Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

The Philippines property market in 2025 presents a mixed landscape where luxury Metro Manila condos command premium prices while emerging regional cities offer significant value opportunities. With foreign ownership restrictions on land but open access to condominiums, investors need to navigate complex regulations while considering infrastructure developments that are reshaping property values across the archipelago.

Property prices vary dramatically from PHP 203,360 per square meter in luxury Manila condos to PHP 25,000-60,000 per square meter in emerging cities like Iloilo and Bacolod. Rental yields range from 4.0-7.2% depending on location and property type, with financing accessible but requiring higher down payments for foreign buyers.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

The Philippines property market shows strong regional variation with Metro Manila commanding premium prices while emerging cities offer better value and growth potential.

Foreign ownership is restricted to condominiums only, with complex financing terms but attractive rental yields in prime locations ranging from 4.5-7.2%.

| Market Segment | Price Range (PHP/sqm) | Rental Yield | Investment Profile |

|---|---|---|---|

| Metro Manila Luxury Condos | 203,360 | 4.5-7.2% | High demand, premium pricing |

| Cebu City Prime Condos | 80,000-150,000 | 4.96-5.74% | Steady growth, rising demand |

| Davao City Properties | 40,000-90,000 | 4.5-5.0% | Stable, upside potential |

| Secondary Cities (Iloilo, Bacolod) | 25,000-60,000 | 4.0-5.5% | Strong value appreciation prospects |

| Resort Areas (Boracay, Palawan) | 100,000+ | Variable | Tourism-dependent, seasonal |

How much does property cost right now in the Philippines, broken down by city, region, and property type?

Property prices in the Philippines as of September 2025 show extreme variation depending on location and property type.

Metro Manila luxury condominiums command the highest prices at PHP 203,360 per square meter, translating to roughly $192,000 for a studio unit. The national average index sits at PHP 11,252 per square meter, but this figure masks significant regional differences.

Cebu City prime condominiums range from PHP 80,000 to PHP 150,000 per square meter, while townhouses in the area cost between PHP 4 million and PHP 12 million. Davao City properties are more affordable at PHP 40,000 to PHP 90,000 per square meter, with houses and lots ranging from PHP 2.5 million to PHP 13.4 million.

Secondary and emerging cities like Iloilo and Bacolod offer the best value at PHP 25,000 to PHP 60,000 per square meter, presenting strong appreciation prospects. Premium resort areas including Boracay and Palawan command PHP 100,000+ per square meter, especially for beachfront properties.

The Q1 2025 median home price nationwide reached PHP 3.37 million, with condominiums generally showing higher turnover and rental yields, particularly in urban cores.

What's the difference in short-term, medium-term, and long-term price trends across these areas?

Short-term trends over the last 12 months show Metro Manila residential prices up 6.5% on average, though the luxury segment experienced slight declines.

Cebu maintained steady 3-7% growth while Davao remained stable with modest increases. "Next wave" cities and infrastructure-driven areas showed above-average appreciation, though some regions like Metro Cebu saw slight price dips due to oversupply issues.

Medium to long-term projections for the next 1-5 years indicate Metro Manila will experience steady but slower price appreciation as high-end segments stabilize, with more growth expected in affordable and mid-tier market niches. Cities like Cebu, Pampanga, Clark, Iloilo, and Bacolod are expected to outpace Manila growth rates, supported by major infrastructure projects and economic decentralization.

Long-term supply and demand fundamentals remain positive outside oversupplied city centers, benefiting from migration patterns, BPO expansion, and continued infrastructure investment. The government's focus on developing secondary cities through improved transportation and business districts creates significant upside potential for regional markets.

It's something we develop in our Philippines property pack.

How much rental income can you realistically expect today in different markets, and how do yields compare?

| City/Property Type | Gross Rental Yield (%) | Monthly Rent (USD, 1BR/Studio) | Investment Profile |

|---|---|---|---|

| Manila CBD Condos | 4.5-7.2 | $800-$1,600 | High demand, quick turnover |

| Central Cebu Condos | 4.96-5.74 | $480-$1,050 | Steady demand, rising |

| Davao Average Properties | 4.5-5.0 | $350-$700 | Stable, upside potential |

| Secondary Cities | 4.0-5.5 | $300-$650 | Improving, affordable entry |

| Resort Areas | 3.5-6.0 | $400-$1,200 | Seasonal, tourism-dependent |

What are the projected rental trends for the next 3 to 5 years?

Rental market conditions face mixed prospects with current vacancy rates remaining elevated, particularly in Metro Manila where vacancy exceeds 24% following the Chinese tenant exodus.

However, stabilization is expected by mid-term as market conditions normalize and new demand sources emerge. Yields are likely to hold steady or rise slightly in emerging and suburban markets with lower supply pressure and higher demand growth, including areas like Bulacan, Iloilo, Cagayan de Oro, and Clark.

Post-pandemic demand patterns favor affordable urban units and flexible mid-term rental arrangements as business expansion continues. The rise of hybrid work models and provincial business centers creates new rental demand outside traditional Metro Manila hotspots.

Office and commercial rental segments continue facing oversupply challenges with muted rent growth expected. However, residential rental demand should benefit from infrastructure completion and improved connectivity in emerging city corridors.

Rental yields in secondary cities may outperform Metro Manila as these markets mature and attract more professional tenants seeking affordable alternatives to expensive urban centers.

Don't lose money on your property in the Philippines

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

How liquid is the resale market—how fast can you sell, and at what average resale margins?

Property selling timeframes typically range from 3 to 6 months in prime locations, though market conditions significantly impact liquidity.

Resale margins vary considerably based on location and timing. Hot secondary markets can outperform saturated areas, while oversupplied locations often see sluggish resales or break-even pricing scenarios. During current oversupply periods in 2025, resale margins have narrowed substantially, creating negotiation opportunities for buyers.

Recovery in resale speed and margins is anticipated alongside expected interest rate decreases and major infrastructure project completions. Properties in infrastructure development corridors typically maintain better liquidity profiles than those in mature, saturated markets.

Undervalued assets in transitional markets may present opportunities for investors with longer time horizons, particularly as government infrastructure investments reach completion over the next 2-3 years.

Condominium units generally offer better liquidity than houses and lots, especially in urban centers with established rental markets and foreign buyer interest.

What are the government rules on foreign ownership, and how do they affect condos, land, and houses differently?

Foreign ownership regulations in the Philippines create distinct investment pathways depending on property type.

For condominiums, foreigners may own up to 40% of total project units on a freehold basis for the unit itself, though not for the underlying land. This makes condos the most accessible investment vehicle for foreign buyers seeking direct ownership.

Land ownership remains strictly prohibited for foreigners unless structured through a Philippine corporation with maximum 40% foreign equity participation. Some exceptions exist for legal heirs through inheritance, and long-term lease arrangements of 50 years with 25-year renewal options are available.

Houses present a middle ground where foreigners may own the building structure but not the land beneath it. Properties can be purchased on leased land arrangements, though this creates additional complexity and risk factors.

The Anti-Dummy Law is strictly enforced against fake local ownership arrangements on behalf of foreigners, making legitimate corporate structures essential for land-related investments.

What taxes, fees, and ongoing costs should you budget for upfront and long-term?

Real Property Tax (RPT) represents the primary ongoing cost, reaching up to 2% of assessed value in Metro Manila and 1% in provincial areas, plus an additional 1% special education fund nationwide.

Transaction costs during property transfers typically total 8-10% of property value, including capital gains tax, documentary stamp tax, and registration fees. These costs apply to both purchase and sale transactions, significantly impacting investment returns.

Condominium ownership includes monthly association dues, maintenance fees, and sinking fund contributions that vary by building quality and location. Premium buildings in Manila can command PHP 100-300 per square meter monthly in association dues.

Late payment penalties can reach 2% per month for overdue RPT payments, making timely payment crucial for cost control. Additional costs include property insurance, utility connections, and any required legal documentation for foreign ownership compliance.

It's something we develop in our Philippines property pack.

How do financing options work for foreigners and locals—interest rates, down payments, and loan terms?

Local Filipino buyers typically access financing with 10-20% down payments and current interest rates ranging from 5.75-8% annually for 10-20 year terms.

Foreign buyers face significantly stricter requirements including 20-30% down payments, more extensive income documentation, and often require residency or business visa status. Interest rates for foreigners range from 6-12% annually with maximum terms usually limited to 10-15 years.

Current market trends indicate interest rates are expected to decrease gradually, with forecasts suggesting rates may reach 4.75-5% by late 2025, improving overall affordability for qualified buyers.

Loan approval processes for foreigners can take 2-3 months versus 4-6 weeks for local buyers, requiring substantial financial documentation and often Philippine-based income sources or guarantors.

Alternative financing through developer arrangements sometimes offers more flexible terms for pre-construction purchases, though these typically require higher initial payments and carry completion risks.

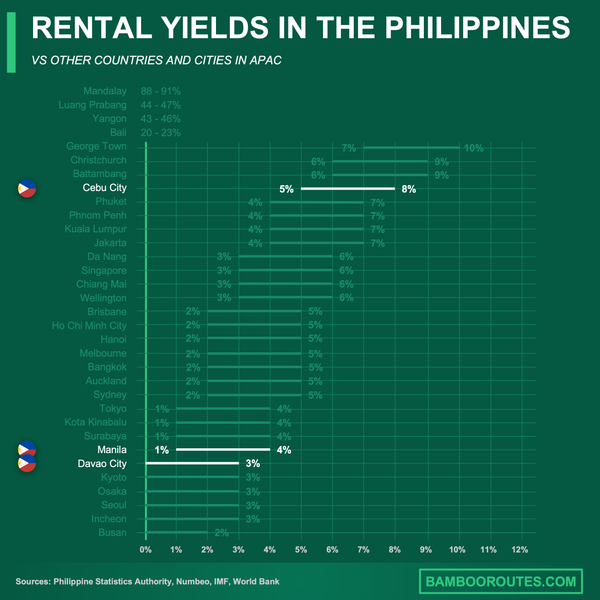

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

Which areas are showing the strongest infrastructure development or foreign investment that could boost property values?

The government's "Next Wave Cities" initiative targets Bulacan, Pampanga (Clark), Laguna, Iloilo, Bacolod, Cagayan de Oro, and Batangas for major infrastructure upgrades including roads, airports, and rail connections.

Metro Manila expansion areas including Quezon City, Caloocan, and Antipolo benefit from major transport projects including MRT and LRT extensions plus new expressway connections. These infrastructure improvements are creating new business districts and residential demand centers.

Clark Freeport Zone and surrounding Pampanga areas show particularly strong development momentum with airport expansion, new economic zones, and improved Manila connectivity driving property demand and price appreciation.

Foreign capital remains most active in luxury condominium projects, major mixed-use developments, and resort town properties as regulatory frameworks have become more investor-friendly in recent years.

Infrastructure completion timelines typically span 2-5 years, creating opportunities for early investment in areas with committed government funding and development partnerships already in place.

How do condos compare to houses or land in terms of risk, appreciation, and rental potential?

Condominiums offer the lowest entry barriers with higher rental yields and best liquidity profiles, making them suitable for foreign investors seeking regular income and easier exit strategies.

However, condos carry ongoing HOA dues and face greater supply risk, particularly in oversupplied urban markets. Management quality varies significantly between developments, affecting long-term value retention and rental competitiveness.

Houses and lots require higher initial investments and ongoing management costs but typically offer more stable long-term value appreciation, especially in suburban and regional markets. However, foreign ownership restrictions limit direct investment options to leasehold arrangements.

Land investments carry the highest risk for foreigners due to ownership restrictions requiring corporate structures, but offer the greatest long-term appreciation potential in growth corridors with infrastructure development.

Appreciation patterns favor emerging infrastructure corridors regardless of property type, with government development focus creating significant upside potential for early investors in targeted regions.

What's the minimum budget you need to enter each segment, and how should you position yourself if you're buying for living, renting out, or flipping?

1. **CBD Studio/1-Bedroom Condos**: USD 75,000-200,000 minimum, ideal for yield-focused investors seeking rental income and quick turnover opportunities.2. **Regional Mid-range Condominiums**: USD 40,000-80,000 entry point, suitable for long-term capital appreciation strategies in emerging markets.3. **Suburban Houses and Lots**: USD 60,000-125,000+ required, best for owner-occupants or family-oriented investment approaches.4. **Resort/Beachfront Properties**: USD 150,000+ minimum investment, targeting both rental income and capital appreciation in tourism markets.5. **Pre-construction Flip Projects**: USD 60,000-200,000+ depending on location, offering higher risk-reward profiles for experienced investors.For owner-occupancy, prioritize location convenience, future infrastructure development, and lifestyle amenities over pure investment returns. Rental-focused buyers should target small urban units in high-demand corridors with strong tenant markets and transportation access.

Flipping strategies work best with pre-sale purchases in areas with strong development pipelines, though these carry higher completion and market timing risks requiring careful due diligence.

Given today's market, is now a good time to buy—or is it smarter to wait?

The Philippines property market in September 2025 presents a split opportunity landscape depending on investment strategy and target markets.

Metro Manila prime segments currently show oversupply and elevated vacancy rates, creating negotiating leverage for buyers and potential bargain opportunities in previously overheated markets. However, short-term appreciation prospects remain limited in saturated urban areas.

Emerging regional markets and infrastructure-growth corridors present more compelling timing for long-term investors, as government development initiatives are actively reshaping value propositions in secondary cities.

Interest rate trends favor buyers with financing capacity, as rates are expected to decrease through 2025, improving affordability and potentially stimulating broader market demand.

For investors with 7-10 year holding periods targeting regional growth zones, current entry timing presents manageable risk profiles. Short-term speculators in crowded Metro Manila markets face significantly higher near-term risks given current oversupply conditions.

It's something we develop in our Philippines property pack.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

The Philippines property market in 2025 offers distinct opportunities for informed investors willing to navigate regulatory complexities and regional market variations.

Success depends on matching investment strategy with market conditions, understanding foreign ownership limitations, and timing entry points with infrastructure development cycles.

Sources

- BambooRoutes Philippines Price Forecasts

- Philippines 5-Year Real Estate Forecast

- Global Property Guide - Philippines Rental Yields

- Foreign Real Estate Ownership Restrictions

- Guide to Real Property Tax in Philippines

- Personal Home Loan for Foreigners

- Philippines Long Term Interest Rate

- Next Wave Cities Investment Report