Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Foreigners can buy condominiums and buildings in the Philippines, but land ownership remains strictly prohibited under Filipino law. Understanding these restrictions and the available workarounds is crucial for international investors looking to enter the Philippines property market. The legal framework allows strategic property ownership through specific structures while maintaining constitutional protections on land rights.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

Foreigners in the Philippines can legally own condominium units and buildings but cannot directly own land, requiring lease agreements or corporate structures for land access.

The property purchase process involves strict documentation, with typical costs including 1.5% documentary stamp tax, 6% capital gains tax, and various registration fees totaling 8-10% of property value.

| Property Type | Foreign Ownership Allowed | Key Restrictions |

|---|---|---|

| Condominium Units | Yes (Direct ownership) | Max 40% foreign ownership per project |

| Houses/Buildings | Yes (Building only) | Land must be leased or held through corporation |

| Land (Direct) | No | Strictly prohibited by constitution |

| Agricultural Land | No | Completely off-limits to foreigners |

| Land via Corporation | Limited | Corporation must be 60% Filipino-owned |

| Long-term Lease | Yes | 50 years + 25-year renewal option |

| Inherited Property | Limited | Must sell within specific timeframe |

What types of property can foreigners legally buy in the Philippines compared to locals, and what is strictly off-limits?

Foreigners in the Philippines can legally own condominium units and buildings but face strict restrictions on land ownership.

Condominium units represent the most straightforward option for foreign property ownership. Foreigners can directly purchase and hold title to condominium units, provided the total foreign ownership within the entire condominium project does not exceed 40%. This means once foreign ownership reaches this threshold, no additional units can be sold to non-Filipino citizens in that specific development.

Buildings, including houses and commercial structures, can be owned by foreigners, but only the structure itself—not the land underneath. This creates a unique ownership situation where the foreigner holds title to the building while the land must be acquired through alternative arrangements such as long-term lease agreements or corporate structures. Long-term leases allow foreigners to lease land for up to 50 years with an option to renew for an additional 25 years.

Corporate ownership provides another pathway, where foreigners can participate in land ownership through corporations that maintain at least 60% Filipino ownership. However, this arrangement is primarily used for business purposes rather than personal residences.

Direct land ownership remains completely prohibited for foreigners, including residential lots, farmland, and agricultural property. This constitutional restriction cannot be circumvented through any legal means for personal ownership.

Are there any exceptions, loopholes, or special cases where foreigners can own land or houses directly?

Several specific exceptions exist within Philippine law that allow limited land ownership rights for certain categories of foreigners.

Inheritance represents the most common exception, where foreigners may inherit land from a Filipino spouse or parent. However, this inherited property must typically be sold within a specific timeframe as dictated by law, and the foreigner cannot freely transfer or develop the inherited land without restrictions.

Marriage to a Filipino citizen creates opportunities for indirect land ownership. While the foreign spouse cannot hold title to land directly, the property can be registered in the Filipino spouse's name. The foreigner's name may appear in purchase contracts and agreements, but never on the actual land title itself.

Former Filipino citizens who acquired foreign citizenship have special privileges under the law. Natural-born Filipinos who became foreign citizens, along with their qualified heirs, can reacquire Filipino citizenship and own up to 1,000 square meters of urban land or 1 hectare of rural land for residential purposes. For business and agricultural purposes, they can own larger areas under strict regulatory limits.

Dual citizenship holders enjoy the same land ownership rights as Filipino citizens, provided they maintain valid Filipino citizenship status. This pathway requires formal reacquisition of Filipino citizenship through proper legal channels and maintaining compliance with both Philippine and foreign citizenship requirements.

It's something we develop in our Philippines property pack.

What residency, visa, or permit requirements apply to foreigners who want to buy or hold property long-term?

No specific visa or residency requirement is legally mandated for foreigners to purchase eligible property types in the Philippines.

For condominium purchases and long-term lease agreements, foreigners can complete transactions regardless of their visa status or residency situation. Tourist visa holders can legally purchase condominiums or enter into lease agreements for land use. The legal framework does not require permanent residency or specific long-term visa status for property ownership.

However, practical requirements often necessitate obtaining certain permits for smooth transaction processing. Tax Identification Numbers (TIN) are required for property purchases, and many banks and developers prefer clients to have Alien Certificate of Registration (ACR) for identification purposes. Long-term residents often find the Special Resident Retiree's Visa (SRRV) helpful for banking relationships and extended stays.

Property ownership does not automatically confer residency rights or visa privileges. Foreigners who purchase property must still comply with standard immigration requirements for their length of stay in the Philippines. Property ownership can support visa applications but does not guarantee approval for extended residence permits.

For ongoing property management and maintenance, having proper documentation simplifies dealings with banks, utilities, and local government offices. While not legally required for ownership, these permits facilitate the practical aspects of property ownership and management.

Do you need to be physically present in the Philippines to purchase or transfer property, or can it be done remotely?

Physical presence in the Philippines is not required for property purchase or transfer transactions.

Remote transactions can be conducted through a Special Power of Attorney (SPA) arrangement. This legal document allows a designated attorney-in-fact to act on behalf of the foreign buyer for all aspects of the property transaction. The SPA must be properly notarized and authenticated in the foreigner's home country, then apostilled or consularized for recognition in the Philippines.

The attorney-in-fact can be a lawyer, trusted individual, or authorized representative who handles document signing, payment processing, and title transfer procedures. This person has full legal authority to complete the purchase on behalf of the foreign buyer, including signing contracts, making payments, and receiving title documents.

Documentation requirements for remote transactions include certified copies of passports, proof of funds, tax identification numbers, and properly executed SPA documents. Banks typically require additional verification for overseas remittances and may request video conferences or additional authentication for large transactions.

While remote purchasing is legally possible, many foreigners choose to visit the Philippines for final inspections and document signing to ensure transaction security and property verification. Remote transactions require higher levels of trust in representatives and more comprehensive due diligence processes.

Don't lose money on your property in the Philippines

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What is the step-by-step process for a foreigner to buy property, and which documents are required at each stage?

The property purchase process for foreigners follows a structured seven-step procedure with specific documentation requirements at each stage.

- Due Diligence and Property Verification: Confirm developer legitimacy, verify clean title status, check for existing liens or encumbrances. Required documents include developer's business permits, title certificates, and property development approvals.

- Reservation Agreement: Reserve the specific unit or property by signing a reservation agreement and paying the reservation fee (typically 5-10% of property value). Documents needed include valid passport and initial proof of funds.

- Contract Signing: Execute the Deed of Sale or Contract to Sell with complete terms and conditions. Required documentation includes valid passport, visa documentation (if applicable), Tax Identification Number (TIN), proof of legitimate source of funds, and bank certifications.

- Payment Processing: Complete payment through official overseas remittance or local bank transfer. Documentation includes bank certificates, foreign exchange conversion records, and Bureau of Internal Revenue (BIR) remittance certificates.

- Title Transfer Preparation: Prepare final Deed of Absolute Sale with all supporting documents. Requirements include updated passport copies, Community Tax Certificate, proof of foreign remittance, visa or ACR documentation, and tax clearance certificates.

- Property Registration: Transfer title or Certificate of Ownership through Registry of Deeds or Condominium Corporation. Documentation includes notarized Deed of Absolute Sale, tax payment receipts, and all previous transaction records.

- Tax and Fee Settlement: Pay all required taxes and registration fees, including documentary stamp tax, capital gains tax, transfer tax, and registration fees. Final documentation includes all tax payment receipts and updated title certificates.

Is hiring a lawyer or legal representative mandatory, and if not, why is it strongly recommended?

Hiring a lawyer or legal representative is not legally mandatory for property purchases, but it is strongly recommended due to the complexity of Philippine property law and common fraud risks.

The Philippine property system involves intricate legal procedures, overlapping jurisdictions, and frequent regulatory changes that require professional legal interpretation. Lawyers ensure compliance with foreign ownership restrictions, proper document execution, and adherence to all regulatory requirements. They also verify that property purchases fall within legal parameters for foreign ownership.

Fraud and title issues are unfortunately common in the Philippine property market. Professional legal review helps identify potential scams, verifies legitimate ownership chains, and ensures clear property titles. Lawyers conduct thorough due diligence on developers, check for existing liens or legal disputes, and verify all documentation authenticity.

Legal representatives provide protection against contractual disputes and ensure proper understanding of terms and conditions. They negotiate favorable contract terms, explain complex legal provisions, and protect buyer interests throughout the transaction process. Professional legal guidance helps avoid costly mistakes and ensures proper legal recourse if problems arise.

The investment protection provided by legal representation far outweighs the cost, typically representing 1-2% of property value. This investment safeguards against potential losses from legal disputes, fraudulent transactions, or regulatory non-compliance that could result in property forfeiture or financial loss.

What taxes, government fees, and hidden costs should foreigners expect when buying and later reselling property?

Property transactions in the Philippines involve multiple taxes and fees that typically total 8-10% of the property value for purchase and 6-8% for resale.

| Fee Type | Rate | Paid By |

|---|---|---|

| Documentary Stamp Tax | 1.5% of property value | Buyer |

| Capital Gains Tax | 6% of higher value (zonal/selling price) | Seller (negotiable) |

| Transfer Tax | 0.5-0.75% (varies by city) | Buyer |

| Registration Fee | 0.25% of property value | Buyer |

| VAT (new properties) | 12% of selling price | Buyer |

| Notarial Fees | 0.1-0.5% of property value | Buyer |

| Legal Fees | 1-2% of property value | Buyer |

Additional ongoing costs include annual real estate taxes (typically 0.25-2% of assessed value), homeowners' association dues for condominiums (₱3,000-₱15,000 monthly), and property insurance premiums. These recurring expenses must be factored into long-term ownership calculations.

Hidden costs often include processing fees, courier charges, title insurance, survey fees, and miscellaneous government charges that can add 1-2% to transaction costs. Bank financing, if available, includes loan processing fees, appraisal costs, and mortgage insurance premiums.

Can foreigners access mortgages in the Philippines, and if so, what are the typical rates, conditions, and best strategies to secure one?

Very few Philippine banks offer mortgages to foreigners, and those that do have extremely strict requirements and limited property eligibility.

As of September 2025, mortgage rates for foreign buyers range from 7-10% annually, significantly higher than rates offered to Filipino citizens. Loan-to-value ratios are typically limited to 60-70% for foreigners, requiring substantial down payments of 30-40% of property value. Most banks require Filipino co-borrowers or guarantors for foreign applicants.

Eligible properties are limited to condominiums and buildings with clear foreign ownership rights. Banks will not finance land purchases or properties with complex ownership structures. Pre-selling units often have different financing requirements compared to ready-for-occupancy properties.

Requirements typically include proof of overseas income, employment certification, bank statements showing consistent income flow, valid visa or residency documentation, and often a local Filipino guarantor. Processing times are extended, often taking 3-6 months compared to 30-45 days for Filipino applicants.

Developer financing represents a more accessible option, though with higher interest rates (8-12%) and shorter terms (5-10 years versus 20-30 years for bank loans). In-house financing from reputable developers often provides more flexible requirements and faster processing times.

Most foreign buyers choose cash purchases or arrange financing in their home countries to avoid Philippine banking complications. This approach provides more negotiating power and faster transaction completion.

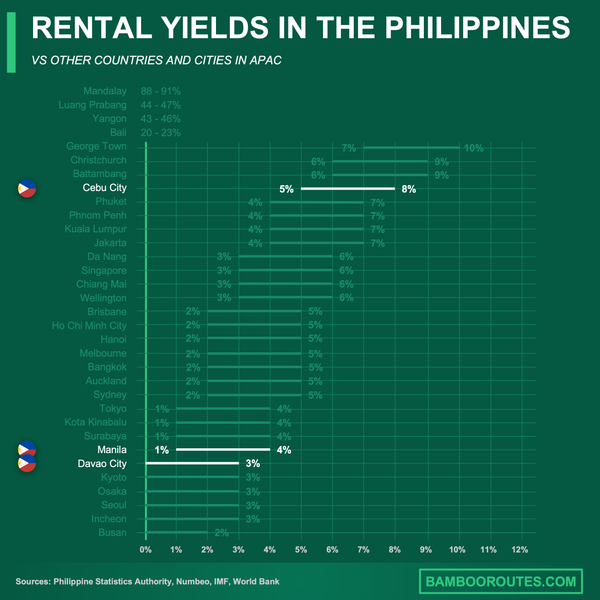

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

Which cities or regions are considered the best for foreigners to live in, and where do they usually settle?

Metro Manila dominates foreign settlement patterns, with Makati, Bonifacio Global City (BGC), and Ortigas Center serving as primary hubs for international residents.

Makati remains the financial capital and most popular destination for business-focused expatriates. The city offers extensive international amenities, premium condominiums, world-class shopping, and established expat communities. Bonifacio Global City attracts younger professionals and families with its modern infrastructure, international schools, and contemporary lifestyle offerings.

Cebu City and Mactan Island serve as the second-largest foreign population center outside Manila. The region's thriving IT and business process outsourcing sectors, combined with lower living costs and proximity to beaches and resorts, make it attractive for both working expatriates and retirees. Cebu IT Park specifically caters to technology professionals and offers high-quality urban amenities.

Davao City appeals to retirees and those seeking a quieter lifestyle while maintaining urban conveniences. The city's reputation for safety, affordable cost of living, and proximity to natural attractions makes it popular among American and Australian retirees. Baguio offers cool climate advantages and attracts those preferring temperate weather conditions.

Subic Bay, Clark in Pampanga, and Tagaytay provide suburban alternatives with peaceful environments, golf courses, and cooler climates. These areas particularly attract retirees and those seeking weekend retreat properties while maintaining accessibility to Manila.

It's something we develop in our Philippines property pack.

What areas currently rank highest for rental yields, tourism-driven demand, livability, and long-term capital appreciation?

Metro Manila's business districts consistently deliver the highest rental yields and strongest capital appreciation potential for foreign property investors.

Makati and Bonifacio Global City generate rental yields of 6-8% annually for well-located condominium units. These areas benefit from consistent demand from multinational corporations, financial institutions, and expatriate professionals willing to pay premium rents for quality accommodation. The established infrastructure and premium positioning support strong long-term appreciation prospects.

Cebu IT Park and surrounding areas offer attractive rental yields of 7-9% due to the expanding business process outsourcing sector and growing IT industry presence. The combination of local professional demand and tourism activity creates diverse rental income opportunities. Mactan Island properties benefit from both long-term rental demand and short-term vacation rental potential.

Tourism-driven markets show strong seasonal performance but require careful management. Boracay, Palawan (specifically El Nido and Coron), and Bohol properties command premium rates during peak tourist seasons but experience significant seasonality. These markets work best for investors comfortable with vacation rental management or seasonal occupancy patterns.

Clark and Pampanga present emerging opportunities with infrastructure development and proximity to Manila driving capital appreciation. The area's transformation from former military base to economic zone creates long-term growth potential, though rental yields currently remain moderate at 5-7%.

Tagaytay offers lifestyle investment opportunities with moderate rental yields of 4-6% but strong appeal for weekend and vacation rentals targeting Manila residents seeking cooler climate retreats.

What is the current breakdown of property prices per city and region, including both affordable and high-demand markets?

As of September 2025, property prices in the Philippines show significant variation between Metro Manila's premium markets and more affordable regional cities.

| Location | Entry-Level Condos (per sqm) | Premium Properties (per sqm) |

|---|---|---|

| Makati/BGC (Manila) | ₱200,000-₱300,000 | ₱400,000-₱600,000+ |

| Ortigas (Manila) | ₱120,000-₱200,000 | ₱250,000-₱400,000 |

| Cebu City/IT Park | ₱80,000-₱130,000 | ₱160,000-₱250,000 |

| Davao City | ₱45,000-₱80,000 | ₱100,000-₱150,000 |

| Clark/Pampanga | ₱60,000-₱100,000 | ₱120,000-₱180,000 |

| Boracay/Palawan | ₱150,000-₱250,000 | ₱300,000-₱500,000 |

| Baguio | ₱70,000-₱120,000 | ₱150,000-₱220,000 |

Metro Manila's premium markets in Makati and BGC command the highest prices, with luxury developments reaching ₱600,000+ per square meter for prime locations with Manila Bay or city views. These prices reflect international-standard amenities, premium locations, and strong rental demand from multinational corporations.

Regional cities offer significantly more affordable entry points, with Davao and smaller cities providing opportunities under ₱100,000 per square meter for quality developments. However, these markets typically have lower rental yields and more limited resale liquidity compared to Metro Manila properties.

Tourist destination pricing reflects location premiums, with beachfront or resort-integrated properties commanding prices comparable to Metro Manila despite lower local income levels. These properties rely on tourism demand and seasonal rental income rather than local economic fundamentals.

What are the classic mistakes and pitfalls foreigners often face when buying or owning property in the Philippines, and how can they be avoided?

The most common and costly mistake involves attempting direct land ownership under foreign names, which violates Philippine constitutional law and can result in property forfeiture.

- Inadequate Developer Due Diligence: Many foreigners fail to properly investigate developer credentials, leading to investments in projects with poor construction quality, delayed completion, or questionable legal status. Always verify business permits, previous project completion records, and financial stability before investing.

- Misunderstanding Condominium Ownership Rules: Buyers often overlook the 40% foreign ownership limit per project or invest in "condo hotels" that don't meet true condominium legal requirements. Verify current foreign ownership percentages and ensure properties qualify as legitimate condominiums under Philippine law.

- Skipping Professional Legal Review: Attempting to navigate complex property transactions without qualified legal representation frequently results in contract disputes, title issues, or regulatory non-compliance. Always engage reputable local lawyers specializing in foreign property transactions.

- Underestimating Total Cost of Ownership: Many buyers focus only on purchase price while underestimating taxes, maintenance fees, association dues, and ongoing expenses. Budget for 8-10% in transaction costs and 3-5% annually in maintenance and taxes.

- Relying on Unlicensed Intermediaries: Working with unofficial agents or brokers without proper credentials often leads to fraudulent transactions or legal complications. Only work with licensed real estate professionals and verified developers with established track records.

Prevention strategies include comprehensive due diligence, professional legal representation, understanding all ownership restrictions, proper financial planning for total ownership costs, and working exclusively with licensed, reputable professionals throughout the transaction process.

It's something we develop in our Philippines property pack.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

Foreign property ownership in the Philippines requires careful navigation of constitutional restrictions and legal frameworks that protect Filipino land rights while allowing strategic investment opportunities for international buyers.

Success in the Philippine property market depends on understanding ownership limitations, working with qualified professionals, and choosing appropriate investment structures that comply with local laws while meeting investment objectives.

Sources

- Respicio Law - Property Ownership for Foreigners in the Philippines

- Veles Club - Philippine Property Investment Guide

- Respicio Law - Foreigner Acquiring Land in the Philippines

- Aurelia Residences - Can Foreigner Own Condo in Philippines

- TransferGo - Buying Property in the Philippines

- Dayanan Consulting - Foreign Ownership Land Philippines

- Mandani Bay - Can Foreigner Buy Property in Philippines

- Juwai Asia - Philippines Property Investment Guide