Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Central Luzon is experiencing one of the Philippines' most dynamic property booms, with prices surging across Pampanga, Bulacan, and emerging areas. Property values in key cities like Angeles and San Fernando have risen 9.3% year-over-year as of September 2025, driven by major infrastructure projects including the MRT-7 and new Bulacan airport. For investors and homebuyers, understanding the current pricing landscape and strategic opportunities across different municipalities is essential for making informed decisions in this rapidly evolving market.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

Central Luzon property prices range from ₱2.3M for budget houses to ₱40M+ for premium estates, with condos averaging ₱126,000/sqm in Angeles and lot prices hitting ₱79,000/sqm across the region.

The market shows strong momentum with infrastructure-driven growth, offering rental yields of 6-8% in prime areas and significant capital appreciation potential through 2027.

| Property Type | Price Range (₱) | Key Areas | Investment Potential |

|---|---|---|---|

| Budget House & Lot | 2.3M - 3.8M | Mexico, San Fernando | Entry-level, steady growth |

| Mid-Market House & Lot | 4M - 7M | Clark, Angeles | Strong rental yields 5-7% |

| Premium House & Lot | 8M - 40M+ | Clark Freeport, Capital Town | High appreciation, luxury market |

| Condos | 126K/sqm avg | Angeles, San Fernando | 6-8% gross yields |

| Lot-Only | 1.2M - 3.5M | Pampanga, Bulacan | 9.1% CAGR growth rate |

| Townhouse | 3M - 6M | Various developments | Market softening, selective buying |

Which cities and neighborhoods in Central Luzon make the most sense for your investment goals?

The Central Luzon property market centers around five key provinces, each offering distinct advantages depending on your investment strategy.

Pampanga leads the region with Angeles City commanding the highest prices due to Clark Airport proximity and BPO sector growth. San Fernando, as the provincial capital, attracts buyers seeking mixed-use developments and government center access. Mabalacat offers more affordable entry points while still benefiting from Clark spillover demand, with Mexico providing the most budget-friendly house-and-lot options starting around ₱2.3M.

Bulacan presents the strongest infrastructure play, particularly Malolos and San Jose del Monte, which will benefit directly from MRT-7 completion and the new Bulacan airport project expected by 2027. These areas currently offer better value compared to Pampanga but are positioned for significant appreciation as transport links improve. Meycauayan provides industrial-residential blend opportunities for mixed investment strategies.

Bataan, led by Balanga City, represents an emerging market with growing logistics and industrial demand driving residential needs. Nueva Ecija cities like San Jose and Gapan offer stable provincial markets for conservative investors seeking steady rental income from local professionals and families.

Neighborhoods within these urban centers near major roads, new townships like Capital Town, and close to infrastructure projects command premium prices and show the strongest rental demand patterns.

What should your primary investment goal be and what timeline works best?

Your investment strategy in Central Luzon should align with current market conditions and infrastructure development timelines as of September 2025.

For buy-to-live scenarios, Angeles, San Fernando, and newer Pampanga estates provide the best combination of amenities, schools, healthcare access, and airport proximity. These areas offer immediate livability with property values expected to continue appreciating through the infrastructure boom period extending to 2027.

Buy-to-rent strategies work exceptionally well in Angeles due to strong expat and business traveler demand, generating gross yields of 6-8% on properly managed properties. The Clark corridor and upcoming Malolos area near MRT-7 stations present solid long-term rental opportunities as the commuter population grows. Short-term rental markets in Angeles particularly benefit from the steady flow of Clark Airport business travelers.

Buy-to-flip opportunities are strongest in pre-selling developments across Pampanga and Bulacan new townships, especially those aligned with infrastructure announcements. The optimal timeline for flipping runs 3-5 years to capture maximum appreciation as MRT-7 and Bulacan airport projects complete between 2025-2027.

For immediate rental income, target 1-2 year horizons in established areas. For capital gains maximization, 3-5+ year holds align with major infrastructure completions delivering the strongest price appreciation potential.

Which property types offer the best opportunities right now?

The Central Luzon market shows clear preferences for specific property types based on current demand patterns and pricing trends.

Single-detached houses dominate buyer interest and show the strongest price appreciation, up 12.8% year-over-year as families and investors prioritize space and privacy. Lot-only purchases have generated impressive 9.1% compound annual growth rates, making them attractive for land banking strategies in peripheral areas of Tarlac and Bataan.

Condominiums in Angeles and Clark maintain solid demand with gross rental yields reaching 6-8%, particularly for 30-50 square meter units targeting professionals and expats. The condo market benefits from proximity to business centers and airport access, though prices average ₱126,000 per square meter in prime Angeles locations.

Townhouses face some market softness with certain areas experiencing oversupply issues, showing -3.4% year-over-year performance in selected developments. However, well-located townhouse projects in established subdivisions continue performing adequately.

Pre-selling versus ready-for-occupancy decisions depend on your timeline and risk tolerance. Pre-selling units in up-and-coming Bulacan areas near MRT-7 and airport projects offer the strongest appreciation potential. Ready-for-occupancy properties in Clark and Angeles provide immediate rental income opportunities but require higher upfront investments.

Commercial and industrial lots are emerging as alternative investments in Bataan and Clark fringe areas, though these require larger capital commitments and longer development timelines.

What size and configuration should you target for optimal returns?

Property sizing in Central Luzon follows clear market preferences that directly impact both purchase prices and rental yields.

| Property Category | Optimal Size Range | Target Configuration | Market Preference |

|---|---|---|---|

| Houses (Floor Area) | 70-200 sqm | 2-4 bedrooms | Family-oriented, strong demand |

| House Lots | 100-250 sqm | Regular shape, corner premium | Standard suburban preference |

| Condos | 30-50 sqm | Studio to 1 bedroom | Professional/expat market |

| Parking Requirements | 1-2 slots (houses) | 0-1 slot (condos) | Essential for marketability |

| Investment Lots | 100-300 sqm | Road access essential | Land banking potential |

| Premium Lots (Clark) | 300+ sqm | Development zone proximity | High appreciation areas |

The 80-150 square meter floor area range for houses captures the broadest market appeal, accommodating both small families and rental tenants seeking space without excessive costs. Two to three-bedroom configurations prove most liquid for both sales and rentals across all Central Luzon markets.

Lot sizes between 120-200 square meters represent the sweet spot for middle-market buyers, providing adequate space for future expansion while remaining affordable. Corner lots and those with wider road frontage command 10-15% premiums but also offer better resale prospects.

What budget range should you prepare for Central Luzon properties?

Central Luzon property budgets vary significantly based on location, type, and quality level, with clear pricing tiers emerging across the region.

Budget-friendly house-and-lot options start at ₱2.3-3.8M in areas like Mexico and outer San Fernando, typically offering 70-100 square meter homes on 120-150 square meter lots. These properties target first-time buyers and provide steady rental income potential though limited appreciation upside.

Mid-market properties in Clark and Angeles range ₱4-7M for 2-4 bedroom houses with 100-200 square meter floor areas and 150-250 square meter lots. This segment shows the strongest market activity and rental demand, generating 5-7% gross yields while maintaining good liquidity for resale.

Premium properties in Clark Freeport, Capital Town, and established Angeles estates command ₱8-40M+, offering superior amenities, security, and location advantages. These properties appreciate faster during economic expansions but require patient capital and higher maintenance costs.

Lot-only investments require ₱1.2-3.5M for 120-200 square meter parcels across Pampanga and Bulacan, with prime areas near infrastructure projects commanding higher prices. The current average of ₱79,000 per square meter for development-ready lots reflects strong demand from both individual buyers and small developers.

Down payment requirements typically range 12-30% for pre-selling projects and 20-35% for ready-for-occupancy properties. Reservation fees start from ₱10,000-50,000 depending on project scale and developer reputation.

What are the actual market prices you can expect to pay today?

As of September 2025, Central Luzon property prices reflect strong market momentum with specific benchmarks across different categories and locations.

Condominium prices in prime Angeles locations average ₱126,000 per square meter, with premium projects like Marquee Residences by Alveo Land in San Fernando reaching ₱151,000 per square meter. These prices include basic finishing and standard amenities but exclude parking and association dues.

House-and-lot properties across Central Luzon average ₱5.3M, while Pampanga specifically averages ₱3.8M for mid-market options featuring 150 square meter lots and 70-100 square meter floor areas. Ready-for-occupancy properties command 15-25% premiums over pre-selling equivalents.

Lot-only purchases average ₱79,000 per square meter region-wide, with individual parcels typically priced ₱1.2-3.5M depending on size and location. Prime lots near Clark development zones and future MRT-7 stations command significant premiums above regional averages.

Townhouse markets show mixed performance with some oversupplied developments experiencing -3.4% year-over-year declines, though well-located projects maintain stable pricing in the ₱3-6M range for 2-3 bedroom units.

It's something we develop in our Philippines property pack.

Don't lose money on your property in Central Luzon

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What are the total costs beyond the property purchase price?

The complete acquisition cost for Central Luzon properties extends significantly beyond the contract purchase price, requiring careful budget planning for additional fees and expenses.

Transfer taxes and government fees typically add 6-8% to your contract price, including transfer tax (1.5%), documentary stamp tax (1.5%), registration fees (0.5-1%), plus notarial and legal documentation costs. These percentages apply to the declared property value or market value, whichever is higher.

Developer fees for new projects commonly include move-in charges, utility connections, and processing fees ranging ₱50,000-200,000 depending on project scale and amenities. Premium developments may charge additional fees for clubhouse access and exclusive facility memberships.

Ongoing monthly expenses include homeowner association dues of ₱500-2,000+ for house-and-lot communities, while condominium association dues average ₱40-120 per square meter monthly. These fees cover security, maintenance, amenities, and common area upkeep.

Agent commissions typically range 3-5% for secondary market transactions, though developer projects often embed these costs in the selling price. Legal representation and due diligence costs add ₱25,000-75,000 for property verification and transaction completion.

Basic furnishing for rental-ready condition requires ₱300,000-1,000,000+ depending on property size and target market. Higher-end properties targeting expat tenants require premium furnishing investments for competitive rental rates.

For example, a ₱3.8M house-and-lot purchase would total approximately ₱4.1M including taxes, transfer costs, and basic furnishing to rental-ready condition.

What mortgage terms and monthly payments should you expect?

Central Luzon property financing benefits from recent Bangko Sentral ng Pilipinas rate cuts, with current mortgage rates ranging 5.25-5.5% as of September 2025.

| Loan Scenario | Property Price | Down Payment | Monthly Payment (15 yrs) | Total Interest Cost |

|---|---|---|---|---|

| Budget Option | ₱3.8M | ₱760K (20%) | ₱21,000 | ₱1.74M |

| Mid-Market | ₱5.5M | ₱1.1M (20%) | ₱30,400 | ₱2.52M |

| Premium | ₱8M | ₱1.6M (20%) | ₱44,200 | ₱3.67M |

| Low Down Option | ₱3.8M | ₱380K (10%) | ₱23,700 | ₱1.93M |

| High Down Option | ₱3.8M | ₱1.14M (30%) | ₱18,400 | ₱1.58M |

Loan terms typically extend 10-20 years, with minimum down payment requirements of 12% for pre-selling projects and 20-30% for ready-for-occupancy properties. Banks prefer borrowers with stable employment and debt-to-income ratios below 35%.

The difference between 10% and 30% down payments creates monthly savings of ₱2,000-3,000 on typical Central Luzon properties, though higher down payments significantly reduce total interest costs over the loan term.

Pre-selling financing often allows extended down payment terms spread over 6-48 months during construction, reducing initial cash requirements while construction progresses.

What rental yields can you realistically expect across different areas?

Central Luzon rental markets offer attractive yields compared to Manila, with performance varying significantly by location, property type, and tenant targeting strategy.

Angeles and Clark areas generate the highest gross rental yields at 6-8% for condominiums and 5-7% for house-and-lot properties, driven by steady expat, business traveler, and BPO employee demand. The proximity to Clark Airport creates consistent short-term rental opportunities, particularly for furnished units targeting business travelers.

Bulacan markets currently provide more modest 4-6% gross yields, though this is expected to improve significantly as MRT-7 completion increases commuter traffic and the new airport project attracts aviation industry workers. Early positioning in these areas offers the potential for both rental income growth and capital appreciation.

Net rental yields typically run 1-2 percentage points below gross yields after accounting for management costs, vacancy periods, maintenance, and property taxes. Professional property management services charge 5-10% of rental income but often achieve higher occupancy rates and rental premiums.

Short-term rental markets in Angeles can achieve 8-10% gross yields with proper management and consistent occupancy above 70%, though they require more active management and higher furnishing investments. Long-term residential rentals provide steadier income with less management intensity.

The rising job market across Central Luzon continues boosting rental demand, with BPO sector expansion and infrastructure project employment driving rental rate increases of 5-8% annually in prime locations.

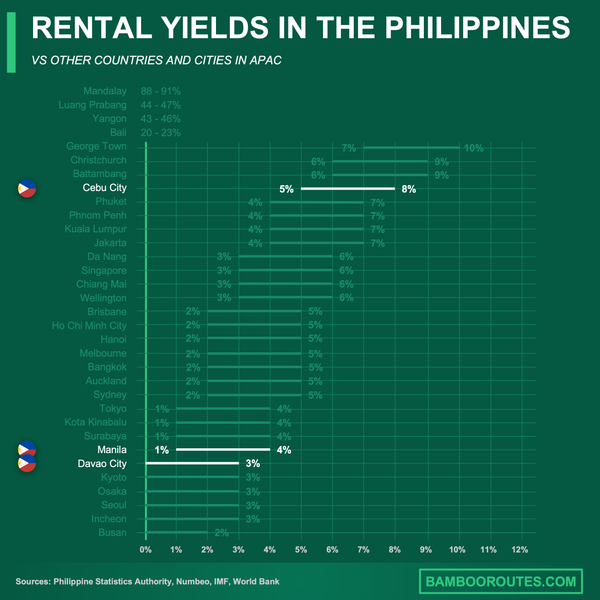

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

Which investment strategy makes the most sense for your situation?

The optimal Central Luzon property strategy depends on your risk tolerance, capital availability, and investment timeline, with each approach offering distinct advantages in the current market environment.

For living purposes, Pampanga locations including Angeles and San Fernando provide the best quality of life combination with access to international schools, private hospitals, shopping centers, and Clark Airport. These areas offer immediate livability while maintaining strong appreciation potential through ongoing infrastructure development.

Long-term rental strategies work exceptionally well in Angeles and upcoming Malolos areas, targeting stable professional tenants from the growing BPO sector and government employees. These markets provide predictable 5-7% yields with lower management requirements and steady tenant demand.

Flipping and capital gains strategies focus on pre-selling developments in Pampanga and Bulacan near new townships, MRT-7 stations, and airport projects. Land banking through lot-only purchases in peripheral areas of Tarlac and Bataan offers high-risk, high-reward potential for patient investors with 5+ year horizons.

Mixed strategies combining immediate rental income with medium-term appreciation work well in Clark corridor properties, providing current cash flow while capturing infrastructure-driven value increases through 2027.

Conservative investors should focus on established areas with proven rental demand, while aggressive growth investors can target pre-development areas with strong infrastructure catalysts but higher execution risk.

It's something we develop in our Philippines property pack.

Which areas offer the best value and which are most expensive right now?

Central Luzon's property market shows clear pricing tiers reflecting development status, infrastructure access, and market maturity levels as of September 2025.

The most expensive areas center on Clark Freeport Zone and central Angeles, where premium estates and established subdivisions command top prices. Capital Town Pampanga and other Megaworld developments represent the luxury segment with properties reaching ₱15-40M+ for high-end houses and premium condominium units.

Up-and-coming areas include the outskirts of Pampanga in Mexico and Mabalacat, offering better entry prices while still capturing spillover demand from Clark expansion. New Bulacan corridors along future MRT-7 and airport routes present the strongest appreciation potential, currently priced below intrinsic value given infrastructure timelines.

Best value opportunities exist in Mexico, outer San Fernando, and Bataan's Balanga fringe areas, where budget-conscious buyers can find quality house-and-lot options starting around ₱2.3M. These areas provide solid fundamentals with steady rental demand from local professionals and families.

Entry-level investors should consider affordable house-and-lot developments in Northern Pampanga and emerging Bataan areas, where lower purchase prices allow easier financing qualification and lower carrying costs during rental property setup periods.

Strategic timing favors areas just ahead of major infrastructure completions, particularly Bulacan properties positioned for MRT-7 and airport benefits before these projects fully price into market values.

How do current prices compare to historical trends and what's the outlook?

Central Luzon property values demonstrate strong momentum with clear historical outperformance and positive forward indicators through 2027 and beyond.

Recent performance shows residential values up 9.3% year-over-year in Q4 2024, with single-detached houses leading at 12.8% appreciation. This growth significantly outpaces the Philippines national average and rivals CALABARZON in price appreciation, particularly for land and detached properties.

The five-year trajectory reveals lot-only units achieving impressive 9.1% compound annual growth rates, while Pampanga consistently outperforms national residential trends. This sustained growth reflects fundamental demand drivers including population migration, infrastructure investment, and economic zone development.

Forward-looking indicators through 2025-2026 remain strongly positive, supported by ongoing infrastructure projects, GDP growth projections of 6.1%, and new government incentives for real estate development. Major price catalysts include MRT-7 completion and Bulacan airport opening between 2025-2027.

Compared to other Philippine markets, Central Luzon remains 50%+ cheaper than Metro Manila in equivalent property categories while closing the gap in prime zones. Growth rates currently rival Cebu and Laguna markets while outpacing mature Manila segments for land and single-detached properties.

Regional Southeast Asian comparisons show Central Luzon offering superior affordability and growth potential compared to similar secondary cities in Thailand, Vietnam, and Indonesia, making it attractive for regional property investors seeking emerging market exposure.

The 10-year outlook supports continued appreciation driven by infrastructure completions, economic zone expansions, and population growth, though investors should expect some moderation from current high single-digit growth rates as the market matures.

It's something we develop in our Philippines property pack.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

Central Luzon's property market in September 2025 presents compelling opportunities across multiple price segments and investment strategies. With infrastructure projects driving appreciation and rental yields exceeding Manila in key areas, the region offers both immediate income potential and strong capital gains prospects.

Success in this market requires matching your specific goals, timeline, and budget to the right locations and property types. Whether targeting budget-friendly options in Mexico and Bataan or premium investments in Clark and Angeles, understanding local market dynamics and timing infrastructure developments will be crucial for maximizing returns in this rapidly evolving real estate landscape.

Sources

- Angeles City Government

- City of San Fernando Government

- Mabalacat City Government

- Malolos City Government

- City of Balanga Government

- Hann Resorts - Central Luzon Economic Rise

- Philippine Daily Inquirer - Real Estate Rally

- ABS-CBN News - Central Luzon Property Hotspots

- Manila Times - Colliers Central Luzon Market Report

- Bangko Sentral ng Pilipinas - Residential Property Price Index