Authored by the expert who managed and guided the team behind the Philippines Property Pack

Get all the data you need about the real estate market in Manila

We constantly update this blog post so that buyers can read a fresh view of the Manila real estate market in 2026.

The idea is simple: we want to know whether buying a residential property in Manila in June 2026 is smart, too risky, or better left for later.

We look at prices, rents, vacancies, new supply, financing, infrastructure, resale risk, and the local rules that matter for a normal individual buyer.

And if you’re planning to buy a property in this place, you may want to download our pack covering the real estate market in Manila.

So, is now a good time?

As of June 2026, buying a residential property in Manila is a rather yes, but only if the price is negotiated and the property has real rental or resale demand.

The strongest signal is that Manila and NCR prices are no longer rising fast, with official BSP data showing weak momentum rather than a clear boom.

Another strong signal is that Metro Manila condominium vacancy remains high, which gives careful buyers more bargaining power than sellers of generic units.

Other strong signals are flat rents, slower GDP growth, expensive mortgage conditions, and a large 2026 completion pipeline in parts of Metro Manila.

The best strategy is to prefer fairly priced resale or ready-for-occupancy condominiums in Sampaloc, Ermita, Malate, Paco, Santa Cruz, or Binondo, then rent them long term to students, hospital workers, office workers, or local families.

This is not financial or investment advice, because we do not know your budget, income, risk tolerance, financing terms, or personal situation, so you should always do your own research.

Is it smart to buy now in Manila, or should I wait as of 2026?

Do real estate prices look too high in Manila as of 2026?

As of 2026, residential property prices in Manila look about 5% to 10% above fair value for average condominiums, close to fair value for practical end-user homes, and 10% to 20% too high for weak investor-style units in buildings with too much similar supply.

This view fits the current Manila listings mood, because many sellers still ask high peso-per-square-meter prices, but buyers can often negotiate on resale units, ready-for-occupancy condos, parking, transfer costs, or payment terms.

The second signal is that rents in Manila are not rising fast enough to support a broad price jump, so a unit that only works with optimistic rent assumptions is probably stretched.

You can also read our latest update regarding the housing prices in Manila.

Does a property price drop look likely in Manila as of 2026?

As of 2026, the risk of a meaningful property price decline in Manila is medium for condominiums and low to medium for scarce landed homes or townhouses in strong locations.

Over the next 12 months, we would consider a 0% to 5% nominal decline plausible for average Manila homes, while weaker condominium units could fall 5% to 12% and the best practical units could still rise 0% to 4%.

The most important macro factor is borrowing cost, because high mortgage rates and sticky inflation make buyers more cautious and push investors to demand better rental yields in Manila.

This factor is already present in June 2026, so the question is not whether it appears, but whether rates and inflation stay high long enough to force more sellers to cut prices.

Finally, please note that we cover the price trends for next year in our pack about the property market in Manila.

Could property prices jump again in Manila as of 2026?

As of 2026, the chance of a renewed broad price surge in Manila within the next 12 months is low to medium, because demand is improving but not strong enough to absorb every condominium unit at higher prices.

For the next 12 months, we would consider a 3% to 8% upside plausible in the best Manila micro-locations, but a citywide jump above 8% looks unlikely without cheaper credit or a sharp return of investors.

The biggest demand-side trigger would be faster credit easing, because lower monthly payments would immediately help local buyers, OFW-backed households, and small investors return to the Manila condo market.

Please also note that we regularly publish and update real estate price forecasts for Manila here.

Are we in a buyer or a seller market in Manila as of 2026?

As of 2026, Manila is buyer-leaning for condominiums, neutral for good townhouses, and closer to seller-leaning for rare clean-title landed homes in strong city locations.

The closest useful inventory signal is Colliers’ Metro Manila condominium inventory life of about 6.8 years in Q1 2026, which means buyers still have time to compare units and negotiate.

There is no single official price-cut share for Manila, but high condominium vacancy, flat rents, and developer incentives suggest many sellers have less leverage than their asking prices imply.

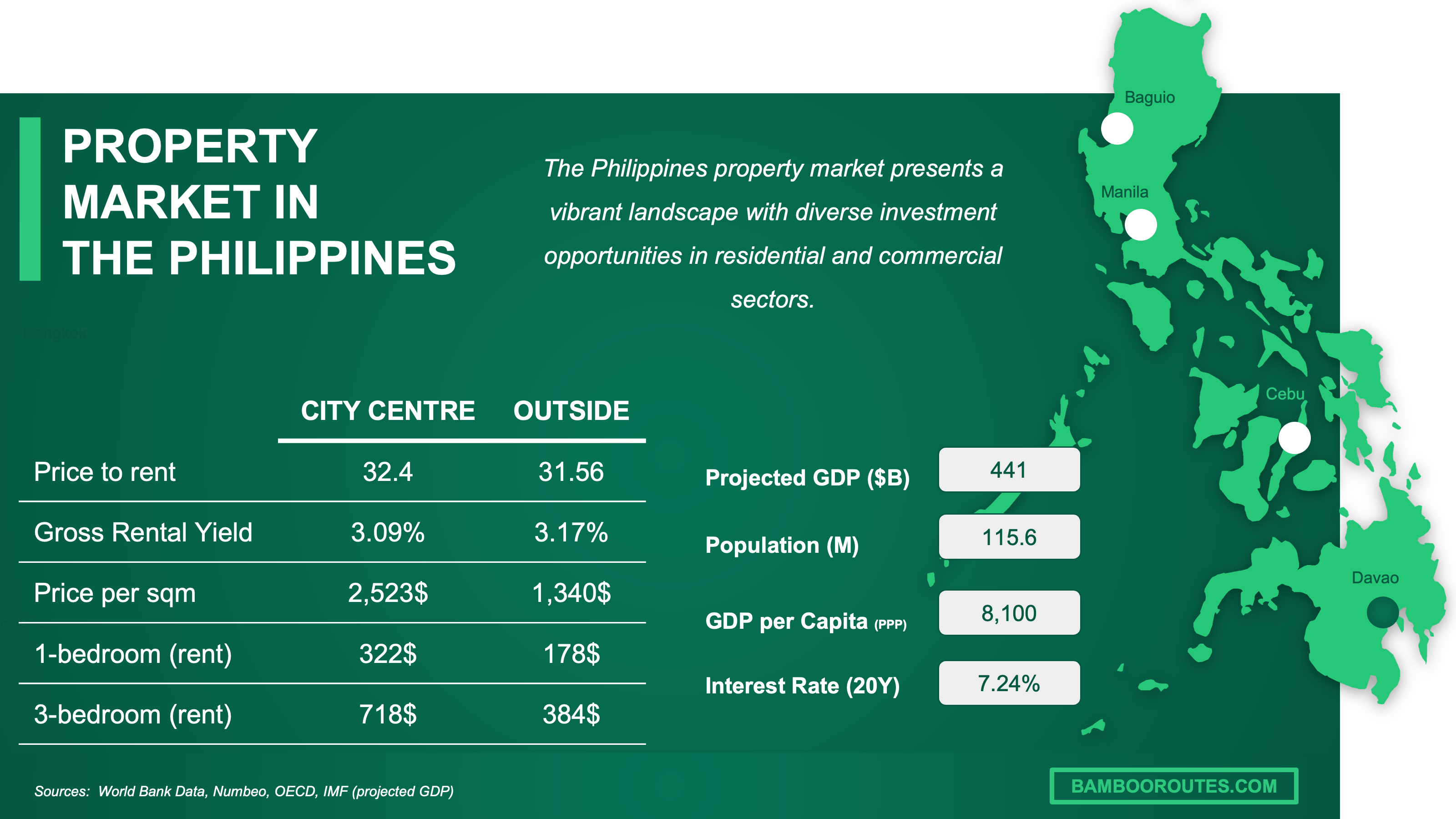

We have made this infographic to give you a quick and clear snapshot of the property market in the Philippines. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Are homes overpriced, or fairly priced in Manila as of 2026?

Are homes overpriced versus rents or versus incomes in Manila as of 2026?

As of 2026, Manila homes look mildly overpriced versus rents and incomes, with the biggest problem in small investor condominiums where dues, vacancy, and soft rents reduce the real return.

The estimated price-to-rent ratio for a good Manila condominium is around 17 to 22, while a more balanced rental investment market would usually feel safer closer to 14 to 18.

The estimated price-to-income multiple is still high for local households in Manila, which means many buyers depend on savings, family support, OFW income, or careful financing rather than ordinary wages alone.

Finally please note that you will have all the indicators you need in our property pack covering the real estate market in Manila.

Are home prices above the long-term average in Manila as of 2026?

As of 2026, home prices in Manila are above their old nominal average, but they do not look far above trend after inflation because recent price growth has been weak.

The latest official BSP data show NCR residential prices rising only about 2.3% year on year in Q4 2025, which is much slower than a classic boom and weaker than many pre-pandemic growth periods.

In inflation-adjusted terms, many Manila condominium values look flat to lower versus the recent cycle peak, so the market is expensive in pesos but not strong in real purchasing-power terms.

Get fresh and reliable information about the market in Manila

Don't base significant investment decisions on outdated data. Get updated and accurate information.

What local changes could move prices in Manila as of 2026?

Are big infrastructure projects coming to Manila as of 2026?

As of 2026, the biggest infrastructure story for Manila property is the Metro Manila Subway and its connection with the wider rail network, which could add a 5% to 15% location premium over several years in areas with real station access or better commute times.

The project is funded and under construction, but completion benefits are gradual, so buyers in Manila should treat the subway as a medium-term support, not as a reason to pay a large premium today.

For the latest updates on the local projects, you can read our property market analysis about Manila here.

Are zoning or building rules changing in Manila as of 2026?

There is no clear citywide zoning shock in Manila in 2026 that suddenly makes all residential property more valuable, but zoning, heritage rules, road access, flood exposure, and redevelopment limits still matter a lot project by project.

As of 2026, the net effect of zoning and building rules on Manila prices is mixed, because rules protect scarcity in old districts but can also limit redevelopment value and raise due-diligence risk.

The most affected areas are older and denser parts of Manila such as Binondo, Ermita, Malate, Santa Cruz, Quiapo, Paco, and parts of Sampaloc, where land use, heritage, access, and building condition can change the real value of a property.

Are foreign-buyer or mortgage rules changing in Manila as of 2026?

As of 2026, the foreign-buyer framework in Manila remains restrictive for land and practical for condominiums, so the price impact is stable rather than dramatic.

The most important foreign-buyer issue is still the condominium ownership limit, because foreigners can buy condo units only within the legal foreign-ownership share of a condominium project.

The most likely mortgage issue is not a new rule but affordability pressure, because BSP policy rates, inflation, and bank caution make leveraged purchases harder in Manila in June 2026.

You can also read our latest update about mortgage and interest rates in The Philippines.

Buying real estate in Manila can be risky

An increasing number of foreign investors are showing interest. However, 90% of them will make mistakes. Avoid the pitfalls with our comprehensive guide.

Will it be easy to find tenants in Manila as of 2026?

Is the renter pool growing faster than new supply in Manila as of 2026?

As of 2026, renter demand in the best Manila neighborhoods is solid, but new condominium supply across Metro Manila is still heavy enough to keep the overall rental market tenant-friendly.

The best demand signal is not abstract population growth, but the steady daily renter base from students, hospital workers, office workers, small traders, public-sector workers, and families in Sampaloc, Ermita, Malate, Paco, Santa Cruz, and Binondo.

The supply signal is less comfortable, because Colliers expects a large Metro Manila completion wave in 2026 and vacancy to remain high, which means weak buildings can struggle even when good Manila locations rent well.

Are days-on-market for rentals falling in Manila as of 2026?

As of 2026, rental days-on-market in Manila look stable rather than clearly falling, with a realistic 30 to 60 days for good units and 60 to 120 days for overpriced or generic units.

The gap between best and weaker areas is important, because a fairly priced unit near universities, hospitals, LRT access, or commerce can rent in about half the time of a similar unit in a high-vacancy tower with many competing listings.

One reason time-to-let can fall in Manila is school-cycle and hospital-worker demand, because tenants often need practical locations before a semester, rotation, or new job starts.

Are vacancies dropping in the best areas of Manila as of 2026?

As of 2026, vacancies in the best Manila rental areas such as Sampaloc, Ermita, Malate, Paco, Santa Cruz, and Binondo look stable to slightly improving, but the broader Metro Manila condominium market remains loose.

Our estimate is that strong Manila buildings can have effective vacancy around 5% to 10%, while the broader Metro Manila condominium vacancy proxy is much higher and can exceed 20% in weaker or oversupplied locations.

A practical sign that the best Manila areas are tightening first is when landlords can renew good tenants without offering big free-rent periods, even while nearby investor condos still advertise discounts.

By the way, we’ve written a blog article detailing what are the current rent levels in Manila.

Make a profitable investment in Manila

Better information leads to better decisions. Save time and money. Download our data.

Am I buying into a tightening market in Manila as of 2026?

Is for-sale inventory shrinking in Manila as of 2026?

As of 2026, for-sale inventory in Manila is hard to measure exactly, but Metro Manila condominium inventory is improving from the worst 2025 levels while still remaining far from tight.

The closest proxy is Colliers’ remaining inventory life of about 6.8 years in Q1 2026, which is better than the 13.4-year peak but still above what buyers would call a balanced market.

The main reason inventory is improving is not a sudden shortage, but stronger affordable and economic condominium take-up after a weak period, while developers still have to clear many units.

Are homes selling faster in Manila as of 2026?

As of 2026, good Manila homes are selling faster than the stressed mid-2025 market, but the average sale is still slow enough that buyers can usually take time to compare options.

We estimate a realistic selling time of 3 to 6 months for well-priced liquid Manila condos, 6 to 12 months for average resale units, and more than 12 months for overpriced or weakly located units.

Are new listings slowing down in Manila as of 2026?

As of 2026, we are not confident enough to give a precise year-on-year change for Manila new resale listings, but developer launches and seller behavior look more cautious than during the boom years.

The normal seasonal pattern is that Manila activity usually improves after holiday periods and around school or work transitions, but June 2026 does not look unusually tight because buyers still have many condominium options.

The most plausible reason new listings are cautious is seller hesitation, because owners of good units do not want to sell into a high-vacancy market unless the price is acceptable.

Is new construction failing to keep up in Manila as of 2026?

As of 2026, new construction is not failing to keep up for investor condominium supply, but it is still failing to deliver enough affordable and practical housing for normal Manila households.

PSA building-permit data show residential construction remains active nationally, while Colliers still expects a large Metro Manila condominium completion wave in 2026.

The biggest bottleneck for truly useful new housing in Manila is land, because the city is dense, old, and constrained by existing buildings, traffic, heritage, flood risk, and redevelopment complexity.

Get to know the market before buying a property in Manila

Better information leads to better decisions. Get all the data you need before investing a large amount of money.

Will it be easy to sell later in Manila as of 2026?

Is resale liquidity strong enough in Manila as of 2026?

As of 2026, resale liquidity in Manila is acceptable for the right property, but weak for generic condominiums bought at full price in buildings with many similar units.

We estimate a healthy resale benchmark at around 3 to 6 months for a good Manila unit, while the broader realistic range is 3 to 12 months depending on price, building condition, rentability, and location.

The property characteristic that most improves resale liquidity in Manila is practical location, especially walkable access to universities, hospitals, LRT stations, offices, commerce, and daily services.

Is selling time getting longer in Manila as of 2026?

As of 2026, selling time in Manila is longer than a hot market but probably not worsening as fast as it did during the weakest 2025 conditions.

Our current estimate is 3 to 6 months for good listings, 6 to 12 months for average listings, and more than 12 months for overpriced units, large units with high dues, or buildings with too many competing resales.

The clearest reason selling time can lengthen in Manila is affordability pressure, because buyers compare the monthly cost of ownership with rent, dues, taxes, and mortgage rates.

Is it realistic to exit with profit in Manila as of 2026?

As of 2026, the likelihood of selling a Manila property with a profit is medium if the buyer holds for long enough, negotiates well, and avoids weak investor-heavy buildings.

The minimum holding period that makes profit realistic in Manila is usually five to seven years, because appreciation is likely to be slow and transaction costs need time to be recovered.

The estimated total round-trip cost drag is often about 8% to 12% of the property price, which is roughly PHP 480,000 to PHP 720,000, about USD 7,800 to USD 11,700, or about EUR 7,200 to EUR 10,800 on a PHP 6 million unit.

The clearest factor that improves profit odds in Manila is buying below market value in a building with durable local tenant demand, because the resale exit then depends less on a market-wide boom.

We made this infographic to show you how property prices in the Philippines compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it’s in our blog articles or the market analyses included in our property pack about Manila, we always rely on the strongest methodology we can and we don’t throw out numbers at random.

We also aim to be fully transparent, so below we’ve listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source used | Why this source is credible | How we used it |

|---|---|---|

| Bangko Sentral ng Pilipinas, Residential Property Price Index Q4 2025 | It is the central bank’s official housing price index. | We used it to judge whether NCR and condominium prices were still rising fast. We treated it as the cleanest official price trend, while noting that it is based on bank-financed purchases. |

| Bangko Sentral ng Pilipinas, RPPI methodology page | It explains how the official housing index is built. | We used it to understand what the RPPI captures and what it misses. We used that caution when applying NCR data to Manila neighborhoods. |

| Bangko Sentral ng Pilipinas, Key Rates | It is the official source for policy rates and inflation snapshots. | We used it to assess mortgage pressure in June 2026. We also used it to test whether expensive financing could push buyers to wait. |

| Bangko Sentral ng Pilipinas, Real Estate Exposure | It tracks bank exposure to real estate loans. | We used it to judge whether a banking-led property crash looked likely. We also used it to check whether loan stress looked large enough to force broad distressed selling. |

| Philippine Statistics Authority, Q1 2026 GDP | It is the official national accounts source. | We used it to test whether the macro backdrop supported another price surge. We treated slower GDP growth as a demand headwind for Manila homes. |

| Philippine Statistics Authority, Construction Statistics from Approved Building Permits | It is the official building-permit dataset. | We used it as a forward signal for future supply. We compared national permit activity with Metro Manila completion forecasts from property consultancies. |

| Colliers, Q1 2026 Philippine Residential Market Report | Colliers regularly tracks Metro Manila residential supply and demand. | We used it for inventory life, preselling, completions, vacancy, and rental outlook. We treated it as key market evidence and cross-checked it with official data. |

| JLL, Manila Residential Market Dynamics Q1 2026 | JLL is a global real estate firm with local Manila coverage. | We used it to cross-check rents, vacancy, completions, absorption, and capital values. We relied on it mainly for direction of change and market tone. |

| Santos Knight Frank, Market Reports | It is a recognized Philippine real estate advisory source. | We used it as a secondary market reference for Manila sentiment. We did not use it as the main source when official data or Colliers and JLL were clearer. |

| Philippine News Agency, Metro Manila Subway and NSCR funding | PNA reports official government infrastructure decisions. | We used it to identify transport projects that may affect accessibility. We focused on the Metro Manila Subway and North-South Commuter Railway funding signal. |

| Philippine News Agency, Subway and NSCR right-of-way update | It reports official DOTr project progress. | We used it to check whether rail projects were moving beyond marketing claims. We treated transport impact as medium-term rather than immediate. |

| Philippine Information Agency, Metro Manila Subway progress | PIA publishes official government information. | We used it to assess the credibility of subway-related price catalysts. We treated the subway as an upside factor only for well-connected locations. |

| Manila City Council, Ordinance No. 8119 | It is Manila’s formal land-use and zoning ordinance. | We used it to understand Manila’s land-use framework. We applied it to neighborhood risk, especially heritage, density, access, and redevelopment constraints. |

| Manila City Council, Ordinance No. 8654 | It is an official zoning amendment. | We used it to check whether zoning rules had changed enough to affect development economics. We treated zoning as a project-specific risk rather than a broad catalyst. |

| Lawphil, Republic Act No. 4726, Condominium Act | Lawphil publishes Philippine legal texts used for primary reference. | We used it to explain why foreigners usually buy condominium units. We also used it to flag foreign-ownership limits as a resale-liquidity issue in some buildings. |

| FOI Philippines, Manila CLUP and zoning requests | It is the official government transparency portal. | We used it to confirm that CLUP and zoning documents are due-diligence items. We treated this as a warning for older buildings and redevelopment plays. |

Don't buy the wrong property, in the wrong area of Manila

Buying real estate is a significant investment. Don't rely solely on your intuition. Gather the right information to make the best decision.

Related blog posts

- What are the best areas to buy a property in property in Manila?