Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Central Luzon's property market is experiencing robust growth with prices rising 9.3% year-over-year and infrastructure investments driving strong demand.

The region offers more affordable entry points than Metro Manila while delivering competitive rental yields of 3-5% annually, making it an attractive destination for both investors and homebuyers seeking value in the Philippines' expanding economic corridor.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

Central Luzon property prices average ₱79,000-₱126,374 per square meter, significantly lower than Metro Manila's ₱140,000-₱210,000 range.

The region shows strong growth momentum with 9.1% compound annual growth rate over five years and major infrastructure projects like MRT-7 and Bulacan International Airport driving future appreciation.

| Key Metric | Central Luzon | Metro Manila |

|---|---|---|

| Average Price per sqm | ₱79,000-₱126,374 | ₱140,000-₱210,000 |

| 5-Year CAGR | 9.1% | 6.7% |

| Rental Yield | 3-5% | 4.5-6% |

| Y-o-Y Price Growth | 9.3% | 5-7% |

| GDP Growth | 6.1% | 4.8% |

| Vacancy Rate Risk | Lower (residential) | 26% (condos) |

| Infrastructure Impact | High (MRT-7, Airport) | Moderate |

What's the current average price per square meter for residential properties in Central Luzon, and how does that compare with Metro Manila and CALABARZON?

As of September 2025, residential properties in Central Luzon average ₱79,000 to ₱126,374 per square meter, with premium areas like Clark commanding the higher end of this range.

This pricing makes Central Luzon significantly more affordable than Metro Manila, where properties average ₱140,000 to ₱210,000 per square meter. The central business districts of Makati and BGC push prices even higher, reaching ₱200,000 to ₱250,000 per square meter.

Compared to CALABARZON, Central Luzon sits in the middle ground. CALABARZON properties range from ₱54,496 to ₱117,269 per square meter, with Laguna being the most expensive province in that region. Central Luzon's pricing reflects its strategic location and growing infrastructure development.

The price difference creates a compelling value proposition for buyers. You can purchase property in Central Luzon for roughly 40-50% less than comparable Metro Manila locations while still accessing major economic centers through improving transportation links.

It's something we develop in our Philippines property pack.

How much have property prices in Central Luzon increased or decreased in the past 12 months, and what's the average annual growth rate over the last 5 years?

Central Luzon property prices surged 9.3% year-over-year through Q4 2024, outpacing the national average and demonstrating the region's strong market momentum.

The growth varies by property type within the region. Single-detached and attached houses experienced the strongest appreciation at 12.8% annually. Condominium units grew more moderately at 5.1%, while townhomes declined 3.4%, reflecting oversupply in certain segments.

Over the past five years, Central Luzon has delivered a compound annual growth rate (CAGR) of 9.1% for land and lot-only properties. This performance significantly outpaces Metro Manila's 6.7% CAGR but trails CALABARZON's impressive 11% CAGR during the same period.

The sustained double-digit growth reflects several factors: infrastructure development, OFW remittance flows, migration from Metro Manila, and foreign investment in economic zones like Clark and Subic.

This consistent appreciation trend positions Central Luzon as one of the Philippines' most reliable property investment markets for capital growth.

What is the forecasted annual price growth for residential and commercial properties in Central Luzon over the next 3 to 5 years?

Central Luzon residential properties are projected to maintain annual price growth of 7-10% through 2030, driven by major infrastructure completions and continued urban migration.

| Property Type | 2026 Forecast | 2027-2030 Range |

|---|---|---|

| Residential (Prime Areas) | 8-11% | 7-10% |

| Residential (Secondary) | 6-9% | 5-8% |

| Commercial Land | 10-15% | 8-12% |

| Office/Retail | 5-8% | 4-7% |

| Industrial | 7-10% | 6-9% |

| Infrastructure Corridors | 12-18% | 10-15% |

| Clark/Subic Zones | 9-13% | 8-11% |

Commercial properties, particularly land near infrastructure nodes, could experience even higher appreciation. Areas around the upcoming MRT-7 line and Bulacan International Airport are expected to see property value spikes of 12-18% annually during peak development phases.

The growth drivers include the ₱735 billion Bulacan International Airport project, MRT-7 completion by 2026-2027, and the Luzon Economic Corridor connecting Subic-Clark-Manila-Batangas. These mega-projects will create significant property value uplift along transport corridors.

However, commercial office properties may grow more conservatively at 4-7% annually due to current oversupply conditions, with vacancy rates around 30% needing to stabilize first.

What are the current rental yields for residential units in Pampanga, Tarlac, and Bulacan, and how do they compare with yields in Metro Manila?

Residential rental yields in Central Luzon currently range from 3-5% annually across Pampanga, Tarlac, and Bulacan, with prime locations like Clark and New Clark City trending toward the higher end of this spectrum.

Pampanga, particularly around Clark Freeport Zone, offers the strongest yields at 4-5% due to sustained demand from business process outsourcing companies and foreign residents. Bulacan yields average 3.5-4.5%, supported by its proximity to Metro Manila and improving infrastructure connectivity.

Tarlac provides more modest yields of 3-4%, reflecting its more agricultural economy, though this is changing as industrial parks expand and transportation links improve with the completion of major highways.

Metro Manila delivers slightly higher rental yields of 4.5-6% for condominiums, with studio and one-bedroom units in premium projects achieving up to 7.2%. The higher yields reflect greater rental demand density and premium pricing power in the capital.

The gap between Central Luzon and Metro Manila yields is narrowing as infrastructure development accelerates urban migration and business relocations to the region. Properties near completed transport links are already commanding premium rents.

Don't lose money on your property in Central Luzon

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

How many new residential and commercial units are expected to be added in Central Luzon by 2026, and what's the vacancy rate trend today?

Central Luzon is experiencing massive supply expansion with nearly 1,000 hectares of new industrial and commercial property development planned through 2027, plus multiple major residential townships currently under construction.

The residential supply pipeline includes several large-scale projects from major developers, though specific unit counts are not publicly disclosed. The focus is on horizontal development (house-and-lot projects) rather than high-rise condominiums, reflecting local preferences and lower land costs.

Commercial property supply is growing rapidly, particularly office and retail spaces in Clark and Subic economic zones. However, this expansion has created oversupply conditions with office vacancy rates reaching approximately 30% as of Q2 2025.

Residential vacancy rates remain healthier than Metro Manila's concerning levels. While Metro Manila condo vacancy is expected to reach 26% by end-2025 due to oversupply, Central Luzon maintains lower residential vacancy rates due to steady absorption from OFW families and internal migration.

The key risk is that aggressive residential launches in 2025-2026 could temporarily increase vacancy rates if supply outpaces absorption, particularly in secondary locations away from major infrastructure nodes.

How many OFW remittances are flowing into Central Luzon annually, and how much of that typically gets invested in property?

National OFW remittances reached $38.3 billion in 2024 and are projected to grow another 3% in 2025, providing a massive funding source for property investments across the Philippines.

Central Luzon benefits significantly from this flow, with 12.7% of OFW households investing remittances in property by Q4 2024. This percentage nearly doubled from Q3's 6.7%, indicating accelerating property investment activity among overseas workers.

The region is particularly popular among OFWs for several reasons: affordable property prices compared to Metro Manila, strong infrastructure development, proximity to international airports, and cultural familiarity for families from Northern Luzon provinces.

OFW property investment focuses heavily on horizontal developments (house-and-lot projects) in Pampanga and Bulacan, where families can build generational wealth while providing retirement homes. This creates sustained demand for residential developments.

It's something we develop in our Philippines property pack.

What's the current mortgage interest rate range in the Philippines, and how would a 1% increase or decrease impact affordability in Central Luzon?

Philippine mortgage interest rates currently range from 5.5% to 7.5% for fixed 3-5 year terms, with rates varying based on loan-to-value ratios, borrower creditworthiness, and lender policies.

A 1% interest rate increase significantly impacts affordability. For a typical ₱3 million property loan, monthly payments would rise by approximately ₱3,000, tightening debt-to-income ratios and potentially disqualifying marginal borrowers from loan approval.

Conversely, a 1% rate decrease would reduce monthly payments by about ₱3,000, increasing borrowing capacity and making properties more accessible to middle-income families. This could stimulate additional demand and accelerate price appreciation.

Central Luzon's affordability advantage means interest rate changes have amplified effects. Lower property prices allow buyers to access larger properties for the same monthly payment, while rate increases can price out entry-level buyers more dramatically than in expensive markets.

Banks are currently maintaining relatively stable lending standards, but any significant rate movements could shift market dynamics, particularly affecting first-time homebuyers and investment property purchases.

What are the current infrastructure projects in Central Luzon, such as new highways, railways, or airports, and how are they expected to impact property values?

Central Luzon is experiencing unprecedented infrastructure development with multiple mega-projects that will transform regional connectivity and property values.

- MRT-7 Extension: Connecting Bulacan to Metro Manila with completion scheduled for 2026-2027, creating property value uplift along the entire corridor

- Bulacan International Airport: A ₱735 billion mega-project driving massive commercial and residential development in surrounding areas

- North-South Commuter Railway (NSCR): High-speed rail connecting Clark to Manila, reducing travel time to under 1 hour

- Luzon Economic Corridor: Comprehensive highway and railway network linking Subic-Clark-Manila-Batangas ports

- Clark International Airport Expansion: Increasing capacity to handle more international flights and cargo operations

These projects are expected to create property value spikes of 15-25% near major transport nodes. Areas within 5 kilometers of MRT stations and airport access points are experiencing the strongest appreciation already.

The infrastructure development addresses Central Luzon's main limitation: connectivity to Metro Manila. Once completed, these projects will make Central Luzon properties increasingly attractive for both residents and businesses seeking lower costs with maintained accessibility.

Commercial property values near logistics hubs and transport connections could appreciate even more dramatically as businesses relocate operations to take advantage of improved regional connectivity.

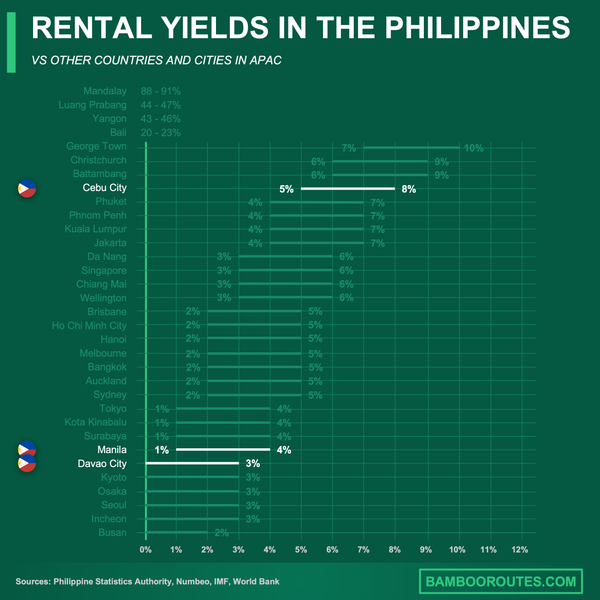

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

How many foreign buyers and investors are purchasing properties in Central Luzon each year, and is this number increasing or declining?

Foreign investment in Central Luzon properties is experiencing a clear upward trend, though exact annual transaction numbers are not publicly available from government statistics.

The growth is concentrated in Clark and Subic Freeport Zones, where foreign ownership restrictions are more relaxed and business-friendly policies attract international investors. Developer reports consistently cite "surging interest" and transaction growth, particularly since 2024.

Foreign buyers are primarily focused on mixed-use developments, commercial sites, and high-end residential properties within economic zones. The appeal includes lower entry costs compared to Metro Manila, growing infrastructure connectivity, and established business environments.

Investment sources include overseas Filipino workers with foreign residency, international business people operating in the economic zones, and regional investors from neighboring ASEAN countries seeking Philippine market exposure.

The trend is supported by infrastructure development making the region more accessible and attractive to international businesses, which in turn drives demand for both commercial and residential properties from foreign nationals working in these companies.

What percentage of Central Luzon's population is urbanizing annually, and how does that affect housing demand and supply?

Central Luzon's population exceeds 12 million as of 2020 census data, with sustained annual urbanization driving strong housing demand, particularly for affordable and mass-market residential units.

While specific annual urbanization percentages are not recently published, the region experiences significant internal migration from rural agricultural areas to urban centers like Angeles, San Fernando, and Malolos. This creates consistent demand for starter homes and affordable housing projects.

Migration from Metro Manila represents another major demand driver. Families and businesses relocate to Central Luzon seeking lower costs, less congestion, and improved quality of life while maintaining reasonable access to the capital through improving infrastructure.

The urbanization pattern creates housing demand across multiple price segments: affordable housing for rural-to-urban migrants, middle-class housing for Metro Manila relocations, and premium housing for professionals working in economic zones.

Developers are responding with horizontal subdivisions rather than high-rise condominiums, reflecting Filipino preferences for landed properties and lower land costs that make this development pattern economically viable.

What's the forecasted GDP growth for Central Luzon in the next 5 years, and how strongly does it correlate with property market performance?

Central Luzon achieved 6.1% GDP growth in 2023, outperforming the national average and establishing the region as one of the Philippines' fastest-growing economic areas.

Five-year GDP growth forecasts for 2025-2030 project sustained expansion of 5.5-6.5% annually, supported by infrastructure completion, manufacturing expansion, OFW remittances, and foreign direct investment in economic zones.

The correlation between GDP growth and property market performance in Central Luzon is particularly strong. Higher economic growth directly supports job creation, wage increases, and business expansion, which translates into greater housing demand and commercial property needs.

Key economic drivers include business process outsourcing expansion, manufacturing growth in Clark and Subic zones, agricultural modernization, and logistics sector development around new transport infrastructure.

It's something we develop in our Philippines property pack.

What risks could slow down property growth in Central Luzon, such as oversupply, rising interest rates, or natural disasters, and how significant are they numerically?

Central Luzon faces several measurable risks that could impact property market growth, with varying levels of significance and probability.

Oversupply Risk: Office sector vacancy rates exceed 30% as of Q2 2025, indicating significant oversupply in commercial properties. Residential oversupply risk is lower but increasing as developers launch aggressive projects that may outpace absorption rates.

Interest Rate Risk: A 1% interest rate increase could reduce homeownership affordability by 10-15% for average borrowers, potentially cooling demand. Current rates at 5.5-7.5% remain manageable but rising trends could impact market momentum.

Natural Disaster Risk: Central Luzon faces significant exposure to flooding, typhoons, and earthquakes common throughout the Philippines. Insurance coverage for catastrophic events remains low, creating financial vulnerability for property owners.

Infrastructure Delays: Major projects like MRT-7 and Bulacan International Airport face potential construction delays that could postpone expected property value appreciation and dampen investor confidence.

Economic Slowdown: Global economic conditions affecting OFW employment and remittance flows could reduce a major source of property investment funding, given that 12.7% of OFW households invest in real estate.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

Central Luzon's property market presents a compelling investment opportunity with strong fundamentals, infrastructure-driven growth, and attractive pricing compared to Metro Manila.

The region's 9.1% compound annual growth rate, major infrastructure projects, and sustained OFW investment flows create favorable conditions for both capital appreciation and rental yields over the next 3-5 years.

Sources

- Central Luzon Price Forecasts

- Colliers Central Luzon Property Market Updates

- Average Land Price Per Sqm Philippines

- Manila Average Condo Prices

- BSP Media and Research

- Global Property Guide Philippines Price History

- CALABARZON Price Forecasts

- Top 12 Philippine Infrastructure Projects

- Central Luzon Property

- Central Luzon Real Estate Forecasts