Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

This is a complete guide for American citizens looking to buy residential property in the Philippines in 2026, covering legal ownership rules, taxes, mortgages, and what the IRS expects from you.

We constantly update this blog post so the information stays current with Philippine laws, tax rates, and market conditions.

Whether you want a condo in Makati, a beachside lease in Cebu, or just to understand how it all works before you commit, this article walks you through it step by step.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in The Philippines.

Can a US citizen legally buy residential property in The Philippines right now?

Can I buy a home in The Philippines as a US citizen in 2026?

As of early 2026, US citizens can legally buy a condominium unit in the Philippines in their own name, but they cannot own land, which means house-and-lot purchases require alternative structures like long-term leases.

The standard buying process for a US citizen purchasing a condo in the Philippines involves selecting a unit where the building still has foreign ownership capacity (under the 40% cap), signing a reservation agreement and Deed of Absolute Sale, paying applicable taxes to the Bureau of Internal Revenue, and then registering the title at the Registry of Deeds to obtain your Condominium Certificate of Title.

What makes The Philippines different from many other countries is that the restriction is not about nationality but about the type of property: any foreigner, including Americans, can own a condo unit outright, but the 1987 Philippine Constitution blocks all foreigners from owning private land, which is why condos are the most common and legally straightforward path for foreign buyers.

By the way, we've written a blog article detailing all the foreigner rights regarding properties in the Philippines.

Are there many Americans buying property and living in The Philippines in 2026?

As of early 2026, there are an estimated 7,000 to 12,000 American long-stay residents in the Philippines at any given time, though no official database directly tracks how many of them own property.

The highest concentrations of American expats and property owners in the Philippines are found in Metro Manila neighborhoods like Makati (especially Legazpi Village and Salcedo Village), Bonifacio Global City (BGC) in Taguig, and Ortigas Center in Pasig, as well as in Cebu City areas like IT Park, Lahug, and Cebu Business Park, plus retirement-friendly cities like Dumaguete and Davao.

The top three reasons Americans choose to buy property and relocate to the Philippines are the significantly lower cost of living compared to the United States, the widespread use of English across the country, and the warm tropical climate paired with a welcoming local culture and strong family ties (many American-Filipino families maintain connections).

The American expat community in the Philippines appears stable to slightly growing in 2026, driven by the rise of remote work, retirement migration (especially with the updated SRRV retiree visa now open to people aged 40 and above since September 2025), and family connections between the two countries.

Do foreigners have the same buying rights as locals in The Philippines?

Foreigners in the Philippines do not have the same buying rights as Filipino citizens because the Philippine Constitution reserves land ownership for Filipinos, but when it comes to condo units, foreigners and locals have equal ownership rights as long as the building's 40% foreign ownership cap is not exceeded, and there is no special advantage or disadvantage for Americans specifically compared to other foreign nationalities.

The property types that are off-limits or restricted for foreign buyers in the Philippines include all private land nationwide (residential lots, agricultural parcels, beachfront land), house-and-lot packages where the land title would need to be in the buyer's name, and any condo project where the 40% foreign ownership quota has already been reached, which happens frequently in popular buildings in BGC, Makati, and Rockwell Center.

We cover all these things in length in our pack about the property market in The Philippines.

Can I buy property in The Philippines without a residence permit?

You do not need a residence permit or any specific visa to buy a condominium in the Philippines, as the purchase is a property transaction that is legally separate from your immigration status.

The process for buying property in the Philippines while living abroad typically involves signing a Special Power of Attorney (SPA) that authorizes a trusted representative in the Philippines to handle document signing, tax payments, and registration on your behalf, though the SPA itself must be notarized at a Philippine consulate or apostilled in the US.

Buying property in the Philippines does not grant you any visa or residency rights, so if you want to live in your condo long-term, you will need to secure a separate visa (such as a tourist visa extension, SRRV retiree visa, or a work-related visa).

The main practical challenge non-resident buyers face when completing a property purchase remotely in the Philippines is the coordination of document notarization, tax payments, and Registry of Deeds filing across time zones, especially since BIR and Registry offices have strict documentary requirements and missing even one item can stall the entire title transfer for weeks.

Can US citizens own land in The Philippines?

US citizens generally cannot own land in the Philippines because the 1987 Philippine Constitution restricts private land ownership to Filipino citizens and to corporations where at least 60% of capital is Filipino-owned, with only very narrow exceptions like hereditary succession.

In the Philippines, "freehold" means you own the land outright and indefinitely (this is only available to Filipinos), while "leasehold" means you rent the land for a fixed number of years, and leasehold is the main path available to foreigners who want to live in a house or use a piece of land, with the maximum lease term recently extended to 99 years under Republic Act 12252, signed into law in September 2025.

There are no geographic zones in the Philippines where foreigners can freely buy land, because the constitutional ban applies nationwide to all private land categories, whether it is a residential lot in Metro Manila, agricultural land in the provinces, or beachfront property in Palawan or Cebu, which is why the leasehold structure or condo ownership remain the only practical options everywhere in the country.

What documents will I need to buy in The Philippines?

To purchase a condo in the Philippines as a US citizen, you will typically need a valid US passport, a Philippine Tax Identification Number (TIN), a notarized Deed of Absolute Sale, proof of funds or source of funds documentation, and the completed BIR tax return forms for Documentary Stamp Tax and transfer processing.

A Philippine Tax Identification Number (TIN) is required in practice because all BIR tax filings and the eCAR issuance process are tied to taxpayer identification, and you can apply for one at any BIR Revenue District Office with your passport or through an authorized representative using a Special Power of Attorney.

A local bank account is not legally required to complete the purchase itself, but it is strongly recommended in practice because it simplifies payment to the seller, makes it easier to show a clear funds trail for anti-money-laundering checks, and is essential if you plan to apply for a mortgage from a Philippine bank.

Philippine banks and developers will ask for proof of funds (such as bank statements or an employer letter) and often request a local contact address for notices and document delivery, especially since foreign wire transfers receive additional scrutiny under the Bangko Sentral ng Pilipinas anti-money-laundering framework.

We have a whole section dedicated to all the documents you need in our The Philippines property pack.

Can a foreign-owned company buy property in The Philippines?

A foreign-owned company can buy a condominium unit in the Philippines (subject to the same 40% foreign ownership cap per building), but a company where foreigners hold more than 40% of the capital cannot legally own land, because the constitutional ownership threshold applies equally to corporations.

Some Americans do set up Philippine corporations to hold property, but this is relatively uncommon for individual residential purchases because the corporation must be at least 60% Filipino-owned to qualify for land ownership, which means the American buyer ends up as a minority shareholder and must rely on carefully drafted shareholder agreements to maintain control.

Owning property through a company structure in the Philippines does not automatically lower your taxes; in fact, the corporation faces its own tax obligations (corporate income tax, annual filings with the SEC, bookkeeping requirements), and any income or gains that flow to you personally will still need to be reported on your US tax return.

The main drawback of using a company structure for residential property in the Philippines is the added cost and complexity: you need to pay for incorporation, annual SEC filings, corporate accounting, and legal advice, and you must find Filipino partners to hold the 60% stake, which introduces trust and governance risks that most individual buyers prefer to avoid.

Thinking of buying real estate in the Philippines?

Acquiring property in a different country is a complex task. Don't fall into common traps – grab our guide and make better decisions.

What taxes and fees will I pay in The Philippines in 2026?

What are buyer taxes in The Philippines in 2026?

As of early 2026, the total buyer tax burden on a typical condo purchase in the Philippines is roughly 2.3% to 3.25% of the property price, so on a PHP 5,000,000 condo (about $86,000 or EUR 72,500), you would pay approximately PHP 115,000 to PHP 162,500 (around $2,000 to $2,800 or EUR 1,650 to EUR 2,350) in government taxes and registration fees.

The individual tax components that buyers in the Philippines typically shoulder are the Documentary Stamp Tax (DST) at 1.5% of the sale price or zonal value (whichever is higher), the Local Transfer Tax at 0.5% to 0.75% depending on the city or municipality, and Registry of Deeds registration fees at roughly 0.25% to 1% on a sliding scale based on property value.

Buyer tax rates in the Philippines do not differ based on nationality, meaning foreigners pay the same DST, transfer tax, and registration fees as Filipino buyers, and there is no distinction between primary residences and investment properties for these specific transaction taxes.

If you want to go into more details, we also have a page detailing all the property taxes and fees in the Philippines.

What are other closing costs in The Philippines in 2026?

As of early 2026, non-tax closing costs for a buyer in the Philippines typically add another 0.5% to 2% or more on top of government taxes, so on a PHP 5,000,000 condo purchase (about $86,000 or EUR 72,500), budget an additional PHP 25,000 to PHP 100,000 (roughly $430 to $1,725 or EUR 360 to EUR 1,450) for professional and administrative fees.

The main closing cost categories in the Philippines include notarial fees for the Deed of Absolute Sale (PHP 5,000 to PHP 25,000, or about $85 to $430), legal and due diligence fees if you hire an independent lawyer (PHP 10,000 to PHP 50,000, or about $170 to $860), condo corporation transfer and admin fees (PHP 10,000 to PHP 30,000, or about $170 to $520), and bank wire and foreign exchange fees when converting USD to Philippine pesos.

The most negotiable closing cost in the Philippines is the real estate broker's commission (typically 3% to 5% of the selling price), which is customarily paid by the seller in resale transactions, but in some deals the split is negotiated, and in developer sales the commission is usually built into the price so the buyer doesn't pay it separately.

The single closing cost item that tends to surprise foreign buyers the most in the Philippines is the BIR eCAR (Electronic Certificate Authorizing Registration) processing delay, which is not a fee you can just pay and resolve but a gating step that stalls your title transfer if any tax payment, document, or form has even a minor discrepancy.

Are there hidden fees foreigners miss in The Philippines right now?

Foreign buyers in the Philippines should budget an extra PHP 50,000 to PHP 200,000 (roughly $860 to $3,450 or EUR 725 to EUR 2,900) for commonly overlooked costs that are not part of the standard tax and registration bill.

The top three hidden or unexpected fees that foreign buyers most often fail to budget for in the Philippines are condo association "move-in" or transfer fees charged by the building management (PHP 10,000 to PHP 50,000, or about $170 to $860), extra costs for certified true copies and document procurement when dealing with BIR and the Registry of Deeds (PHP 5,000 to PHP 20,000, or about $85 to $345), and the foreign exchange spread and wire transfer fees when sending large sums from a US bank to a Philippine account (which can cost 1% to 2% of the amount transferred).

The ongoing annual costs that foreign property owners in the Philippines most often underestimate are condo association dues (PHP 100 to PHP 200 per square meter per month, so a 40-square-meter unit could cost PHP 48,000 to PHP 96,000 per year, or about $830 to $1,655), annual Real Property Tax (typically 1% to 2% of the assessed value, which is usually well below market value), and special assessments that condo corporations occasionally levy for major building repairs or upgrades.

Getting surprised by hidden fees is one of the pitfalls people face when buying real estate in the Philippines.

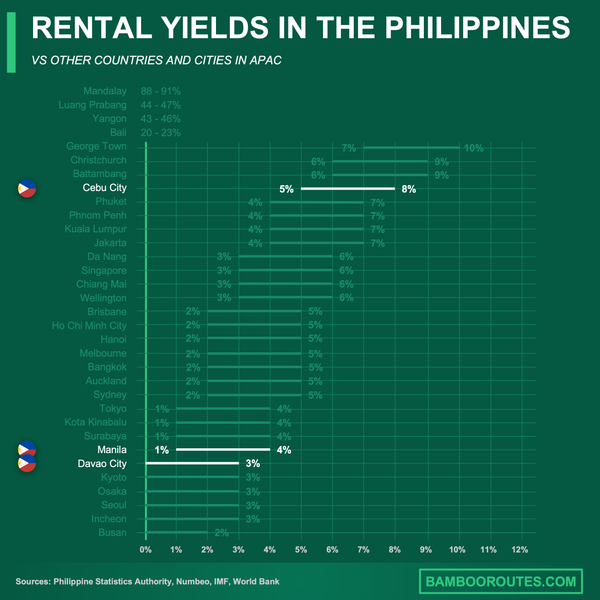

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

Can I get a mortgage as a US citizen in The Philippines in 2026?

Do banks lend to US citizens in The Philippines in 2026?

As of early 2026, some Philippine banks do offer mortgage financing to US citizens, mainly for condo purchases, but approval depends heavily on your residency status, income documentation, and the bank's internal appetite for foreign borrowers.

US citizens do not receive better treatment than other foreign nationals when applying for mortgages in the Philippines; in fact, they sometimes face more paperwork because Philippine banks must comply with FATCA (Foreign Account Tax Compliance Act), which adds extra reporting and verification steps for American account holders.

The main reason some banks in the Philippines are hesitant to lend to American borrowers specifically is the FATCA compliance burden, which requires the bank to report American account holders' information to the IRS, creating additional administrative costs that smaller banks would rather avoid.

A realistic success rate for US citizens applying for property loans in the Philippines is moderate: those with strong local income, a stable visa, and a well-documented financial history have a reasonable chance of approval at major universal banks, but non-resident Americans with only overseas income will find it significantly harder, and many end up paying cash instead.

There is a full document dedicated to mortgage for foreigners in our pack covering the property buying process in The Philippines.

What down payment do American people need in The Philippines in 2026?

As of early 2026, US citizens buying a condo in the Philippines should plan for a down payment of at least 30% to 40% of the purchase price, so on a PHP 5,000,000 property (about $86,000 or EUR 72,500), that means PHP 1,500,000 to PHP 2,000,000 upfront (roughly $26,000 to $34,500 or EUR 21,750 to EUR 29,000).

The typical down payment range for foreign buyers in the Philippines goes from 20% at the low end (usually only available to long-term residents with strong local banking relationships) to 40% or even 50% for non-residents, with 30% being the most common starting point in practice.

A larger down payment does generally improve your mortgage terms in the Philippines because it lowers the bank's risk exposure, which can translate into a slightly better interest rate, a longer repayment period option, and a faster approval process since the bank has less money at stake.

You can also read our latest update about mortgage and interest rates in The Philippines.

What interest rates do US citizens get in The Philippines in 2026?

As of early 2026, US citizens purchasing a condo in the Philippines can expect mortgage interest rates in the range of roughly 6.5% to 8.5% per year, depending on the bank, the fixing period chosen, and the borrower's risk profile.

Interest rates for foreign buyers in the Philippines are generally in line with what local borrowers pay for comparable housing loans, because Philippine banks price mortgages based on the BSP policy rate and the borrower's credit risk rather than nationality, though foreigners may end up at the higher end of the range due to perceived repayment risk.

Most Philippine banks offer a choice between a fixed-rate period (typically 1, 3, or 5 years) that then converts to a variable rate for the remainder of the loan, and a fully variable rate from the start; foreign buyers often prefer the fixed-rate-then-variable structure because it provides predictable payments in the early years, with typical loan terms ranging from 10 to 20 years.

The single factor that has the biggest impact on the interest rate a US citizen will be offered by a Philippine bank is the length of the fixed-rate period: shorter fixing windows (1 year) come with lower initial rates, while locking in a rate for 5 years costs more upfront but gives you payment certainty during that time.

Can I use US income to qualify in The Philippines right now?

Philippine banks will often accept US-sourced income for mortgage qualification, but they treat it with extra scrutiny compared to local income because verifying foreign earnings and ensuring repayment from abroad adds complexity to the bank's risk assessment.

The documentation Philippine banks typically require from American applicants includes recent US tax returns (usually the last two years), pay stubs or an employer verification letter, US bank statements showing regular income deposits, and sometimes a letter from your employer confirming your position and salary, all of which may need to be authenticated or apostilled.

If standard US documentation is not sufficient, some Philippine banks accept alternative verification such as audited financial statements for self-employed applicants, proof of rental income from other properties, or evidence of regular remittances to a Philippine bank account over a sustained period, though each bank has its own policies and flexibility varies widely.

Get fresh and reliable information about the market in the Philippines

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.

How do US taxes interact with owning property in The Philippines?

Do I have to declare the property to the IRS from The Philippines?

Simply owning a condo in the Philippines does not, by itself, create a standalone IRS reporting obligation the way a foreign bank account does, but the moment you earn rental income, sell the property for a gain, or hold it through a foreign entity, you will have US tax filing requirements.

If you rent out your Philippine property, you will report the rental income on Schedule E of your US federal tax return; if you sell the property, you report the capital gain on Schedule D; and if you hold the property through a foreign corporation or partnership, you may also need to file Form 5471 (for foreign corporations) or Form 8865 (for foreign partnerships), depending on your ownership stake.

To be clear, owning a Philippine condo that you use personally and do not rent out does not trigger annual IRS reporting for the property itself, but it becomes reportable when money flows (rental income, sale proceeds) or when the ownership structure involves a foreign entity that the IRS wants to track.

Will I pay tax twice in the US and The Philippines in 2026?

As of early 2026, the risk of being taxed twice on the same Philippine property income is real but manageable, because the US and the Philippines have mechanisms in place to reduce or eliminate double taxation on most types of income.

There is an active US-Philippines income tax treaty, hosted on the IRS website, which provides protections including reduced withholding rates on certain income types and a framework for determining which country gets to tax what, though the treaty itself does not automatically exempt you from anything without proper filing.

The Foreign Tax Credit (IRS Form 1116) is the main tool American property owners use to offset Philippine taxes against their US tax bill: if you pay income tax or capital gains tax in the Philippines on property-related earnings, you can generally claim a credit for those taxes on your US return, dollar for dollar up to the US tax liability on that same income.

Whether annual Real Property Tax paid in the Philippines is deductible on your US federal return depends on your specific situation: if the property is a personal residence, the deduction for foreign real estate taxes was eliminated by the 2017 Tax Cuts and Jobs Act, but if the property generates rental income, the tax is typically deductible as a rental expense on Schedule E, which is why talking to a US CPA before buying is strongly recommended.

Do I need FATCA reporting when buying in The Philippines?

Buying a condo in the Philippines does not, by itself, trigger FATCA reporting because FATCA focuses on foreign financial accounts and certain foreign financial assets, not on real estate held directly in your personal name.

FATCA reporting (Form 8938, Statement of Specified Foreign Financial Assets) is triggered when you hold foreign financial assets exceeding certain thresholds: $200,000 on the last day of the tax year or $300,000 at any point during the year for single filers living abroad (lower thresholds apply for US-based filers), and this would mainly be relevant if you hold Philippine bank accounts or financial instruments tied to your property purchase.

FATCA (Form 8938, filed with your tax return) is different from FBAR (FinCEN Form 114, filed separately with the Treasury): FBAR requires you to report any foreign bank accounts if the combined value exceeds $10,000 at any point during the year, so if you open a Philippine bank account to facilitate your condo purchase, that account alone could trigger FBAR filing even if your FATCA threshold is not met.

Consulting a US CPA before buying property in the Philippines is strongly recommended if you plan to open Philippine bank accounts, earn rental income, hold property through an entity, or move significant funds internationally, and the specific questions to ask include how to structure the purchase to minimize double taxation, which IRS forms will apply to your situation, and whether your foreign accounts trigger FBAR or FATCA filing requirements.

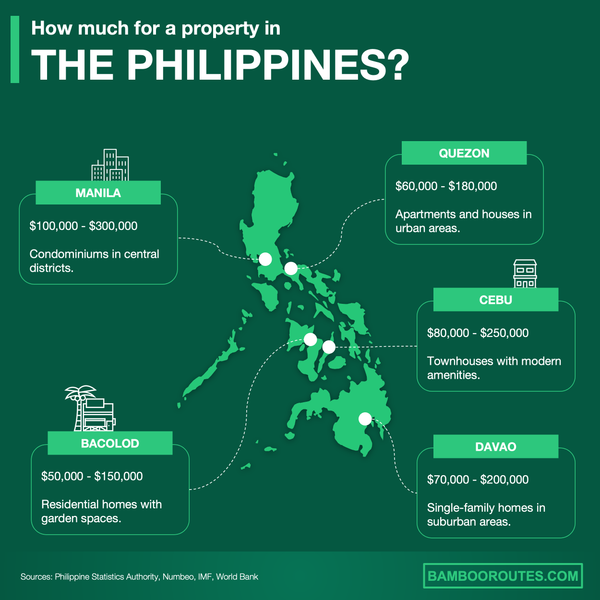

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of the Philippines. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about The Philippines, we always rely on the strongest methodology we can ... and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why we trust it | How we used it |

|---|---|---|

| 1987 Philippine Constitution (Article XII) | It is the top-level legal rulebook that overrides all ordinary laws. | We used it to anchor the "no foreign land ownership" rule. We treated every other rule (condos, companies, leases) as needing to stay consistent with this constitutional foundation. |

| Condominium Act (Republic Act No. 4726) | It is the governing statute for condo ownership and condo corporations. | We used it to explain why foreigners can own condo units under the 40% cap. We also used it to clarify that condo ownership is legally different from owning land. |

| Local Government Code (Republic Act No. 7160) | It is the national law that empowers cities and provinces to charge transfer taxes. | We used it to ground the local transfer tax concept and explain why rates vary by location. We applied it alongside typical market practice examples from Metro Manila and Cebu. |

| Amended Investors' Lease Act (Republic Act No. 12252) | It is the 2025 law that extended foreign land leases to 99 years. | We used it to explain the updated leasehold path for foreigners who want house-and-lot living. We also used it to set expectations on how the new lease terms work in practice. |

| Bureau of Internal Revenue (BIR) - DST page | BIR is the national tax authority for all internal revenue taxes. | We used it to validate DST as a standard buyer cost in property transfers. We paired it with the eCAR checklist to show what actually blocks title registration if unpaid. |

| BIR - eCAR processing checklist | It is BIR's own operational checklist for the tax clearance that unlocks title transfer. | We used it to describe the documentary requirements that buyers must satisfy. We also used it to explain why missing documents or incorrect forms can stall closing for weeks. |

| Land Registration Authority (LRA) - Fee computation tool | LRA is the government body that supervises land title registration. | We used it to confirm that registration fees exist and are computed against the property's value. We used it to warn buyers that registration is not just a flat administrative fee. |

| Bangko Sentral ng Pilipinas (BSP) - Housing loan rates | It is an official, regularly updated statistical table from the central bank. | We used it to produce a grounded interest rate range for housing loans in early 2026. We treated this as the main quantitative anchor for mortgage rate estimates instead of guessing. |

| BSP - Key policy rates | BSP is the central bank; these are its published policy and reference rates. | We used it to set the macro backdrop for mortgage pricing in early 2026. We anchored our rate expectations to the January 2026 BSP policy rate readings. |

| IRS - Philippines tax treaty documents | It is the IRS's official repository for treaty PDFs and related documents. | We used it to confirm the US-Philippines income tax treaty exists and is publicly accessible. We used it to frame double tax relief options at a practical level for property owners. |

| Bureau of Immigration Philippines - Annual report data | It is the immigration authority that tracks all registered foreign nationals. | We used it to estimate the stock of long-stay foreigners in the Philippines (153,000 registrants in 2024). We used this as the base for our American expat population estimate. |

| US Embassy in the Philippines - BI annual report notice | It is an official US government channel communicating requirements to US citizens locally. | We used it to confirm that Americans are a meaningful subset of registered long-stay foreigners. We used it as a real-world signal of the American expat footprint in the Philippines. |

Get to know the market before buying a property in the Philippines

Better information leads to better decisions. Get all the data you need before investing a large amount of money. Download our guide.