Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Whether you are eyeing a condominium in Angeles City near Clark or exploring opportunities in Bulacan, understanding the real costs of buying property in Central Luzon as a foreigner is essential before you commit.

This guide breaks down every tax, fee, and hidden cost you will face in early 2026, so you can budget accurately and avoid surprises.

We constantly update this blog post to reflect the latest regulations and market conditions in Central Luzon.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in Central Luzon.

Overall, how much extra should I budget on top of the purchase price in Central Luzon in 2026?

How much are total buyer closing costs in Central Luzon in 2026?

As of early 2026, total buyer closing costs in Central Luzon typically range from 2% to 8% of the purchase price, which on a PHP 5,000,000 property (about USD 87,000 or EUR 80,000) means you should prepare between PHP 100,000 and PHP 400,000 (USD 1,750 to USD 7,000 or EUR 1,600 to EUR 6,400) in additional funds.

If you keep expenses to the bare legal minimum in Central Luzon and the seller pays the major seller-side taxes, you can get by with roughly 1.5% to 3% extra, meaning around PHP 75,000 to PHP 150,000 (USD 1,300 to USD 2,600 or EUR 1,200 to EUR 2,400) on a PHP 5,000,000 purchase.

However, if you hire your own lawyer, need translation services, pay for comprehensive due diligence, or negotiate to cover some seller-side costs, your closing costs in Central Luzon can climb to 10% to 14% of the purchase price, potentially reaching PHP 500,000 to PHP 700,000 (USD 8,700 to USD 12,200 or EUR 8,000 to EUR 11,200) on the same property.

The main factors that determine whether your Central Luzon closing costs fall at the low or high end include which local government unit (LGU) the property is in (Angeles City has different rates than rural Tarlac), whether the contract shifts any seller taxes to you, and how much professional help you engage for legal verification and document handling.

What's the usual total % of fees and taxes over the purchase price in Central Luzon?

The usual total percentage of fees and taxes over the purchase price in Central Luzon sits around 2% to 4% for buyers when the seller handles Capital Gains Tax, which is the standard market convention in the Philippines.

The realistic range that covers most standard residential property transactions in Central Luzon spans from 1.5% on the low end (minimal services, low-transfer-tax municipality) to about 8% on the high end (full professional support, higher-rate city, and Documentary Stamp Tax shifted to buyer).

Of that total, government taxes typically account for about 60% to 70% (transfer tax around 0.5% to 0.75%, Documentary Stamp Tax around 1.5% if buyer pays, plus registration fees), while professional service fees like notary, lawyer, and due diligence make up the remaining 30% to 40%.

By the way, you will find much more detailed data in our property pack covering the real estate market in Central Luzon.

What costs are always mandatory when buying in Central Luzon in 2026?

As of early 2026, the mandatory costs you cannot avoid when buying property in Central Luzon include the local transfer tax (paid to the LGU treasurer), Registry of Deeds registration fees, notarization of the deed of sale, and certified document costs like tax declarations and title copies.

Costs that are optional but highly recommended for foreign buyers in Central Luzon include hiring an independent conveyancing lawyer to verify the title chain and check for liens, conducting full due diligence at the Registry of Deeds, engaging a translator if you are not comfortable with Filipino or legal English, and getting a professional property valuation if you are negotiating in fast-moving areas like Clark or Angeles City.

Don't lose money on your property in Central Luzon

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What taxes do I pay when buying a property in Central Luzon in 2026?

What is the property transfer tax rate in Central Luzon in 2026?

As of early 2026, the property transfer tax rate in Central Luzon ranges from 0.5% to 0.75% of the tax base (whichever is higher between contract price and government reference values), depending on which city or municipality the property is located in.

There is generally no extra transfer tax specifically for foreigners in Central Luzon because the transfer tax is tied to the property transaction itself, not the buyer's nationality, under the Local Government Code framework.

Buyers may pay 12% VAT on residential property purchases in Central Luzon if the selling price exceeds PHP 3,600,000 and the seller is VAT-registered (typically developers or businesses), though sales below this threshold are VAT-exempt under BIR Revenue Regulations 1-2024.

Documentary Stamp Tax, which functions like a stamp duty in Central Luzon, is calculated at PHP 15 per PHP 1,000 of the tax base (approximately 1.5%) and is typically paid during BIR processing to obtain the certificate authorizing registration.

Are there tax exemptions or reduced rates for first-time buyers in Central Luzon?

There is no standard nationwide first-time buyer tax exemption or reduced rate in Central Luzon as of early 2026, though all buyers benefit from VAT exemption on residential properties priced at PHP 3,600,000 or below regardless of whether it is their first purchase.

If you buy property through a company in Central Luzon, the transaction may trigger different withholding and income tax mechanics depending on asset classification, and you will face higher compliance costs for accounting and tax advisory services.

There is often a tax difference between buying new-build versus resale properties in Central Luzon because developer sales above the PHP 3,600,000 threshold are more likely to attract VAT, while resales between private individuals are typically handled under Capital Gains Tax and Documentary Stamp Tax rules.

Since there is no formal first-time buyer program in Central Luzon, no specific documentation or conditions are required to qualify for such exemptions, though you should always confirm VAT-inclusive pricing in writing when purchasing from developers.

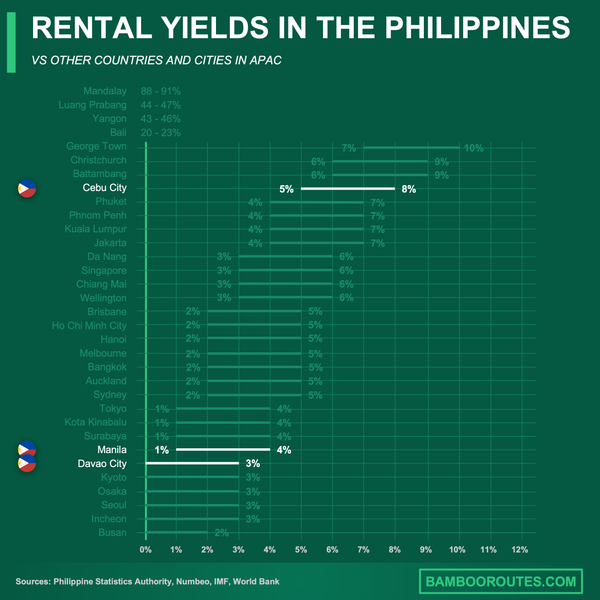

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

Which professional fees will I pay as a buyer in Central Luzon in 2026?

How much does a notary or conveyancing lawyer cost in Central Luzon in 2026?

As of early 2026, notary fees combined with basic document handling in Central Luzon typically cost between PHP 10,000 and PHP 50,000 (USD 175 to USD 875 or EUR 160 to EUR 800), while an independent conveyancing lawyer recommended for foreigners can charge PHP 50,000 to PHP 200,000 (USD 875 to USD 3,500 or EUR 800 to EUR 3,200) depending on transaction complexity.

Notary and lawyer fees in Central Luzon are typically charged as a flat rate or a combined service fee rather than as a strict percentage of the property price, though complex deals involving corporate sellers, inheritance titles, or lien issues will cost more.

Translation or interpreter services for foreign buyers in Central Luzon generally cost PHP 2,000 to PHP 8,000 (USD 35 to USD 140 or EUR 32 to EUR 128) per session, with certified document translations running PHP 1,500 to PHP 5,000 (USD 26 to USD 87 or EUR 24 to EUR 80) depending on length and urgency.

A tax advisor is not strictly necessary for straightforward condo purchases in Central Luzon, but if you are structuring anything unusual like a leasehold arrangement or corporate buyer, expect to budget PHP 20,000 to PHP 100,000 (USD 350 to USD 1,750 or EUR 320 to EUR 1,600) for professional tax advice.

We have a whole part dedicated to these topics in our our real estate pack about Central Luzon.

What's the typical real estate agent fee in Central Luzon in 2026?

As of early 2026, the typical real estate agent fee in Central Luzon ranges from 3% to 5% of the sale price, which on a PHP 5,000,000 property translates to PHP 150,000 to PHP 250,000 (USD 2,600 to USD 4,400 or EUR 2,400 to EUR 4,000).

In most Central Luzon transactions, the seller pays the listing broker's commission, though if you hire your own buyer's agent you may pay separately or the commission may be built into the negotiated price.

The realistic range for agent fees in Central Luzon spans from 3% (common for straightforward deals or when both parties share one agent) to 5% or occasionally higher for premium properties or extensive buyer representation services.

How much do legal checks cost (title, liens, permits) in Central Luzon?

Legal checks including title search, liens verification, and permits review in Central Luzon typically cost PHP 5,000 to PHP 30,000 (USD 87 to USD 525 or EUR 80 to EUR 480) for hard document costs and certifications, with higher fees if you need multiple trips to offices or historical title tracing.

A property valuation fee in Central Luzon usually costs PHP 5,000 to PHP 25,000 (USD 87 to USD 440 or EUR 80 to EUR 400), with bank-grade appraisals for financing purposes sitting at the higher end of that range.

The most critical legal check you should never skip in Central Luzon is the title verification at the Registry of Deeds to confirm the seller actually owns the property, that there are no liens or encumbrances, and that the title is not fake or contested.

Buying a property with hidden issues is something we mention in our list of risks and pitfalls people face when buying real estate in Central Luzon.

Get the full checklist for your due diligence in Central Luzon

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.

What hidden or surprise costs should I watch for in Central Luzon right now?

What are the most common unexpected fees buyers discover in Central Luzon?

The most common unexpected fees buyers discover in Central Luzon include condo association dues and special assessments (often PHP 50 to PHP 150 per square meter monthly in Clark or Angeles City towers), unpaid association arrears that block clearance, move-in charges, elevator reservation fees, renovation bonds, and document re-signing costs if signatures do not match registry expectations.

Yes, you can inherit unpaid property taxes or debts when purchasing in Central Luzon if you do not verify Real Property Tax (RPT) clearance and tax declaration status at the local treasurer and assessor offices before closing.

Buyers do get scammed with fake listings or fake fees in Central Luzon, typically through reservation fee requests to personal accounts without proper documentation or fake "processing fees" supposedly required by government offices, so you should always pay official taxes only to authorized government cashiers and demand receipts.

Fees that are usually not disclosed upfront by sellers or agents in Central Luzon include the full condo dues and special assessments, the real transfer and registration cost when computed on the "higher of" value basis, and extra costs for foreign document handling like apostilles and Special Powers of Attorney.

In our property pack covering the property buying process in Central Luzon, we go into details so you can avoid these pitfalls.

Are there extra fees if the property has a tenant in Central Luzon?

If the property has a tenant in Central Luzon, you may face extra costs of PHP 5,000 to PHP 20,000 (USD 87 to USD 350 or EUR 80 to EUR 320) for legal notices, lease assignment paperwork, and clear agreements on security deposit handling, plus potential delayed possession costs while you wait to occupy.

When purchasing a tenanted property in Central Luzon, the buyer typically inherits the existing lease agreement and must honor its terms until expiration, including the obligation to respect the tenant's right to occupy and the proper handling of any security deposits.

It is generally not possible to terminate an existing lease immediately after purchase in Central Luzon unless the lease contract has a specific clause allowing early termination, the tenant agrees to leave voluntarily, or there are valid legal grounds for eviction under Philippine tenancy law.

A sitting tenant in Central Luzon typically weakens your negotiating position because many buyers prefer vacant possession, though investors specifically seeking rental income may view an existing tenant as an advantage that reduces vacancy risk.

If you want to optimize your rental strategy, you can read our complete guide on how to buy and rent out in Central Luzon.

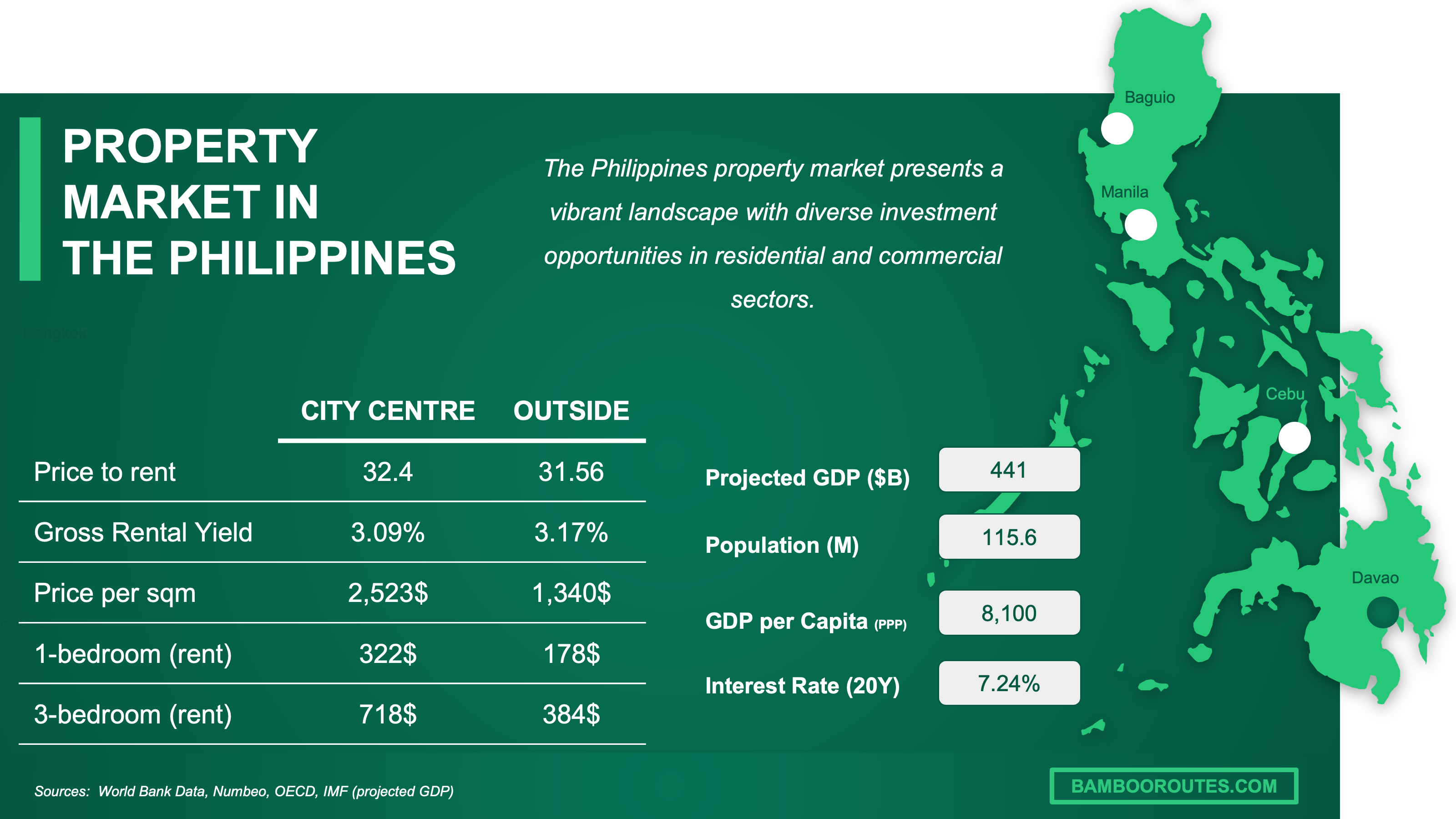

We have made this infographic to give you a quick and clear snapshot of the property market in the Philippines. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Which fees are negotiable, and who really pays what in Central Luzon?

Which closing costs are negotiable in Central Luzon right now?

The closing costs that are negotiable in Central Luzon include who pays the Documentary Stamp Tax (around 1.5%), who pays the Capital Gains Tax (6%, normally the seller but often negotiated), notary and legal fees, and the agent commission split between parties.

Closing costs that are fixed by law or regulation and cannot be negotiated in Central Luzon include the transfer tax rate itself (set by LGU ordinance within legal ceilings) and Registry of Deeds registration fees (based on official schedules), though you can still negotiate which party pays these fixed amounts.

Typical discounts or reductions buyers can realistically achieve on negotiable fees in Central Luzon range from 10% to 30% on professional service fees like notary and legal costs, while tax-related negotiations usually involve shifting the burden rather than reducing the rate.

Can I ask the seller to cover some closing costs in Central Luzon?

Yes, you can ask the seller to cover some closing costs in Central Luzon, and in a balanced market there is roughly a 40% to 60% chance the seller will agree to negotiate on items like DST or even CGT if you structure it correctly in the contract.

The specific closing costs sellers are most commonly willing to cover in Central Luzon are Capital Gains Tax (which is technically their obligation anyway), Documentary Stamp Tax, and sometimes a portion of the agent commission if they are motivated to close quickly.

Sellers in Central Luzon are more likely to accept covering closing costs when the market is slow, the property has been listed for a long time, the unit needs repairs, or the paperwork is messy and they want a clean exit.

Is price bargaining common in Central Luzon in 2026?

As of early 2026, price bargaining is common and expected in Central Luzon's resale market, with most sellers anticipating some negotiation, though new developments from major builders tend to have firmer pricing with less room to bargain on the base price.

Buyers in Central Luzon typically negotiate 3% to 10% below the asking price on resale properties (PHP 150,000 to PHP 500,000 off a PHP 5,000,000 listing, or USD 2,600 to USD 8,700 / EUR 2,400 to EUR 8,000), with higher discounts possible when sellers are motivated or properties need work, while hot inventory in Clark or Angeles City may only yield 0% to 5% off.

Don't sign a document you don't understand in Central Luzon

Buying a property over there? We have reviewed all the documents you need to know. Stay out of trouble - grab our comprehensive guide.

What monthly, quarterly or annual costs will I pay as an owner in Central Luzon?

What's the realistic monthly owner budget in Central Luzon right now?

A realistic monthly owner budget in Central Luzon for a typical condominium ranges from PHP 8,000 to PHP 25,000 (USD 140 to USD 440 or EUR 128 to EUR 400) covering association dues, utilities, and basic maintenance, with higher-end Clark or Angeles City towers pushing toward the upper range.

The main recurring expense categories that make up this monthly budget in Central Luzon include condominium association dues (often the largest fixed cost), electricity, water, internet, and a maintenance reserve for minor repairs or appliance replacement.

The realistic low-to-high range for monthly owner costs in Central Luzon spans from PHP 5,000 (USD 87 or EUR 80) for a small unit in a basic building with low dues to PHP 40,000 (USD 700 or EUR 640) or more for a large unit in a premium development with high dues, parking fees, and significant utility consumption.

The monthly cost that tends to vary the most in Central Luzon is electricity, because air conditioning usage in the region's hot climate can dramatically swing your bill depending on your habits and unit size.

You can see how this budget affect your gross and rental yields in Central Luzon here.

What is the annual property tax amount in Central Luzon in 2026?

As of early 2026, annual property tax (Real Property Tax or RPT) in Central Luzon is based on assessed value rather than market value, with rates typically around 1% to 2% of assessed value plus an additional 1% Special Education Fund levy, meaning the actual peso amount depends heavily on your property's official assessment.

The realistic low-to-high range for annual property taxes in Central Luzon spans from around PHP 5,000 to PHP 50,000 (USD 87 to USD 875 or EUR 80 to EUR 800) for typical residential properties, though premium properties with higher assessed values will pay more.

Property tax in Central Luzon is calculated by applying the LGU's tax rate to the property's assessed value (which is a percentage of the fair market value as determined by the local assessor), not the purchase price or current market price, which is why actual tax bills often feel lower than expected.

Exemptions or reductions in Central Luzon may be available for certain categories like senior citizens or properties used for specific purposes, though these vary by LGU and require application to the local assessor's office.

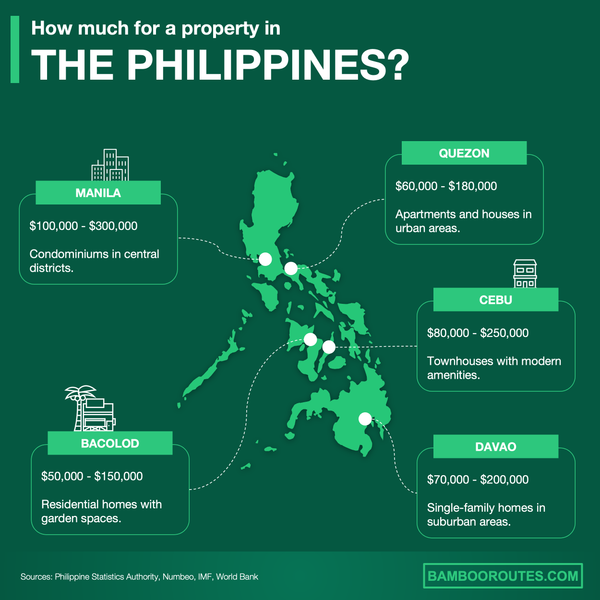

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of the Philippines. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

If I rent it out, what extra taxes and fees apply in Central Luzon in 2026?

What tax rate applies to rental income in Central Luzon in 2026?

As of early 2026, rental income in Central Luzon is taxed as ordinary income under the Philippine tax system, with rates ranging from 0% to 35% for resident individuals depending on total taxable income, while non-resident foreigners may face a flat 25% final withholding tax on gross rental income.

Landlords in Central Luzon can generally deduct allowable expenses from rental income, including property depreciation, repairs and maintenance, association dues, property taxes, and insurance, which can significantly reduce the taxable amount.

The realistic effective tax rate after deductions for typical landlords in Central Luzon often falls between 10% and 25% of gross rental income, depending on the owner's total income level and how many legitimate expenses can be documented and claimed.

Foreign property owners in Central Luzon typically pay a different rental income tax rate than residents, with non-resident aliens subject to a 25% final withholding tax on gross income rather than the graduated rates available to residents.

Do I pay tax on short-term rentals in Central Luzon in 2026?

As of early 2026, short-term rental income in Central Luzon (such as Airbnb or similar platforms) is taxable as income and may also trigger local business permit requirements and potentially VAT registration if your annual gross receipts exceed the VAT threshold.

Short-term rental income is generally taxed the same way as long-term rental income in Central Luzon in terms of income tax rates, but the compliance burden is higher because you may need additional local permits, and some condominium corporations in Central Luzon restrict or prohibit short-term rentals entirely.

If you're interested, we've published a detailed guide about Airbnb regulations and short-term rentals in Central Luzon.

Get to know the market before buying a property in Central Luzon

Better information leads to better decisions. Get all the data you need before investing a large amount of money. Download our guide.

If I sell later, what taxes and fees will I pay in Central Luzon in 2026?

What's the total cost of selling as a % of price in Central Luzon in 2026?

As of early 2026, the total cost of selling a property in Central Luzon typically ranges from 8% to 12% of the sale price when you add up all seller-side taxes, commissions, and fees.

The realistic low-to-high percentage range for total selling costs in Central Luzon spans from about 7% (if you sell without an agent and have minimal fees) to 14% or more (if you use a full-service broker, pay all taxes, and have additional document or clearance costs).

The specific cost categories that typically make up that total in Central Luzon include Capital Gains Tax (6%), Documentary Stamp Tax (around 1.5% if the seller pays), broker commission (3% to 5%), notary and document fees, and clearance costs like condo or HOA certificates.

The single largest contributor to selling expenses in Central Luzon is almost always the 6% Capital Gains Tax, which alone accounts for more than half of total selling costs in most transactions.

What capital gains tax applies when selling in Central Luzon in 2026?

As of early 2026, the capital gains tax rate when selling residential property classified as a capital asset in Central Luzon is 6% of the gross selling price or the fair market value, whichever is higher.

Exemptions to capital gains tax in Central Luzon may be available if you sell your principal residence and use the proceeds to purchase a new principal residence within 18 months, though this exemption requires strict documentation and can only be used once every 10 years.

Foreigners do not pay an extra or different capital gains tax rate when selling property in Central Luzon, as the 6% CGT applies to the property transaction regardless of the seller's nationality, though non-residents may face additional compliance requirements like appointing a local tax representative.

Capital gain in Central Luzon is calculated simply by taking the higher of the gross selling price or the BIR zonal value or assessor's fair market value, with the 6% tax applied directly to that amount rather than to the profit over your original purchase price.

We made this infographic to show you how property prices in the Philippines compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about Central Luzon, we always rely on the strongest methodology we can … and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why It's Authoritative | How We Used It |

|---|---|---|

| Bureau of Internal Revenue (BIR) | The Philippines' official tax authority for national tax rules. | We used it as the primary reference for DST rates and CGT rules. We cross-checked all tax figures against this official source. |

| DILG Local Government Code (RA 7160) | The governing law for local taxes like transfer tax and RPT. | We used it to anchor all LGU-level taxes and recurring property taxes. We translated legal ceilings into practical budget ranges for Central Luzon. |

| Grant Thornton Philippines | A major global audit firm citing specific BIR regulations. | We used it to confirm the VAT-exempt threshold and effective date. We treated it as a bridge to official BIR issuances. |

| Land Registration Authority (LRA) Circular 06-2025 | Official LRA guidance on registration fee computation. | We used it to validate how registration fees are determined. We relied on it to avoid misconceptions about which values apply. |

| Supreme Court E-Library Fee Schedule | The Judiciary's official fee schedules used by registries. | We used it to anchor registration fee structure. We justified why we estimate fees as sliding amounts rather than flat rates. |

| CREBA BIR Tax Updates | A large industry association summarizing BIR rules with citations. | We used it to cross-check VAT thresholds and the "higher of" value principle. We used it for triangulation, not as a sole source. |

| LawPhil Condominium Act (RA 4726) | The core law governing condo ownership structure in the Philippines. | We used it to explain what foreigners can realistically buy. We prevented budgeting advice for illegal purchase structures. |

| PRC Real Estate Service Act (RA 9646) | The law regulating licensed brokers and salespersons. | We used it to justify budgeting for licensed brokerage. We treated it as authority for who can legally charge you fees. |

| Malaya Business Insight | A national publication covering condo fees and hidden costs. | We used it as a reality check for condo association dues ranges. We combined it with conservative assumptions for Central Luzon. |

| GMA News | A major national newsroom attributing changes to BIR regulations. | We used it to corroborate VAT threshold information. We only relied on it where it traced back to official BIR issuances. |

Get fresh and reliable information about the market in Central Luzon

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.

Related blog posts

- Is now a good time to invest in property in Central Luzon?