Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Getting a mortgage in the Philippines as a foreigner is possible, but it comes with real restrictions that can surprise first-time buyers.

Most banks will only lend to foreigners who already live in the Philippines or have strong local ties, and the property you can finance is almost always limited to condominiums.

We constantly update this blog post to reflect the latest rules, rates, and bank policies so you always have current information.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in the Philippines.

Can foreigners get a mortgage in the Philippines right now?

Can a foreigner get a residential mortgage in the Philippines right now?

Yes, foreigners can get a residential mortgage in the Philippines, but banks are selective and typically require you to be living in the country or have a strong connection to it.

Foreigners who hold long-term residency visas (like the Special Resident Retiree Visa, or SRRV) or those married to Filipino citizens have the easiest path to mortgage approval in the Philippines.

The most common restriction banks impose on foreign applicants in the Philippines is that you must be a resident in the country under an approved visa category, and some banks only accept foreigners who are married to a Filipino citizen.

By the way, we have a whole document dedicated to mortgages for foreigners in our property pack about the Philippines.

Can I get a mortgage in the Philippines without residency?

Getting a mortgage in the Philippines without residency is uncommon because banks want assurance that you will stay in the country and keep paying in pesos.

The residency statuses that typically qualify for a mortgage in the Philippines include permanent immigrant visas, Special Resident Retiree Visa (SRRV), and certain long-term work visas, while tourist visa holders are almost always declined.

Banks most commonly require non-residents to either provide a Filipino co-borrower, show large peso deposits in a local bank, or make a significantly larger down payment to compensate for the higher risk.

By the way, we've written a blog article detailing residency and citizenship options that exist when you buy property in the Philippines.

Do banks require a local work contract in the Philippines right now?

Many banks in the Philippines prefer applicants with a local work contract, but it is not always mandatory if you can prove stable income another way.

If you do not have a local work contract, Philippine banks typically accept alternatives like overseas employment contracts with consistent remittances, business financial statements, or proof of pension income with regular transfers to a Philippine bank account.

When a local work contract is present, banks in the Philippines usually require at least one to two years of continuous employment history to consider you for mortgage approval.

Can self-employed foreigners qualify for a mortgage in the Philippines?

Yes, self-employed foreigners can qualify for a mortgage in the Philippines, but the application process is more demanding than for salaried workers.

Banks in the Philippines typically require self-employed applicants to show at least two to three years of profitable business history, backed by audited financial statements and tax returns.

Is foreign income accepted for mortgages in the Philippines right now?

Foreign income is sometimes accepted for mortgages in the Philippines, but it depends heavily on how well you can document the income and show regular transfers into a Philippine bank account.

When applicants earn income abroad, Philippine banks typically require translated employment contracts, foreign tax returns, bank statements showing consistent remittances, and sometimes a certificate of employment verified by a Philippine consulate.

Can I buy a primary home (and an investment property?) with a mortgage in the Philippines as a foreigner?

Foreigners can obtain a mortgage for a primary home in the Philippines, and banks actually prefer owner-occupiers because they tend to have lower default rates.

Financing an investment property as a foreigner is also possible in the Philippines, but banks will be stricter about the property's location, resale potential, and your down payment size.

If you're buying for investment, you might want to check our blog article about buying and renting out in the Philippines.

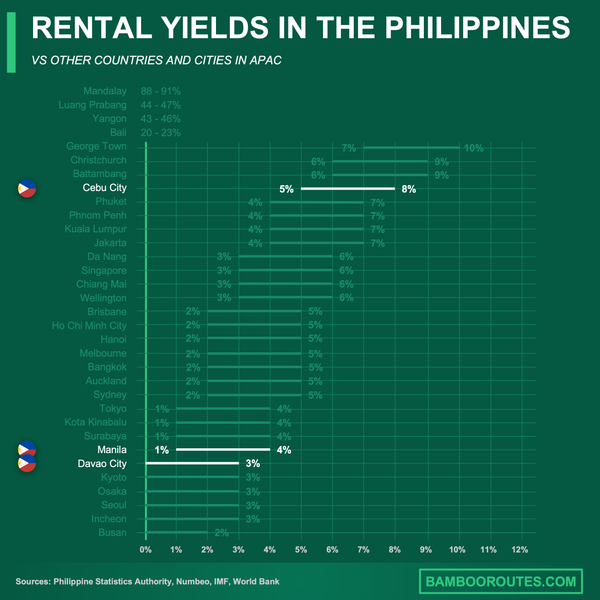

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

What are the eligibility rules banks actually use in the Philippines?

What minimum monthly income do I need in the Philippines as of 2026?

As of early 2026, banks in the Philippines typically require a minimum combined monthly income of around PHP 40,000 to PHP 50,000 (roughly USD 700 to USD 900, or EUR 650 to EUR 850) just to be eligible for a mortgage application.

However, for foreigners buying condos in prime areas like Makati, BGC, or Cebu Business Park, the realistic income range for approved borrowers is PHP 80,000 to PHP 150,000 per month (USD 1,400 to USD 2,700, or EUR 1,300 to EUR 2,500) because property prices push loan sizes higher.

The minimum income requirement in the Philippines scales directly with the loan amount, as banks calculate whether your monthly payment would exceed their debt-to-income comfort zone, typically 30% to 40% of gross income.

Philippine banks do allow combining household incomes from multiple applicants (such as spouses or co-borrowers) to meet the minimum threshold, which is especially helpful for foreigners who may have a Filipino spouse.

What debt-to-income limit do banks use in the Philippines right now?

Banks in the Philippines typically allow a maximum debt-to-income ratio of around 30% to 40% for mortgage approval, meaning your total monthly debt payments (including the new mortgage) should not exceed that share of your gross monthly income.

When calculating your debt-to-income ratio, Philippine banks include all existing debts such as credit card balances, car loans, personal loans, and any other mortgages you already have.

Do I need a local credit score in the Philippines right now?

Philippine banks do not require a single universal credit score, but they strongly prefer applicants who have a credit footprint with the Credit Information Corporation (CIC), the country's public credit registry.

Foreign credit reports can help support your application as supplementary evidence (especially with international banks), but they usually do not replace the local due diligence that Philippine banks perform, including verifying local IDs, address history, and bank relationships.

Do banks require a local guarantor in the Philippines right now?

Philippine banks do not always require a local guarantor for foreigners, but having one can significantly improve your chances of approval if your own profile is borderline.

Banks in the Philippines are most likely to request a guarantor (or co-borrower) when the applicant is a non-resident, has irregular income documentation, or lacks a Philippine banking history.

When a guarantor is required, the guarantor must typically be a Filipino citizen or permanent resident with stable income, good credit standing, and the financial capacity to cover the loan if you default.

Make a profitable investment in the Philippines

Better information leads to better decisions. Save time and money. Download our guide.

How much cash do I need upfront in the Philippines as of 2026?

What's the minimum down payment in the Philippines right now?

The minimum down payment that Philippine banks require from foreign buyers is typically 20% of the property value, which corresponds to a maximum loan-to-value ratio of 80%.

In practice, the realistic range of down payments for foreigners in the Philippines spans from 20% for well-documented resident borrowers to 30% or even 40% for non-residents or those with less verifiable income.

A buyer might secure a lower down payment (closer to 20%) if they have permanent residency, strong local income documentation, an existing relationship with the bank, or are purchasing from a developer that the bank has pre-accredited.

What loan terms can I realistically get in the Philippines as of 2026?

What mortgage interest rates are typical in the Philippines as of 2026?

As of early 2026, the typical mortgage interest rate range for foreigners in the Philippines is around 6.5% to 8.5% per year, with promotional rates from some banks starting as low as 6.0% for short fixing periods.

The factors that most significantly influence the interest rate you receive in the Philippines include the length of your fixed-rate period, the size of your down payment, your income stability, and whether you are buying from a bank-accredited developer.

Foreigners in the Philippines do not automatically receive higher interest rates than local residents, but they may end up at the higher end of the range if their income documentation is complicated or if the bank perceives higher risk.

The interest rate is one of the factors we look at when assessing whether now is a good time to buy a property in the Philippines.

Are fixed-rate mortgages available in the Philippines right now?

Yes, fixed-rate mortgages are available to foreigners in the Philippines, and they are actually a standard feature of most home loan products offered by major banks.

The typical fixed-rate period options offered by Philippine banks include 1 year, 2 years, 3 years, and 5 years, after which the rate resets to a variable rate based on market conditions.

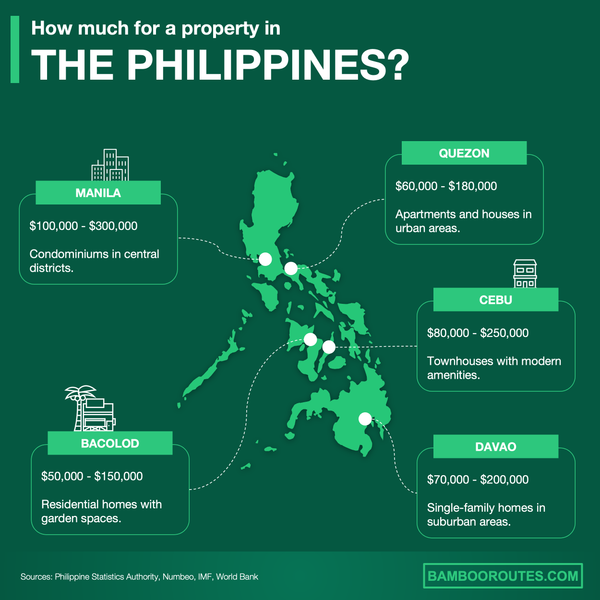

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of the Philippines. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

How do I maximize approval chances in the Philippines right now?

What financial profile gets "yes" fastest in the Philippines right now?

The ideal financial profile that gets mortgage approval fastest in the Philippines is a resident visa holder with stable local income, clean documentation, a Philippine bank account with consistent deposits, and a property in a prime location like Makati, BGC, or Cebu Business Park.

Banks in the Philippines consider an ideal applicant to have a minimum monthly income of around PHP 80,000 to PHP 150,000 (USD 1,400 to USD 2,700, or EUR 1,300 to EUR 2,500) and a debt-to-income ratio below 35%.

The most favored employment type in the Philippines is permanent salaried employment with at least two years of continuous history at the same employer or in the same industry.

A down payment of 30% or more typically signals a strong applicant profile in the Philippines, as it reduces the bank's risk and often unlocks better rates or faster processing.

We give more detailed tips in our pack covering the property buying process in the Philippines.

What mistakes make foreigners get rejected in the Philippines right now?

The most common mistake that leads to mortgage rejection for foreigners in the Philippines is trying to finance a property type you cannot legally own (such as a house-and-lot with land title in your personal name), when only condominium units are available for outright foreign ownership.

The financial red flag that most often disqualifies foreign applicants in the Philippines is presenting income that cannot be quickly verified, such as deposits from multiple sources without clear documentation, irregular freelance payments, or foreign earnings without a consistent remittance trail to a local bank.

Get to know the market before you buy a property in the Philippines

Better information leads to better decisions. Get all the data you need before investing a large amount of money. Download our guide.

Which banks say yes to foreigners in the Philippines right now?

Which banks are most foreigner-friendly in the Philippines as of 2026?

As of early 2026, the banks considered most foreigner-friendly for mortgages in the Philippines include BDO, Security Bank, and Metrobank, which have clearer processes and published eligibility criteria for foreign nationals.

What makes these banks more accessible to foreign applicants in the Philippines is that they explicitly document which visa categories qualify (BDO lists SRRV and other residency visas), publish transparent income thresholds, and have experience processing non-Filipino borrowers.

Which banks accept non-resident borrowers in the Philippines right now?

In the Philippines, very few banks actively accept pure non-resident foreign borrowers, and most successful non-resident applications involve either a Filipino spouse, large local deposits, or a pre-existing bank relationship.

When banks do consider non-resident applicants in the Philippines, they typically require larger down payments (often 30% to 40%), proof of consistent remittances to a local account, and sometimes a local co-borrower or guarantor.

Do international banks lend more easily in the Philippines right now?

International banks do not automatically lend more easily to foreigners in the Philippines than local banks, because the collateral and legal ownership rules are still governed by Philippine law regardless of which bank you use.

International banks with a presence in the Philippines, such as HSBC and Citibank (though consumer banking presence has evolved), may offer advantages if you already have a global relationship with them, but they still apply local underwriting standards.

The main advantage of using an international bank for a mortgage in the Philippines is that they may be more familiar with verifying foreign income, accepting international credit references, and providing cross-border service for documentation.

We made this infographic to show you how property prices in the Philippines compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about the Philippines, we always rely on the strongest methodology we can ... and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why it's authoritative | How we used it |

|---|---|---|

| Bangko Sentral ng Pilipinas (BSP) - Key Rates | The Philippine central bank's official dashboard for policy rates. | We used it to anchor where interest rates stand in January 2026. We also used it to explain why mortgage pricing is where it is. |

| BSP - Weekly Housing Loan Rates | Official BSP statistical release based on bank submissions. | We used it to estimate the realistic mortgage rate band in early 2026. We triangulated it with bank promo pages for accuracy. |

| BDO - Home Loan Promo Mechanics | The bank's own published offer with rates and terms. | We used it as a real market rate anchor. We compared it with BSP statistics and other banks' published rates. |

| Security Bank - Home Loan Requirements | A primary source checklist from a major Philippine bank. | We used it to state typical income and employment requirements. We also used its approval timeline as a realistic benchmark. |

| RCBC - Home Loans | RCBC's published eligibility and product terms page. | We used it to highlight a key restriction: some banks only accept foreigners married to Filipinos. We also used it for down payment expectations. |

| Metrobank - Loan Rates and Fees | Metrobank's official rate card for consumer loans. | We used it to show fixed-rate options across different fixing periods. We triangulated it with BSP stats for a confident rate range. |

| BPI - Housing Loan Requirements | The bank's official list of required documents by income type. | We used it to describe the practical underwriting checklist. We also used it to explain proof of income for foreign earners. |

| 1987 Philippine Constitution (Lawphil) | A widely used full-text legal reference for the Constitution. | We used it to explain the hard boundary on land ownership by foreigners. We kept the explanation simple and buyer-friendly. |

| Republic Act 4726 - Condominium Act | The governing statute for condominium ownership in the Philippines. | We used it to explain why condos are the main foreigner-safe ownership route. We also explained the 40% foreign ownership cap. |

| Credit Information Corporation (CIC) | The country's public credit registry for improving credit access. | We used it to explain what local credit means in the Philippines. We also suggested steps to build a usable local credit record. |

Get the full checklist for your due diligence in the Philippines

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.