Authored by the expert who managed and guided the team behind the The Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Central Luzon's property market is experiencing significant growth in 2025, driven by major infrastructure projects and strong investor demand.

Property prices have surged across the region, with residential lots rising 9.3% year-on-year and single-detached houses posting impressive 12.8% annual increases. The market is particularly strong in Pampanga and Bulacan provinces, where new expressways, railways, and airports are transforming accessibility and driving substantial property value appreciation.

If you want to go deeper, you can check our pack of documents related to the real estate market in Central Luzon, based on reliable facts and data, not opinions or rumors.

Central Luzon's property market shows robust growth with residential prices up 9.3% annually and strong infrastructure-driven demand in key provinces like Pampanga and Bulacan.

The region offers attractive investment opportunities with rental yields of 3-5% and continued development pipeline, making it favorable for buyers and long-term holders in 2025.

| Market Indicator | Current Status (2025) | Growth/Performance |

|---|---|---|

| Residential Price Growth | ₱79,000/sqm (Pampanga) | +9.3% year-on-year |

| Single-Detached Houses | ₱5.3M average | +12.8% annually |

| Rental Yields | 3-5% region-wide | Up to 6% in business hubs |

| Commercial Land | ₱10,000-₱50,000/sqm | Infrastructure-driven growth |

| Agricultural Land | ₱100-₱10,000/sqm | Location-dependent pricing |

| Office Vacancy Rate | 30% (Q2 2025) | High due to new supply |

| Investment Outlook | Buy/Hold favorable | Strong growth corridors |

How have property prices in Central Luzon changed over the past three years?

Central Luzon property prices have shown remarkable growth over the past three years, with residential properties leading the charge.

Residential lots in Central Luzon rose 9.3% year-on-year in Q4 2024, reflecting a compound annual growth rate (CAGR) of 9.1% across recent years. Single-detached houses posted the strongest performance with 12.8% annual increases, driven primarily by family buyers and overseas Filipino worker (OFW) demand returning to the region.

In Pampanga specifically, residential lot prices reached ₱79,000 per square meter as of 2025, while house-and-lot packages averaged ₱5.3 million. Condominium values grew at a more moderate 5.1% annually, though townhouses experienced a rare decline of -3.4% during the same period.

The growth has been consistent and sustained, making Central Luzon one of the Philippines' most dynamic regional property markets outside Metro Manila.

What are the current average prices per square meter for residential, commercial, and agricultural land?

Property prices in Central Luzon vary significantly based on location and property type as of September 2025.

| Property Type | Price Range (per sqm) | Prime Locations |

|---|---|---|

| Residential Land | ₱5,726 - ₱29,775 | Pampanga: ₱79,000/sqm |

| Condominium Units | ₱50,000 - ₱126,374 | Clark/Angeles City: ₱126,374/sqm |

| Commercial Land | ₱10,000 - ₱50,000 | Provincial business districts |

| Agricultural Land | ₱100 - ₱10,000 | Depends on irrigation/access |

| Industrial Lots | ₱8,000 - ₱25,000 | Economic zones command premium |

Which cities or provinces in Central Luzon are seeing the fastest growth in real estate demand?

Pampanga province leads Central Luzon in real estate demand growth, particularly in Angeles City, Mabalacat, and San Fernando.

Clark and New Clark City represent the top investment destinations in the region, benefiting from their status as major economic and aviation hubs. Bulacan province follows closely, especially areas near the upcoming MRT-7 extension and the new Bulacan International Airport.

Major developers including Ayala Land and Vista Land are actively launching new projects in these growth corridors. Angeles City specifically has seen significant interest due to its proximity to Clark International Airport and established business process outsourcing (BPO) sector.

The fastest appreciation is occurring along major infrastructure corridors, where new expressways and railway connections are reducing travel times to Metro Manila and boosting property values accordingly.

It's something we develop in our Central Luzon property pack.

How are new infrastructure projects impacting property values in Central Luzon?

Infrastructure projects are the primary driver of property value increases across Central Luzon in 2025.

Major expressways including NLEX, SCTEX, TPLEX, and CLLEX have dramatically reduced travel times to Metro Manila, making Central Luzon provinces more attractive for both residents and businesses. The North-South Commuter Railway project further enhances connectivity, with stations planned in key growth areas.

Clark International Airport and the upcoming Bulacan International Airport are creating aviation-centered development zones that command premium property prices. New Clark City, positioned as a major government and business hub, is attracting significant real estate investment and development.

Properties within 5-10 kilometers of major infrastructure projects typically see 15-25% higher appreciation rates compared to areas without direct access. Economic zones and industrial parks linked to these transport networks are experiencing particularly strong demand from logistics and manufacturing companies.

Don't lose money on your property in Central Luzon

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What's the current rental yield for residential and commercial properties in the main urban areas?

Rental yields in Central Luzon's main urban areas range from 3-5% region-wide, with premium locations offering higher returns.

Residential properties in Angeles City and Clark typically generate 4-6% rental yields, particularly for condominiums and house-and-lot units targeting expatriate and OFW tenants. Commercial properties in established business districts can achieve 5-7% yields, though this varies significantly based on tenant quality and lease terms.

New Clark City and areas around major BPO centers offer some of the highest yields, potentially reaching 6-8% for well-located residential units. Agricultural land converted for residential or commercial use often provides lower initial yields but higher capital appreciation potential.

Shopping centers, office buildings, and mixed-use developments in provincial capitals like San Fernando typically generate steady 4-5% yields with long-term lease agreements providing income stability.

How much new housing and commercial development is in the pipeline for the next two to three years?

Central Luzon has approximately 1,000 hectares of new industrial and mixed-use development planned through 2027.

Major developers are announcing significant house-and-lot projects across Pampanga, Tarlac, and Bulacan, with Vista Land leading expansion efforts in the region. Ayala Land is developing several mixed-use townships that combine residential, commercial, and office components.

Office space completions nationwide have averaged 500,000 square meters annually from 2020-2024, with Central Luzon capturing an increasing share of this development. New residential projects focus primarily on middle-income housing to serve the growing workforce in economic zones.

The pipeline includes several master-planned communities designed around new transport hubs, particularly near proposed railway stations and airport access roads. Most developments target completion between 2026-2028 to align with major infrastructure project timelines.

What is the current vacancy rate for condos, apartments, and office spaces?

Central Luzon office spaces hit a concerning 30% vacancy rate in Q2 2025, primarily due to oversupply and reduced corporate demand.

The high office vacancy reflects nationwide trends of excess supply, softer corporate expansion, and reduced Philippine Offshore Gaming Operator (POGO) activity that previously drove significant office absorption. Many new office buildings completed in 2024-2025 struggled to find tenants immediately.

Residential vacancy rates remain more moderate, with condominiums and apartments in prime locations like Clark and Angeles City maintaining occupancy levels around 80-85%. House-and-lot developments targeted at families and OFWs show stronger occupancy due to limited supply relative to demand.

Developers are now being more cautious about new office launches, focusing instead on mixed-use projects that combine residential and retail components with smaller office components.

How strong is the demand from OFWs and foreign investors in Central Luzon right now?

OFW demand remains robust in Central Luzon, continuing to drive residential property purchases across the region.

Strong remittance flows from overseas Filipino workers support consistent demand for residential lots and family homes, particularly in provinces like Pampanga and Bulacan where many OFW families maintain roots. This demographic typically prefers house-and-lot packages over condominiums for family use.

Foreign direct investment declined year-on-year for Q1-Q2 2025 nationwide, but Central Luzon continues attracting interest for logistics facilities, industrial parks, and leisure residential projects. The region's proximity to Metro Manila and improved infrastructure make it attractive for foreign businesses establishing Philippine operations.

Retirement-focused foreign buyers show interest in Clark and Angeles City due to established expat communities, healthcare facilities, and airport accessibility. However, regulatory restrictions on foreign land ownership typically channel this demand toward condominium units and leasehold arrangements.

It's something we develop in our Central Luzon property pack.

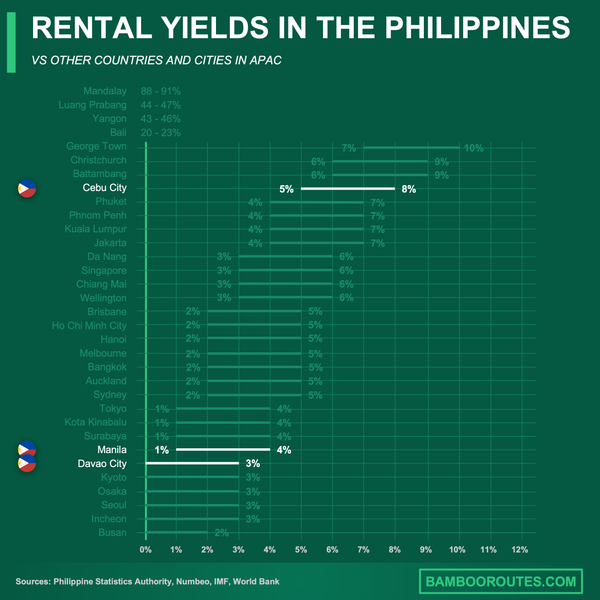

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

What government policies, taxes, or incentives are affecting real estate investment?

Local governments in Central Luzon have implemented several property tax incentives to attract development, particularly for BPO buildings and commercial spaces.

San Fernando and select Bulacan municipalities offer property tax holidays for developers constructing business process outsourcing facilities and commercial developments that meet employment targets. These incentives typically run for 3-5 years and can represent significant savings for large-scale projects.

Business policies under the Philippine Development Plan prioritize regional growth, including specific incentives for new housing developments and industrial projects in designated growth corridors. Special Economic Zones in the region offer additional tax benefits for qualifying businesses and their associated residential developments.

Standard Philippine property taxation applies throughout the region, with transfer taxes, documentary stamp taxes, and annual real property taxes calculated according to national rates plus any applicable local incentives or surcharges.

How do mortgage interest rates and bank financing availability influence property buying activity?

Mortgage interest rates in Central Luzon typically range from 5.25% to 8% as of September 2025, supporting continued property buying activity.

Government-backed loans through Pag-IBIG and Landbank offer some of the most attractive rates at 5.5-6.5%, making homeownership more accessible for middle-income Filipino buyers. These programs are particularly popular among OFW families purchasing their first homes in the region.

Commercial banks commonly offer 70-90% loan-to-value ratios for eligible buyers, with higher ratios available for borrowers with strong credit profiles and stable income. Pre-approved financing has become more common, helping buyers compete effectively in fast-moving markets.

The relatively favorable interest rate environment compared to historical levels continues supporting both end-user purchases and investment activity, though some buyers are accelerating purchase decisions amid expectations of potential rate increases.

What are the risks or challenges that could slow down the property market over the next five years?

Several significant risks could impact Central Luzon's property market growth through 2030.

- Office market oversupply: The 30% vacancy rate in office spaces indicates potential oversupply that could take years to absorb, affecting commercial property values and rental income.

- Declining foreign investment: The 2025 decrease in foreign direct investment could slow industrial and commercial development that drives residential demand.

- Interest rate risk: Rising inflation and potential interest rate increases could reduce buyer affordability and slow transaction volumes.

- Infrastructure delays: Any significant delays in planned railway, airport, or expressway projects could reduce the infrastructure premium driving current price appreciation.

- Economic slowdown: A broader Philippine or global economic downturn could reduce OFW remittances and domestic buyer demand.

Condominium and apartment oversupply risk is emerging in some areas where multiple projects are launching simultaneously, potentially creating downward pressure on both sales prices and rental rates.

Based on all this, is it a better time to buy, sell, or hold property in Central Luzon right now?

September 2025 represents a favorable time to buy or hold property in Central Luzon, particularly in strategic growth corridors.

The combination of ongoing infrastructure development, active rental demand, and continued price appreciation creates attractive conditions for property acquisition. Investors targeting residential land, house-and-lot developments, or prime commercial lots along expressway and railway corridors have the best prospects for capital appreciation and rental returns.

Buyers should focus on Bulacan, Pampanga, and Clark areas where infrastructure projects are creating the strongest value drivers. Properties within 10 kilometers of major transport hubs offer the highest probability of continued appreciation over the next 3-5 years.

Selling may be appropriate for owners of office buildings or commercial spaces facing high vacancy rates, as market conditions favor buyers in these segments. However, residential property owners are better positioned to hold their assets given continued demand fundamentals.

It's something we develop in our Central Luzon property pack.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

Central Luzon's property market in 2025 presents compelling opportunities for strategic investors and end-users alike.

The region's transformation through major infrastructure projects, combined with strong fundamental demand from OFWs and growing business activity, positions it as one of the Philippines' most attractive regional property markets outside Metro Manila.

Sources

- Central Luzon Price Forecasts

- Average Land Price per Sqm Philippines

- Central Luzon Property

- Central Luzon Real Estate Forecasts

- Gulf News - Philippine Infrastructure Projects

- Vista Land Central Luzon Expansion

- Office Market Vacancy Rates

- PSA Foreign Investment Statistics

- Tax Rules and News 2025

- Best Home Loan Philippines