Authored by the expert who managed and guided the team behind the France Property Pack

Yes, the analysis of the French Riviera's property market is included in our pack

Wondering what rental yields you can realistically expect on the French Riviera in 2026?

This article breaks down gross and net yields, neighborhood variations, and the costs that eat into your returns, all based on current data from official French sources.

We update this blog post regularly to keep the numbers fresh and relevant.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in the French Riviera.

Insights

- The average gross rental yield on the French Riviera sits around 3.2% in January 2026, which is lower than most French cities because property prices are driven up by second-home buyers and lifestyle demand, not just rental income potential.

- Neighborhood spreads on the French Riviera can double your yield: buying in Libération or La Bocca instead of the Croisette or Mont Boron can push gross returns from under 2.5% to above 4%.

- Studios and small one-bedroom apartments on the French Riviera typically deliver the highest gross yields (3.6% to 4.6%), because rent per square meter is much higher for compact units than for larger family homes.

- Net yields on the French Riviera drop to around 2.2% on average once you factor in copropriété charges, taxe foncière, insurance, and management fees, which together can consume a full percentage point or more.

- Vacancy rates for long-term rentals in central Nice or Antibes run as low as 2% to 3%, while luxury or seasonal micro-areas can see 6% to 8% vacancy due to thinner tenant pools.

- The typical rent-to-price ratio on the French Riviera is about 0.27% per month, meaning a 300,000 euro apartment usually supports around 800 to 900 euros in monthly rent.

- Upcoming infrastructure projects like Nice Tram Line 5 and the Ligne Nouvelle rail upgrades are expected to lift rents in areas like Paillon valley and Nice Saint-Augustin by 5% to 10% once completed.

- Full-service property management on the French Riviera costs 6% to 9% of rent, plus tenant placement fees, which makes self-management appealing for investors who want to protect net yield.

What are the rental yields in the French Riviera as of 2026?

What's the average gross rental yield in the French Riviera as of 2026?

As of early 2026, the average gross rental yield across residential properties on the French Riviera is around 3.2%, which reflects the premium prices buyers pay for the Mediterranean lifestyle and climate.

Most typical apartments, townhouses, and houses on the French Riviera fall within a realistic gross yield range of 2.2% to 4.8%, depending on whether you buy in a trophy seafront location or a more practical, renter-focused neighborhood.

Compared to the French national average for rental yields (which often sits closer to 4% to 6% in secondary cities), the French Riviera underperforms on pure income metrics because property prices here are supported by second-home demand and international buyers, not just rental math.

The single most important factor influencing gross yields on the French Riviera right now is price dispersion between neighborhoods: buying in a "lifestyle" micro-area like Carré d'Or or Cap d'Antibes versus a "renter-heavy" zone like Libération or La Bocca can easily swing your yield by two full percentage points.

What's the average net rental yield in the French Riviera as of 2026?

As of early 2026, the average net rental yield on the French Riviera is around 2.2%, which is roughly one percentage point below gross yield once you account for all recurring landlord expenses.

The typical gap between gross and net yield on the French Riviera runs between 0.8% and 1.2%, which is larger than in many other French markets because coastal properties often have higher maintenance needs and building charges.

The expense category that most significantly reduces gross yield on the French Riviera is copropriété charges (building fees) combined with taxe foncière, which together can consume the equivalent of one to two months of rent every year.

Most standard investment properties on the French Riviera deliver net yields in the range of 1.4% to 3.6%, with the lower end reflecting trophy locations and the higher end achievable in practical, renter-friendly neighborhoods with newer buildings and lower charges.

By the way, you will find much more detailed rent ranges in our property pack covering the real estate market in the French Riviera.

We made this infographic to show you how property prices in the Philippines compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What yield is considered "good" in the French Riviera in 2026?

On the French Riviera, a gross rental yield of 3.8% or higher is generally considered "good" by local investors, because it means you are earning above the market average while still buying in a desirable coastal area.

The threshold that typically separates average-performing properties from high-performing ones on the French Riviera is around 4.5% gross yield, though achieving this usually requires accepting trade-offs like a less prestigious micro-area, a smaller unit, or an older building with renovation potential.

How much do yields vary by neighborhood in the French Riviera as of 2026?

As of early 2026, gross rental yields on the French Riviera can vary by a factor of two between neighborhoods, with spreads ranging from under 2.5% in trophy areas to above 4.5% in more practical, everyday districts.

The neighborhoods that typically deliver the highest rental yields on the French Riviera are renter-heavy areas with reasonable prices, such as Libération, Riquier, Saint-Roch, and Nice Nord in Nice, or La Bocca, Petit-Juas, and Saint-Cassien in Cannes.

The lowest-yield neighborhoods on the French Riviera are the prestigious seafront and hillside locations where buyers pay heavily for views and scarcity, including Croisette and Palm Beach in Cannes, Carré d'Or and Mont Boron in Nice, and Cap d'Antibes.

The main reason yields vary so much across neighborhoods on the French Riviera is that purchase prices in trophy locations are driven by lifestyle and second-home demand, not rental income potential, while rents stay relatively similar across the market.

By the way, we've written a blog article detailing what are the current best areas to invest in property in the French Riviera.

How much do yields vary by property type in the French Riviera as of 2026?

As of early 2026, gross rental yields on the French Riviera range from around 2.0% for large houses and villas up to 4.6% for well-located studios and small one-bedroom apartments.

The property type that currently delivers the highest average gross yield on the French Riviera is the studio or small one-bedroom apartment, which typically achieves 3.6% to 4.6% because rent per square meter is much higher for compact units.

The property type with the lowest average gross yield on the French Riviera is the detached house or villa, which usually sits between 2.0% and 3.2% because purchase prices are high but rents do not scale up proportionally, plus maintenance costs are steeper.

The key reason yields differ between property types on the French Riviera is that smaller units attract a broader pool of renters (students, young professionals, seasonal workers), which pushes up rent per square meter, while larger properties are priced for owner-occupiers and lifestyle buyers.

By the way, you might want to read the following:

- What rental yields can you expect for a house in the French Riviera?

- What rental yields can you expect for an apartment in the French Riviera?

- What rental yields can you expect for a villa in the French Riviera?

What's the typical vacancy rate in the French Riviera as of 2026?

As of early 2026, the average rental vacancy rate for long-term residential properties on the French Riviera is around 4%, though this varies significantly by location and tenant profile.

Vacancy rates on the French Riviera range from as low as 2% to 3% in high-demand, commuter-friendly neighborhoods like central Nice or Antibes centre, up to 6% to 8% in more seasonal or luxury-skewed micro-areas where tenant pools are thinner.

The main factor driving vacancy rates on the French Riviera is proximity to employment and transport hubs: areas near train stations, the airport, or major job centers see much faster tenant turnover and lower vacancy than prestigious but isolated hillside or seafront locations.

Compared to the French national average vacancy rate (which can exceed 8% in some regions), the French Riviera performs well because strong year-round demand from local professionals, students, and service workers keeps most rental units occupied.

Finally please note that you will have all the indicators you need in our property pack covering the real estate market in the French Riviera.

What's the rent-to-price ratio in the French Riviera as of 2026?

As of early 2026, the average rent-to-price ratio on the French Riviera is about 0.27% per month, which means monthly rent typically equals around 0.27% of the purchase price (or about 3.2% annually).

A rent-to-price ratio above 0.32% per month (or 3.8% annually) is generally considered favorable for buy-to-let investors on the French Riviera, because it translates directly into a gross yield that beats the local average and leaves more room for expenses.

Compared to other popular French coastal areas or secondary cities, the French Riviera's rent-to-price ratio is relatively compressed because property prices are elevated by lifestyle demand and international buyers, while rents are constrained by local wage levels.

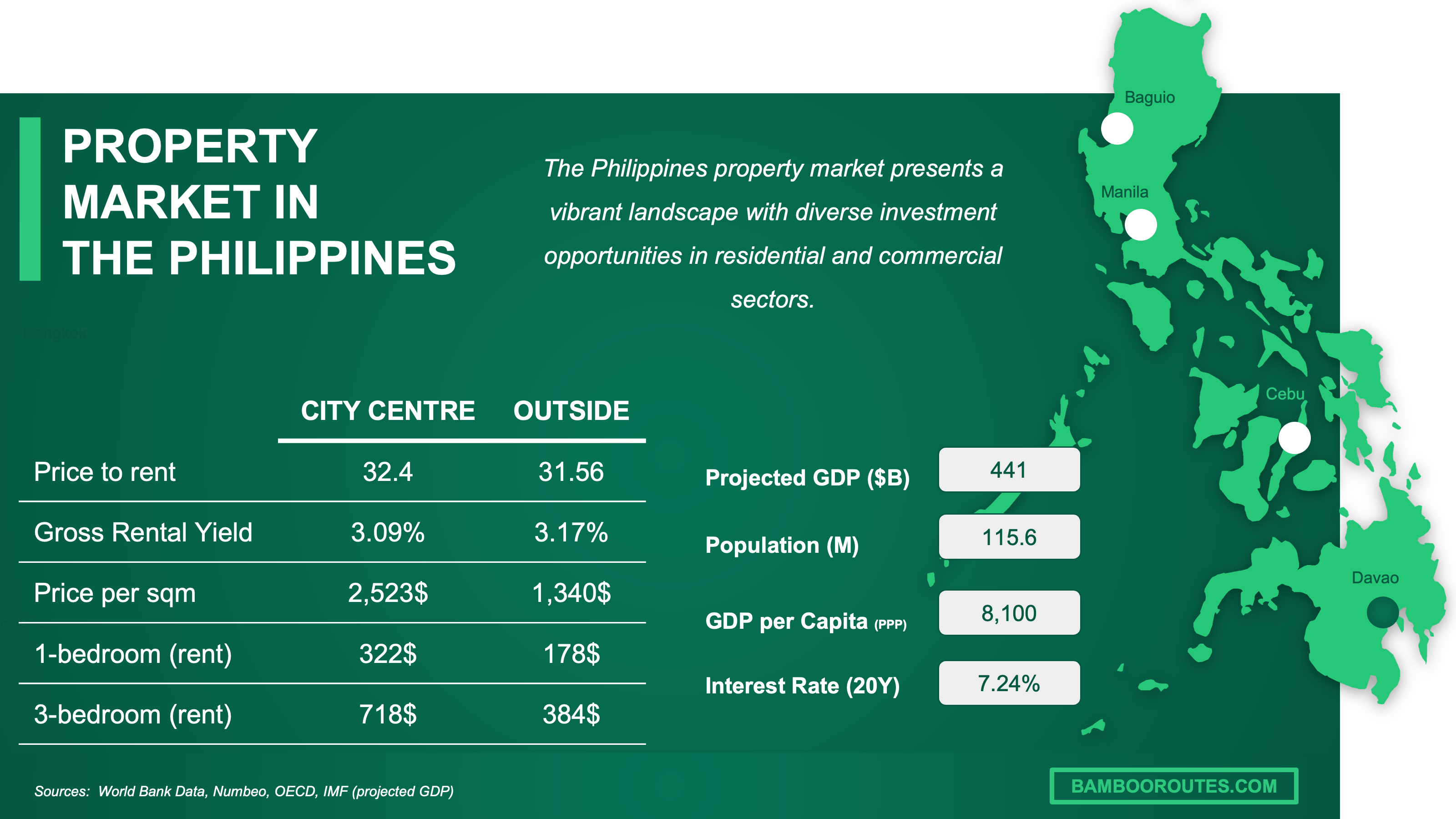

We have made this infographic to give you a quick and clear snapshot of the property market in the Philippines. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Which neighborhoods and micro-areas in the French Riviera give the best yields as of 2026?

Where are the highest-yield areas in the French Riviera as of 2026?

As of early 2026, the top three highest-yield neighborhoods on the French Riviera are Libération and Riquier in Nice, La Bocca in Cannes, and Antibes centre, all of which combine strong local renter demand with more accessible purchase prices.

In these high-yield areas, gross rental yields typically range from 3.8% to 4.6%, with the best returns going to well-bought studios and small apartments in buildings with reasonable charges.

The main characteristic these high-yield neighborhoods share is that they cater to "everyday" renters like local professionals, students, and service workers, rather than to tourists or second-home buyers, which keeps prices rational while rents stay solid.

You'll find a much more detailed analysis of the areas with high profitability potential in our property pack covering the real estate market in the French Riviera.

Where are the lowest-yield areas in the French Riviera as of 2026?

As of early 2026, the three lowest-yield neighborhoods on the French Riviera are Croisette and Palm Beach in Cannes, Carré d'Or and Mont Boron in Nice, and Cap d'Antibes, where trophy pricing pushes gross yields well below the market average.

In these prestigious areas, gross rental yields typically fall between 1.8% and 2.5%, because purchase prices are driven by lifestyle demand and scarcity rather than rental income potential.

The main reason yields are compressed in these areas is that buyers are often acquiring for personal use, capital preservation, or prestige, not for rental returns, which decouples prices from what the rental market can actually support.

Buying a property in a low-yield area is one of the mistakes we cover in our list of risks and pitfalls people face when buying property in the French Riviera.

Which areas have the lowest vacancy in the French Riviera as of 2026?

As of early 2026, the three neighborhoods with the lowest residential vacancy rates on the French Riviera are the Gare Thiers and Libération area in Nice, Antibes centre, and the Centre and Gare district in Cannes, all of which benefit from excellent transport links and steady job access.

In these low-vacancy areas, rental vacancy rates typically run between 2% and 3%, meaning landlords rarely experience more than one or two weeks of vacancy between tenants.

The main demand driver keeping vacancy low in these areas is proximity to train stations, major employers, and everyday amenities, which attracts year-round tenants who prioritize convenience over beachfront prestige.

The trade-off investors face when targeting these low-vacancy areas is that strong demand often pushes purchase prices higher, which can compress gross yields compared to slightly less central neighborhoods.

Which areas have the most renter demand in the French Riviera right now?

The three neighborhoods currently experiencing the strongest renter demand on the French Riviera are Libération and Masséna in Nice, Antibes centre, and La Bocca in Cannes, where local professionals, students, and service workers compete for available units.

The renter profile driving most of the demand in these areas is young to mid-career professionals working in Nice's health, education, tech, and airport sectors, plus seasonal hospitality staff in Cannes and Antibes who need affordable, well-connected housing.

In these high-demand neighborhoods, quality rental listings typically get filled within one to three weeks, and well-priced studios or two-bedroom apartments often receive multiple applications within days of being listed.

If you want to optimize your cashflow, you can read our complete guide on how to buy and rent out in the French Riviera.

Which upcoming projects could boost rents and rental yields in the French Riviera as of 2026?

As of early 2026, the three most significant infrastructure projects expected to boost rents on the French Riviera are Nice Tram Line 5 (extending into the Paillon valley), the Ligne Nouvelle Provence Côte d'Azur rail capacity upgrades, and the BoccaCabana seafront redevelopment in Cannes La Bocca.

The neighborhoods most likely to benefit from these projects include the Paillon corridor and eastern Nice communes like La Trinité and Drap for the tram line, Nice Saint-Augustin and the airport area for the rail upgrades, and La Bocca for the seafront improvements.

Once these projects are completed over the next few years, investors might realistically expect rent increases of 5% to 10% in the directly affected neighborhoods, as improved connectivity and amenities attract a broader and more affluent tenant pool.

You'll find our latest property market analysis about the French Riviera here.

Get fresh and reliable information about the market in Central Luzon

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.

What property type should I buy for renting in the French Riviera as of 2026?

Between studios and larger units in the French Riviera, which performs best in 2026?

As of early 2026, studios and small one-bedroom apartments on the French Riviera outperform larger units in terms of both gross rental yield and occupancy, making them the default choice for income-focused investors.

Studios on the French Riviera typically achieve gross yields of 3.6% to 4.6% (around 550 to 750 euros per month for a 150,000 to 200,000 euro unit, or roughly 600 to 820 USD), while larger two or three-bedroom apartments usually fall in the 3.0% to 3.8% range.

The main reason studios outperform is that rent per square meter is much higher for compact units because there is broad demand from students, young professionals, and seasonal workers who prioritize location and affordability over space.

However, larger units can be the better investment if you are targeting families or roommates in practical neighborhoods like Libération or Antibes centre, where two-bedroom apartments offer lower turnover and more stable tenancies than studios.

What property types are in most demand in the French Riviera as of 2026?

As of early 2026, the most in-demand property type for long-term rentals on the French Riviera is the studio or one-bedroom apartment near transport and job hubs, which attracts the widest pool of tenants.

The top three property types ranked by current tenant demand on the French Riviera are: first, studios and one-bedroom apartments in central locations; second, two-bedroom apartments in practical neighborhoods with schools and parking; and third, small townhouses or ground-floor units with outdoor space.

The primary demographic trend driving this demand is the growing number of young professionals, remote workers, and Sophia Antipolis tech employees who want convenient, affordable housing in well-connected areas rather than sprawling villas.

The property type currently underperforming in demand on the French Riviera is the large detached villa in hillside locations, which appeals mainly to second-home buyers and struggles to attract year-round tenants at rents that justify the purchase price.

What unit size has the best yield per m² in the French Riviera as of 2026?

As of early 2026, the unit size that delivers the best gross rental yield per square meter on the French Riviera is between 18 and 35 square meters, which corresponds to studios and compact one-bedroom apartments.

For units in this optimal size range, gross rental yield per square meter on the French Riviera typically runs between 14 and 18 euros per square meter per month (around 15 to 20 USD or 170 to 215 euros annually per square meter), compared to 10 to 13 euros for larger units.

The main reason smaller or larger units have lower yield per square meter is that very small micro-studios can be hard to rent legally and attract a narrow tenant pool, while units above 60 to 70 square meters see rents rise more slowly than purchase prices because families have more options and less urgency.

By the way, we also have a blog article detailing whether owning an Airbnb rental is profitable in the French Riviera.

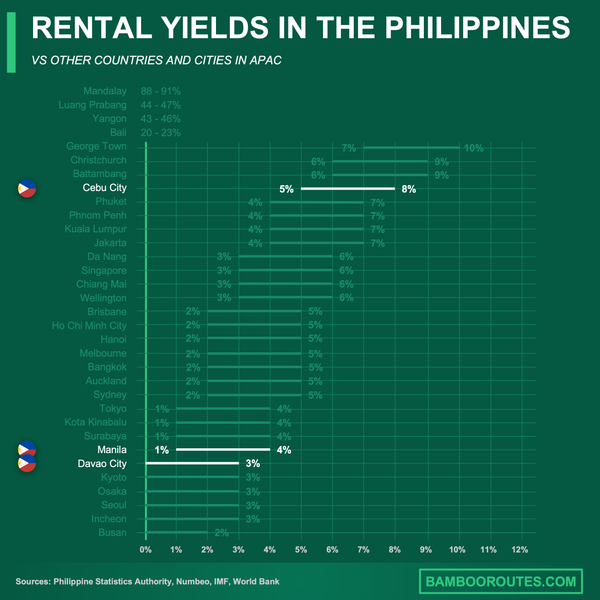

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

What costs cut my net yield in the French Riviera as of 2026?

What are typical property taxes and recurring local fees in the French Riviera as of 2026?

As of early 2026, the annual taxe foncière (property tax) for a typical rental apartment on the French Riviera ranges from 800 to 2,000 euros (around 870 to 2,180 USD), depending on the commune and property size.

Beyond taxe foncière, landlords on the French Riviera must budget for non-recoverable copropriété charges (building fees not passed to tenants), which typically add another 300 to 800 euros per year (330 to 870 USD) for a standard apartment.

Together, these taxes and fees usually represent around 8% to 15% of gross rental income on the French Riviera, which is a meaningful drag on net yield that many first-time investors underestimate.

By the way, we cover all the hidden fees and taxes in our property pack covering the real estate market in the French Riviera.

What insurance, maintenance, and annual repair costs should landlords budget in the French Riviera right now?

The annual landlord insurance cost (assurance propriétaire non-occupant) for a typical rental apartment on the French Riviera runs between 250 and 600 euros (around 275 to 655 USD), with higher premiums for older buildings or coastal exposure.

A sensible annual maintenance and repair budget on the French Riviera is 0.5% to 1.0% of property value, or roughly 5% to 10% of annual rental income, to cover routine upkeep and small fixes before they become major problems.

The type of repair expense that most commonly catches landlords off guard on the French Riviera is salt air corrosion damage to balconies, shutters, and exterior fixtures, which accelerates wear compared to inland properties and requires more frequent attention.

In total, landlords on the French Riviera should realistically budget 1,000 to 2,500 euros per year (around 1,090 to 2,725 USD) for the combined cost of insurance, maintenance, and minor repairs on a typical rental apartment.

Which utilities do landlords typically pay, and what do they cost in the French Riviera right now?

In standard long-term rentals on the French Riviera, tenants typically pay electricity, gas, and internet directly, while landlords advance building charges and recover the "recoverable" portion (charges récupérables) from tenants at year-end.

If a landlord does cover utilities (common in some furnished or all-inclusive setups), the monthly cost for a typical apartment on the French Riviera runs between 80 and 150 euros (around 87 to 165 USD), depending on heating type and usage.

What does full-service property management cost, including leasing, in the French Riviera as of 2026?

As of early 2026, full-service property management on the French Riviera typically costs 6% to 9% of monthly rent (around 50 to 90 euros per month, or 55 to 100 USD, for a unit renting at 900 euros), covering rent collection, tenant communication, and routine coordination.

On top of ongoing management, tenant placement fees on the French Riviera usually run one month's rent or more, though tenant-billed portions are capped by law at around 10 to 12 euros per square meter depending on the service, with the rest falling on the landlord.

What's a realistic vacancy buffer in the French Riviera as of 2026?

As of early 2026, landlords on the French Riviera should set aside around 5% of annual rental income as a vacancy buffer, which covers the typical gap between tenancies and any unexpected turnover.

In practice, landlords on the French Riviera experience an average of two to four vacant weeks per year in well-located properties, though this can stretch to six or more weeks in luxury or seasonal micro-areas with thinner tenant pools.

Buying real estate in Central Luzon can be risky

An increasing number of foreign investors are showing interest. However, 90% of them will make mistakes. Avoid the pitfalls with our comprehensive guide.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about the French Riviera, we always rely on the strongest methodology we can … and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why it's authoritative | How we used it |

|---|---|---|

| Observatoires des Loyers (Nice) | It's the official, publicly-backed rent observatory network with consistent methodology across France. | We use it as our anchor for long-term rent levels per square meter in Nice. We also use its zone ranges to explain neighborhood-level yield dispersion. |

| Observatoires des Loyers (Cannes) | Same official observatory approach, focused on Cannes with zone-based rent medians. | We use it to benchmark Cannes long-term rent per square meter and the low-to-high zone spread. We cross-check it against private portals to avoid overstating achievable rents. |

| Observatoires des Loyers (Antibes) | It's part of the same official OLL network and lets us compare rent levels across key Riviera cities consistently. | We use it as the Antibes rent anchor for long-term rentals. We combine it with price benchmarks to compute gross yields for the Antibes and Juan-les-Pins area. |

| data.gouv.fr (OLL dataset) | It's the government open-data distribution channel for OLL outputs, making the data auditable. | We use it to validate that OLL figures are published in an auditable dataset. We use it to support our triangulation approach prioritizing official rent data. |

| INSEE Housing Price Index | INSEE is France's official statistics institute and this series is a core reference for housing price trends. | We use it to frame the macro context (prices stabilizing by early 2025) rather than relying only on portal snapshots. We use it to sanity-check that our January 2026 pricing assumptions are plausible. |

| Le Figaro Immobilier (Nice) | It's a major national outlet with disclosed methodology and granular neighborhood cuts. | We use it for neighborhood-level relative comparisons showing which areas are pricier versus higher-yielding. We keep official OLL as the baseline for long-term rent levels. |

| Le Figaro Immobilier (Cannes) | Same large publisher with a neighborhood table that helps explain intra-city price variation. | We use its neighborhood table to show how yields can diverge inside Cannes. We treat it as complementary to official OLL rent medians. |

| Immobilier Notaires (Nice) | It's the notarial network's official portal, rooted in actual transaction data. | We use it to triangulate portal-based prices with a notary-branded source. We use it mainly as a credibility check on city-level price ranges. |

| Immobilier Notaires (Cannes) | Same notary and transaction grounding, for Cannes specifically. | We use it to cross-check Cannes price levels against portal medians. We use it to avoid anchoring too heavily on asking-price portals in a luxury-heavy market. |

| Immobilier Notaires (Antibes) | Same notary and transaction grounding, for Antibes and Juan-les-Pins. | We use it as a second transaction-based checkpoint for price per square meter. We combine it with OLL rents to compute yield bands for Antibes-area rentals. |

| Service-Public.fr (agency fees) | Service-Public is the French government's official guidance portal for citizens. | We use it to explain which fees landlords typically pay versus what can be charged to tenants. We use it to keep our net yield cost stack legally realistic. |

| Légifrance (fee cap decree) | Légifrance is the official publication of French law and regulations. | We use it to cite the hard caps on certain letting fees to tenants. We then focus on landlord-borne costs when computing net yield. |

| Service-Public.fr (recoverable charges) | Official government guidance on landlord and tenant charge allocation. | We use it to clarify which building charges are usually reimbursed by tenants versus left with landlords. We use it to explain why copropriété fees can drag net yield. |

| Ministry of Economy (local tax tool) | It's an official Ministry and DGFiP channel pointing to open, comparable local tax rates. | We use it to ground the discussion of taxe foncière in official data availability. We use it to justify using ranges by commune for net-yield assumptions. |

| Observatoire des Territoires (vacancy) | A government-backed observatory that standardizes territorial indicators. | We use it to define vacancy consistently and avoid hand-wavy definitions. We then translate that into a conservative rental vacancy buffer for investors. |

| CRE (electricity tariffs) | The CRE is France's energy regulator and the reference for regulated tariff construction. | We use it to anchor utility-cost context when landlords cover utilities in some furnished rentals. We keep utilities mostly tenant-paid in our typical long-term lease net yield. |

| ADEME (maintenance guidance) | ADEME is France's official energy transition agency with practical guidance. | We use it to support the principle that heating systems need regular maintenance. We translate that into a realistic annual maintenance budget range for net yield. |

| Métropole Nice Côte d'Azur (Tram Line 5) | It's the official project page from the metropolitan authority. | We use it to identify infrastructure changes likely to shift renter demand along the Paillon corridor. We use it as pipeline context for rent upside in specific micro-areas. |

| Ligne Nouvelle Provence Côte d'Azur | Official site for a major rail capacity project affecting Côte d'Azur commuting and station areas. | We use it to frame medium-term connectivity improvements around Nice Saint-Augustin and the airport hub. We link those improvements to likely demand for long-term rentals near transport nodes. |

| City of Cannes (BoccaCabana) | It's a municipal project source, not marketing material. | We use it to highlight urban realm upgrades in Cannes La Bocca that can raise livability and rents. We use it to justify why non-prime districts can improve and tighten vacancy. |

| Savills (Riviera prime markets) | Savills is a respected international property consultancy with dedicated Riviera research. | We use it to understand how second-home and lifestyle demand supports prices in trophy locations. We use it to explain why yields are structurally compressed in prime micro-areas. |

Get the full checklist for your due diligence in Central Luzon

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.

Related blog posts

- Is now a good time to invest in property in Central Luzon?