Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

The Philippines property market is experiencing robust growth with Metro Manila leading price appreciation at 13.9% year-on-year in Q1 2025. Secondary cities like Cebu and Davao offer compelling investment opportunities with higher rental yields and significant infrastructure-driven growth potential.

As of September 2025, the Philippine real estate landscape presents diverse opportunities across different market segments and regions. While Metro Manila commands premium pricing with luxury condos averaging PHP 203,360 per square meter, secondary cities like Cebu and Davao provide attractive entry points with strong fundamentals and projected annual growth of 3-7% over the next three years.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

Metro Manila luxury condos average PHP 203,360 per sqm while Cebu and Davao offer more affordable entry points with higher rental yields. The national residential price index rose 7.6% year-on-year in Q1 2025, with Metro Manila outpacing provinces at 13.9% growth.

Infrastructure projects including the Metro Manila Subway and Mindanao Railway are driving property value appreciation, while robust pipeline developments and 92% occupancy rates in secondary cities indicate strong market fundamentals across the archipelago.

| Market Indicator | Metro Manila | Cebu/Davao | Forecast 2025-2028 |

|---|---|---|---|

| Average Price per sqm | PHP 203,360 (luxury) | PHP 75,000-200,000 | 3-7% annual growth |

| Rental Yields | 4.5-6% | 6-8% | Stable to improving |

| Occupancy Rates | 93.3% (prime districts) | 92% (Davao) | Sustained high demand |

| Price Growth (Y-o-Y) | 13.9% | 3-7% | Moderate expansion |

| Infrastructure Impact | Subway, rail projects | Bypass, expressways | High value appreciation |

What are the current property prices per square meter in Metro Manila compared to Cebu and Davao?

Metro Manila luxury condominiums command the highest prices in the Philippines, averaging PHP 203,360 per square meter in central business districts as of Q1 2025.

Cebu City presents a more diverse pricing structure with prime condominiums in areas like Ayala and IT Park reaching PHP 170,000-230,000 per square meter. However, properties in secondary locations within Cebu start around PHP 75,000 per square meter, making it accessible for different budget ranges.

Davao City offers the most affordable entry point among major Philippine cities, with houses averaging PHP 45,600 per square meter. Condominium units in Davao typically range from PHP 40,000-90,000 per square meter, with complete units priced between PHP 3-5 million.

The price differential between these cities creates distinct investment opportunities. Metro Manila attracts premium investors seeking established markets, while Cebu and Davao appeal to those looking for growth potential at lower entry costs.

It's something we develop in our Philippines property pack.

How much have property prices grown in the past five years and what's the forecast for the next three years?

The Philippine residential property market has demonstrated strong price appreciation, with the national residential index rising 7.6% year-on-year in Q1 2025, though this represents a moderation from the 9.8% growth recorded in Q4 2024.

Metro Manila significantly outpaced provincial markets with a robust 13.9% price increase year-on-year, reflecting continued demand concentration in the capital region. This growth rate positions Metro Manila among the fastest-appreciating property markets in Southeast Asia.

Cebu has maintained steady annual growth of 3-5% for condominiums over recent years, with suburban landed properties showing stronger performance at 6-8% annually over the past decade. Davao recorded more moderate growth of 3% for houses and 5-7% for condominiums in 2024-2025.

The three-year forecast indicates continued positive momentum with Cebu and Davao projected to sustain 3-7% annual growth through 2028. Metro Manila is expected to moderate but remain positive as expanding supply balances with sustained demand from both domestic and overseas Filipino workers.

Infrastructure investments and urban population growth support these projections, making the Philippine property market attractive for medium-term investment strategies.

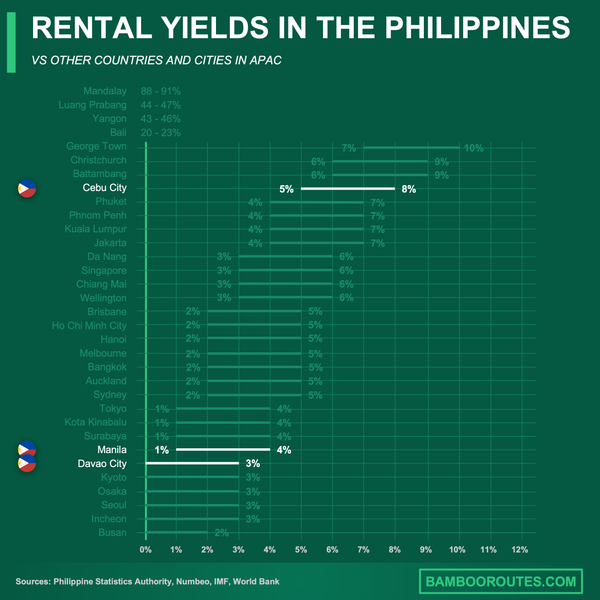

What are the current rental yields for condos and houses, and how do they compare to Southeast Asian averages?

Metro Manila condominium rental yields average 5.1-5.2% gross returns as of 2025, with high-end units in Makati and Bonifacio Global City ranging from 4.5% to 6%.

Cebu offers more attractive rental yields at 6-8% for studio and compact condominiums in prime locations, particularly benefiting from strong demand from business process outsourcing workers. This higher yield compensates for lower absolute property values and attracts yield-focused investors.

Davao rental yields, while not explicitly detailed in current data, are implied to be similar to or slightly below Cebu levels due to lower base prices but rising tenant demand from the city's economic expansion.

Compared to regional Southeast Asian markets, Philippine yields are competitive but generally positioned in the middle range. Thailand's Bangkok averages 6.1% rental yields, while Vietnam offers 5-7% in major cities. However, Philippine yields typically fall below higher-yielding markets like Phnom Penh, which exceeds 7%.

The yield differential between Metro Manila and secondary cities creates opportunities for investors to balance capital appreciation potential against immediate income generation based on their investment objectives.

How many new residential and commercial units are expected to be completed in the next 12-24 months?

Metro Manila faces a robust residential pipeline extending through 2028, though development delays have shifted major completions from early 2025 to late 2025-2027.

Q2 2025 demonstrated positive net absorption despite no new completions, indicating strong underlying demand. Major handovers are expected from late 2025 onward, concentrated in established districts including Makati, Taguig, and Ortigas.

Commercial development shows significant expansion with 139,000 square meters of office space and 151,000 square meters of retail space scheduled for delivery by 2026. This commercial pipeline extends beyond Metro Manila to include substantial projects in Cebu, Davao, and emerging secondary cities.

Regional development is accelerating with significant new projects planned for Pampanga, Batangas, Laguna, Bacolod, and Iloilo. These secondary city developments are often positioned as more affordable alternatives or targeting higher rental income potential.

The pipeline concentration in multiple regions rather than solely Metro Manila reflects the market's geographic diversification and infrastructure-driven expansion into previously underserved areas.

Don't lose money on your property in the Philippines

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What are the current occupancy rates for condominiums and office spaces in major cities?

Davao City demonstrates exceptional condominium market strength with a 92% occupancy rate as of mid-2025, indicating robust tenant demand and limited available inventory.

Metro Manila prime condominium districts report improving fundamentals with vacancy rates declining to 6.7% in Q2 2025, driven by healthy absorption in Makati and Taguig. However, aggregate residential vacancy across Metro Manila may rise to historic highs of 26% as major supply deliveries come online.

Office space occupancy presents mixed signals with vacancy rates remaining elevated in Manila due to headwinds from Philippine Offshore Gaming Operator exits. However, leasing activity remains resilient in top central business districts.

Demand for office space outside Metro Manila is rising significantly due to business process outsourcing expansion into secondary cities, creating opportunities in regional markets like Cebu and Davao.

The occupancy rate differential between established prime districts and emerging areas highlights the importance of location selection and timing in Philippine property investments.

How much foreign direct investment has entered the Philippine real estate sector recently?

Foreign direct investment in Philippine real estate remains substantial, though specific 2025 figures require current market analysis beyond the available data.

The real estate sector continues attracting overseas Filipino investors and foreign institutional capital, particularly in pre-selling phases and mixed-use township projects. These investments demonstrate confidence in long-term market fundamentals.

Business process outsourcing expansion, tourism recovery, and infrastructure development support steady to moderate incremental FDI increases. Foreign investment focuses heavily on commercial and mixed-use developments rather than purely residential projects.

Institutional investors show particular interest in Real Estate Investment Trust opportunities as the government continues liberalizing REIT regulations to attract foreign capital.

The expected trend indicates stable foreign investment flows with potential for growth as infrastructure projects mature and regulatory frameworks become more investor-friendly.

What are the current mortgage interest rates and how do they compare historically?

Philippine bank mortgage rates in 2025 typically range from 6-8% per annum for prime borrowers, representing a significant increase from pre-pandemic levels.

These current rates are notably higher than the 5-6% range common during 2017-2019, reflecting global monetary tightening and domestic economic conditions. However, they remain well below the double-digit rates experienced in previous decades.

The interest rate environment affects affordability calculations and investment returns, particularly for leveraged property purchases. Higher rates have moderated some buyer demand while potentially creating opportunities for cash buyers.

Banks maintain selective lending criteria, with prime borrowers accessing lower rates while average borrowers face the higher end of the range. Foreign buyers typically encounter additional documentation requirements and potentially higher rates.

Interest rate trends will significantly influence property market dynamics, with any future rate reductions likely to stimulate renewed buying activity across all market segments.

What percentage of household income goes toward housing costs compared to other ASEAN countries?

Households in Metro Manila typically allocate 28-35% of disposable income to housing costs, whether mortgage payments or rent, positioning the Philippines in the higher range among ASEAN nations.

This housing cost burden is slightly elevated compared to regional peers, with Malaysia, Thailand, and Vietnam commonly citing 25-32% of income dedicated to housing expenses. The differential reflects both higher property prices and income levels in Philippine urban centers.

Rising property prices and elevated interest rates continue challenging affordability for lower-income segments, particularly first-time buyers seeking entry into major urban markets.

The affordability challenge creates market segmentation, with middle and upper-income households accessing prime locations while lower-income buyers seek opportunities in peripheral areas or secondary cities.

Government initiatives targeting affordable housing aim to address this gap, though implementation and market impact remain gradual processes requiring sustained policy commitment.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

What are the projected population growth and urban migration trends over the next decade?

The Philippines population is projected to reach approximately 129 million by 2035, representing sustained demographic growth that fundamentally supports housing demand.

Continued urbanization will see Manila, Cebu, Davao, and emerging regional growth centers absorbing the majority of new arrivals from rural areas. This migration pattern concentrates housing demand in areas with existing infrastructure and employment opportunities.

Urban migration particularly benefits secondary cities as businesses seek lower costs and government policies encourage development outside Metro Manila. Cities like Iloilo, Bacolod, and Cagayan de Oro are experiencing increased attention from both residents and developers.

The demographic trend sustains high housing demand across all market segments, with particular pressure on affordable and mid-market brackets where new urban residents typically enter the property market.

Population growth combined with rising income levels creates a expanding pool of potential property buyers and tenants, supporting long-term market fundamentals across the archipelago.

What government policies and reforms are currently influencing the property market?

The government has increased VAT-exempt thresholds for affordable housing projects, making lower-priced units more accessible to budget-conscious buyers while encouraging developer participation in this segment.

Incentives for business process outsourcing office construction support commercial real estate development, particularly in secondary cities where BPO companies are expanding operations to access talent pools and reduce costs.

Real Estate Investment Trust liberalization continues fostering commercial and mixed-use development by providing developers with additional financing options and investors with liquid real estate exposure.

Planned reforms include further REIT liberalization, streamlined permit processes, and expanded investment incentives for townships outside Metro Manila. These legislative initiatives aim to distribute development more evenly across the country.

Foreign ownership restrictions remain in place with non-citizens limited to condominium purchases and long-term leases rather than direct land ownership, though no outright purchase bans affect the condominium market.

How does the supply-demand balance look across different housing segments?

| Housing Segment | Current Supply-Demand Balance | Growth Potential | Key Characteristics |

|---|---|---|---|

| Luxury | Balanced to slight oversupply | Moderate | Steady demand in prime districts, high foreign/expat interest |

| Mid-Range | Well-balanced | Strong | Largest segment, driven by OFW families and middle class |

| Affordable | Significantly undersupplied | Highest | Limited by regulatory and funding constraints |

| Commercial | Expanding supply | Moderate to strong | BPO expansion driving demand |

| Mixed-Use | Growing supply | Strong | Township developments gaining popularity |

What infrastructure projects are impacting property values in surrounding areas?

The Metro Manila Subway system represents the most significant infrastructure investment affecting property values, with stations creating appreciation zones extending several kilometers from each stop.

North-South Commuter Rail and other railway projects are transforming accessibility between Metro Manila and surrounding provinces, making previously distant areas viable for residential development and investment.

The Mindanao Railway project in Davao and surrounding regions is driving property speculation and development along planned routes, with early investors positioning for infrastructure completion benefits.

New airports in Bulacan and Clark are creating entirely new property markets as accessibility improves and commercial activities expand around these transportation hubs. Properties within 30 kilometers of these facilities are experiencing increased investor interest.

Regional infrastructure including the Davao Bypass, Cebu-Cordova Link Expressway, and Batangas Port upgrades are transforming regional accessibility and creating localized property appreciation zones.

It's something we develop in our Philippines property pack.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

The Philippine property market offers compelling opportunities across diverse segments and regions, with Metro Manila providing established premium markets while secondary cities like Cebu and Davao present higher yields and growth potential.

Infrastructure investments, demographic trends, and policy reforms create a supportive environment for sustained property market expansion, though careful location selection and market timing remain critical for investment success.

It's something we develop in our Philippines property pack.

Sources

- Philippines Price Forecasts

- Cebu Real Estate Prices 2025 Market Update

- Davao City Price Forecasts

- Cebu Price Forecasts

- Manila Expects Robust Residential Supply Pipeline Until 2028

- Emerging Cities Philippines Real Estate 2025

- Property Price Growth Cools Q1 Demand Wanes

- Philippines 5-Year Real Estate Forecast

-How Much Does Property Cost in the Philippines

-The Philippines Property Taxes and Fees

-Average Property Prices in the Philippines

-Average Land Price per Square Meter in Philippines

-Average Rental Yields in the Philippines

-Title Deeds in the Philippines