-Library (1987 Constitution) | This is the primary constitutional text published by the judiciary's official library. | We used it to anchor the non-negotiable rule that foreigners generally cannot own private land. We also used it to explain why nominee arrangements are risky and often void. |

| Lawphil (Condominium Act RA 4726) | Lawphil is a widely used legal reference that publishes full statute text. | We used it to define what a condo legally is and what you actually own. We also used it as the legal base for foreign condo ownership subject to constitutional limits. |

| Lawphil (Investors' Lease Act RA 7652) | This is the statute text for long-term leases and a core reference for foreigner land use. | We used it to explain the practical alternative to land ownership through long leases up to 50 years. We also used it to set expectations on what leasing does and does not do. |

| Philippine Retirement Authority (SRRV) | This is the official government program page for the retiree visa pathway. | We used it to describe one realistic long-stay residency option. We also clarified that residency options affect your ability to live in Central Luzon, not the land ownership rules. |

| BOI (SIRV FAQ) | BOI is the administering authority for SIRV endorsements, making this the source of truth. | We used it to summarize investor residency basics including the minimum investment figure. We also explicitly separated investor visa from property ownership rights. |

| Bangko Sentral ng Pilipinas (Key Rates) | This is the central bank's official publication of benchmark policy rates. | We used it to contextualize mortgage pricing in January 2026. We also used it to justify why Philippine mortgage rates tend to be higher than in the US or EU. |

| Reuters (BSP December 2025 Rate Cut) | Reuters is a top-tier wire service and reliable for dated monetary policy events. | We used it to pin the January 2026 interest rate backdrop with a concrete recent datapoint. We cross-checked it against BSP's own Key Rates page for consistency. |

| Land Registration Authority (eSerbisyo Portal) | This is the official portal for requesting Certified True Copies of titles. | We used it to explain how buyers verify title authenticity without relying on seller photocopies. We also included it as the safest first due diligence step before paying anything. |

| LRA (Certified True Copy Guide) | It is an official user guide that describes the process and scope of the LRA online service. | We used it to give step-by-step instructions for requesting a CTC. We also used it to set expectations on what a CTC can reveal about ownership and encumbrances. |

| BIR (Documentary Stamp Tax) | BIR is the tax authority, so it is the definitive reference for DST as a tax type. | We used it to frame DST as a standard non-optional closing cost in transfers. We then triangulated the practical DST rate with legal and tax practitioner references. |

| DOF-BLGF (RPT/SEF Notices) | BLGF sits under DOF and deals directly with local finance and real property taxation. | We used it to confirm how LGUs communicate real property tax and SEF tax obligations. We also used it to reinforce that RPT is locally administered and varies by LGU in Central Luzon. |

| BDO (Home Loan Interest Rate Card) | This is the bank's own published rate card document, so it is primary-source pricing. | We used it to ground our January 2026 mortgage rate range with an actual major bank schedule. We then translated that into what a foreign borrower is likely to see after risk adjustments. |

| Security Bank (Home Loan Promo) | This is a bank's official product promo page, so it is verifiable and dated. | We used it as a cross-check that sub-7% fixed rates existed recently with conditions. We also explained that promos are time-bound and not the same as standard foreigner pricing. |

| Metrobank (Loan Rates and Fees) | It is the bank's official disclosure page for consumer loan fees and rates information. | We used it to support the discussion of bank fees and pricing mechanics around housing loans. We also used it to remind buyers to budget for bank charges beyond interest. |

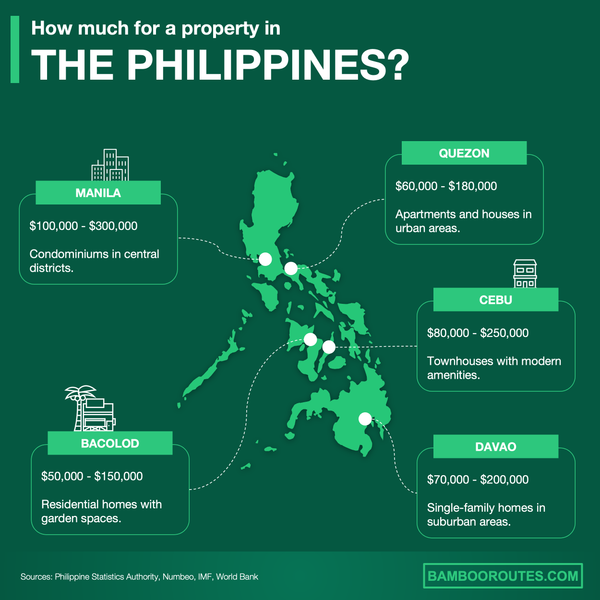

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of the Philippines. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

Related blog posts

- Is now a good time to invest in property in Central Luzon?