Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Buying property in the Philippines in 2026 involves several taxes, professional fees, and registration costs that foreign buyers need to budget for on top of the purchase price.

We constantly update this blog post to reflect the latest regulations and market conditions in the Philippines.

Understanding these costs upfront helps you avoid surprises and negotiate better deals when purchasing residential property in the Philippines.

And if you're planning to buy a property in this place, you may want to download our pack covering the real estate market in the Philippines.

Overall, how much extra should I budget on top of the purchase price in the Philippines in 2026?

How much are total buyer closing costs in the Philippines in 2026?

As of early 2026, foreign buyers purchasing residential property in the Philippines should expect total closing costs of around 3% to 5.5% of the purchase price, which translates to roughly ₱300,000 to ₱550,000 (about $5,300 to $9,700 or €4,900 to €9,000) for every ₱10 million spent.

The minimum extra budget possible in the Philippines is around 2.3% to 3.2% of the purchase price (approximately ₱230,000 to ₱320,000 or $4,000 to $5,600 or €3,700 to €5,200 per ₱10 million) if you keep legal fees lean and buy in a lower-tax locality with clean paperwork.

The maximum extra budget you should realistically plan for is 6% to 9% of the purchase price (approximately ₱600,000 to ₱900,000 or $10,500 to $15,800 or €9,700 to €14,600 per ₱10 million), especially if VAT applies, you need extensive legal due diligence, or withholding tax mechanics add cash handling complexity.

Your closing costs in the Philippines fall at the low end when paperwork is clean, the locality has lower transfer tax rates, and you need minimal legal support, while they land at the high end when you buy from a VAT-registered developer, require translations, or face ordinary asset tax treatment.

What's the usual total % of fees and taxes over the purchase price in the Philippines?

The usual total percentage of fees and taxes over the purchase price in the Philippines in 2026 is around 3% to 5.5%, with most foreign buyers landing somewhere near 5% as a safe planning rule.

The realistic low-to-high percentage range that covers most standard residential property transactions in the Philippines is 2.3% at the absolute minimum to about 9% in more complex situations involving VAT or extensive professional services.

Of that total percentage, government taxes (Documentary Stamp Tax, LGU transfer tax, and registration fees) typically account for about 2.3% to 3.25%, while professional service fees (notary, legal, and broker if applicable) make up the remaining 0.5% to 2% or more depending on what services you need.

By the way, you will find much more detailed data in our property pack covering the real estate market in the Philippines.

What costs are always mandatory when buying in the Philippines in 2026?

As of early 2026, the mandatory costs when buying property in the Philippines include Documentary Stamp Tax (about 1.5%), LGU transfer tax (0.5% to 0.75%), Registry of Deeds registration and annotation fees (0.3% to 1%), certified true copies of documents, and notarization of the deed of sale.

Optional but highly recommended costs for foreign buyers in the Philippines include hiring an independent lawyer for due diligence (especially helpful for foreigners navigating Special Power of Attorney requirements), professional title and lien checks, tax clearance verification, property valuation, and translation or interpreter services if you are not comfortable signing documents in Filipino or English legal wording.

Don't lose money on your property in the Philippines

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What taxes do I pay when buying a property in the Philippines in 2026?

What is the property transfer tax rate in the Philippines in 2026?

As of early 2026, the property transfer tax (called LGU transfer tax) in the Philippines ranges from 0.5% in provinces to 0.75% in Metro Manila cities and other highly urbanized areas, calculated on the higher of the selling price or the property's fair market value.

There are no extra transfer taxes specifically for foreigners buying property in the Philippines, as the transfer tax is tied to the property and locality rather than the buyer's nationality (though foreigners do face ownership restrictions on land, which is a separate legal matter).

Buyers may pay 12% VAT on residential property purchases in the Philippines when the seller is a VAT-registered developer or real estate business and the sale price exceeds the VAT-exempt threshold of ₱3.6 million for houses and residential dwellings, though this VAT is often already included in the developer's quoted price.

The Philippines does not use the term "stamp duty" but has Documentary Stamp Tax (DST), which buyers typically pay at around 1.5% of the property's tax base value when executing the deed of sale or conveyance.

Are there tax exemptions or reduced rates for first-time buyers in the Philippines?

There is no broad automatic tax exemption or reduced rate specifically for first-time property buyers in the Philippines for DST or LGU transfer tax, unlike some European countries that offer first-time buyer programs.

If you buy property through a company in the Philippines instead of as an individual, you may trigger a more commercial tax analysis with different withholding and compliance requirements, and the transaction could fall under "ordinary asset" treatment if the company is engaged in real estate business.

There is often a tax difference between buying new-build versus resale property in the Philippines, as new-build purchases from VAT-registered developers are more likely to include VAT (if above ₱3.6 million), while resale transactions between individuals typically only involve DST, LGU transfer tax, and registration fees without VAT.

Since there is no standard first-time buyer exemption in the Philippines, there are no specific documentation or conditions to meet, but buyers should verify whether VAT exemption thresholds apply to their purchase by confirming the property type and price with the seller or developer.

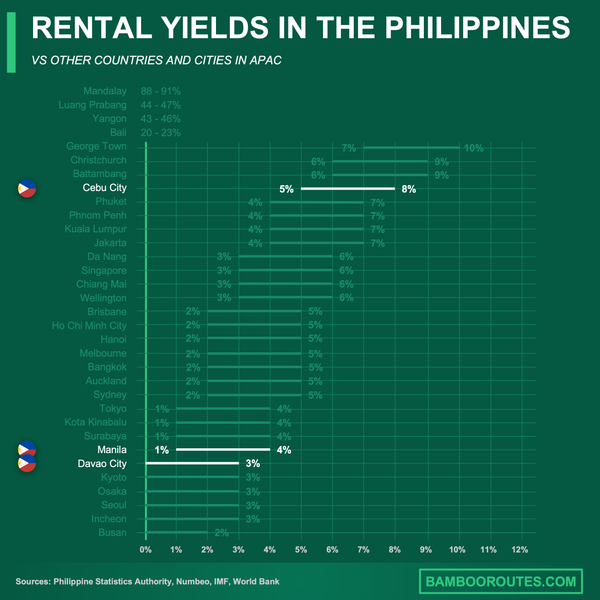

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you’re planning to invest there.

Which professional fees will I pay as a buyer in the Philippines in 2026?

How much does a notary or conveyancing lawyer cost in the Philippines in 2026?

As of early 2026, notary and conveyancing lawyer fees in the Philippines typically range from 0.5% to 1.5% of the property price for full legal support (approximately ₱50,000 to ₱150,000 or $880 to $2,600 or €810 to €2,430 on a ₱10 million property), while basic notarization alone may cost 0.1% to 0.5% with minimum peso fees.

Notary and lawyer fees in the Philippines are typically charged as a percentage of the property price for full conveyancing services, though some lawyers offer flat-rate packages for basic notarization or specific tasks like title verification.

Translation or interpreter services for foreign buyers in the Philippines typically cost ₱2,000 to ₱10,000 ($35 to $175 or €32 to €160) per document for written translations and ₱3,000 to ₱8,000 ($53 to $140 or €49 to €130) per day for an interpreter at signing, with Metro Manila prices often at the higher end.

A tax advisor is recommended for foreign buyers in the Philippines when the transaction involves VAT, ordinary asset classification, or rental income planning, with typical consultation fees ranging from ₱15,000 to ₱50,000 ($260 to $880 or €240 to €810) for a focused transaction review.

We have a whole part dedicated to these topics in our our real estate pack about the Philippines.

What's the typical real estate agent fee in the Philippines in 2026?

As of early 2026, the typical real estate agent or broker commission in the Philippines ranges from 2.5% to 5% of the sale price, which translates to approximately ₱250,000 to ₱500,000 ($4,400 to $8,800 or €4,050 to €8,100) on a ₱10 million property.

In the Philippines, the seller typically pays the real estate agent or broker fee, but buyers who hire their own buyer's agent can agree to a separate buyer-side fee, and developer sales often have commissions built into the price.

The realistic low-to-high range for agent fees in the Philippines is 2.5% at the minimum (common for straightforward transactions) to 5% at the higher end (often seen with full-service brokers or premium properties), and this is always negotiable.

How much do legal checks cost (title, liens, permits) in the Philippines?

Legal checks including title search, liens verification, tax declaration copies, and basic clearances in the Philippines typically cost ₱5,000 to ₱25,000 ($88 to $440 or €81 to €405), with more complex situations involving inheritance history or boundary issues costing more.

Property valuation or appraisal fees in the Philippines typically range from ₱5,000 to ₱20,000 ($88 to $350 or €81 to €325), depending on the property's location and complexity, and are often required when financing or verifying the deal price against comparable sales.

The most critical legal check that foreign buyers should never skip in the Philippines is verifying the title at the Registry of Deeds, including checking for liens, encumbrances, and confirming the seller's authority to sell, as title fraud and documentation issues are real risks.

Buying a property with hidden issues is something we mention in our list of risks and pitfalls people face when buying real estate in the Philippines.

Get the full checklist for your due diligence in the Philippines

Don't repeat the same mistakes others have made before you. Make sure everything is in order before signing your sales contract.

What hidden or surprise costs should I watch for in the Philippines right now?

What are the most common unexpected fees buyers discover in the Philippines?

The most common unexpected fees foreign buyers discover in the Philippines include sellers asking buyers to shoulder the 6% capital gains tax (which is technically a seller cost), unpaid real property tax arrears that block registration, condo association dues or special assessments in arrears, move-in or turnover fees, and withholding tax remittance requirements in ordinary asset transactions.

Yes, unpaid property taxes or debts can become your problem in the Philippines, not because you legally inherit them, but because outstanding real property tax arrears can block your ability to register the title cleanly, so always demand updated tax clearances before closing.

Scams with fake listings and fake fees do occur in the Philippines, including fake reservation fees paid to non-owners and pressure to sign without verified title documents, so your protection is to verify the title chain, confirm the seller's authority, only pay against official receipts, and use escrow or lawyer-managed closing.

Fees usually not disclosed upfront by sellers or agents in the Philippines include condo move-in and turnover fees, association dues arrears, document procurement and certification costs, and informal "liaison" fees that appear when paperwork has complications.

In our property pack covering the property buying process in the Philippines, we go into details so you can avoid these pitfalls.

Are there extra fees if the property has a tenant in the Philippines?

Extra fees when buying a tenanted property in the Philippines can include legal costs for lease assignment documentation (approximately ₱5,000 to ₱15,000 or $88 to $260 or €81 to €240), proration of rent and deposits, and potentially higher lawyer fees for reviewing the existing lease terms.

When purchasing a tenanted property in the Philippines, the buyer inherits the existing lease agreement and must honor its terms until expiration, including the tenant's right to occupy and any rent amounts or conditions already agreed upon.

Terminating an existing lease immediately after purchase in the Philippines is generally not possible unless the lease has a valid termination clause you can invoke, the tenant agrees to leave, or you have legal grounds for eviction under the lease terms or law.

A sitting tenant in the Philippines can affect the property's market value both positively (guaranteed rental income) and negatively (limited flexibility), and it often gives you negotiating leverage on price if the tenant situation is seen as a complication by other buyers.

If you want to optimize your rental strategy, you can read our complete guide on how to buy and rent out in the Philippines.

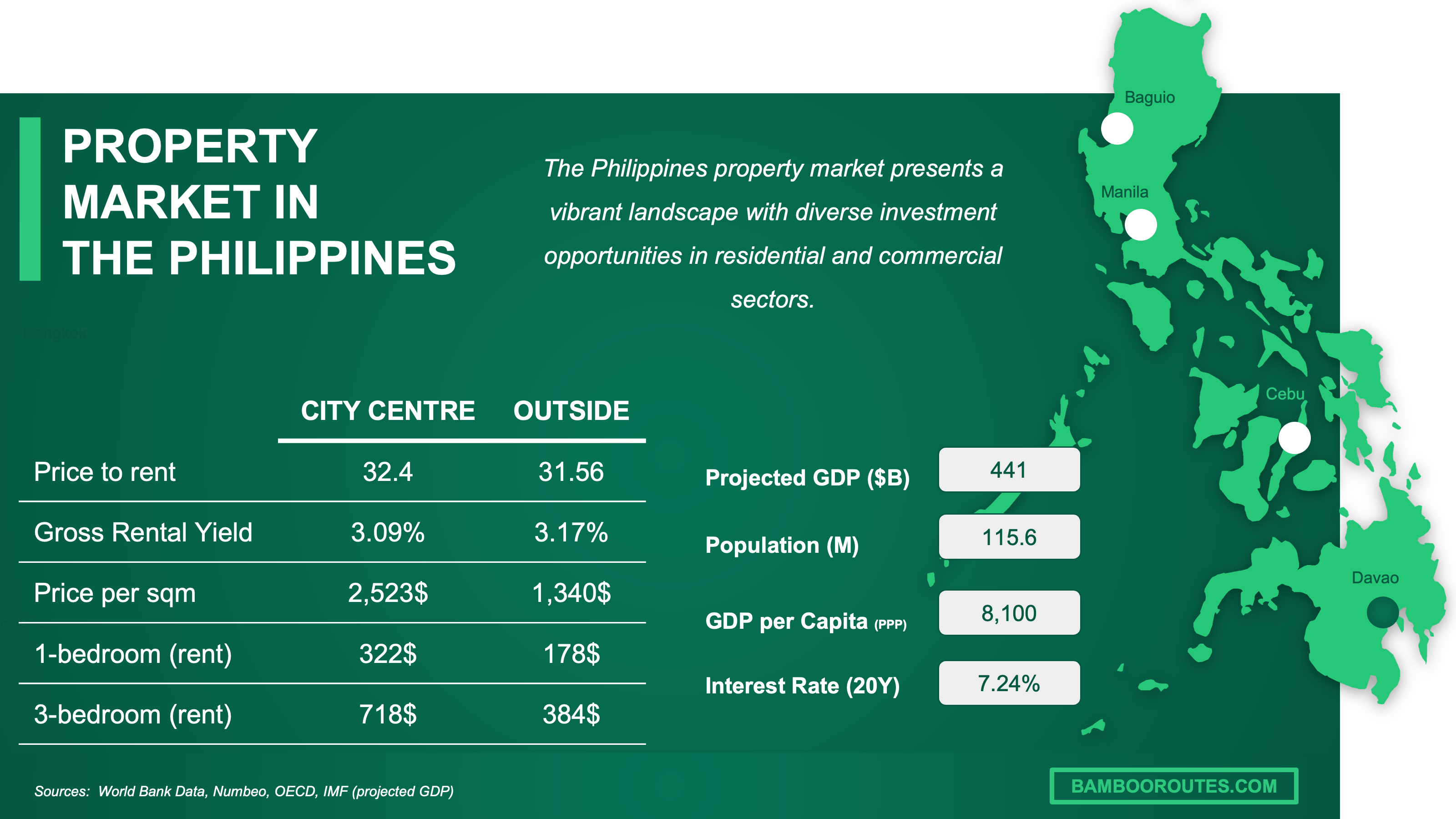

We have made this infographic to give you a quick and clear snapshot of the property market in the Philippines. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Which fees are negotiable, and who really pays what in the Philippines?

Which closing costs are negotiable in the Philippines right now?

Closing costs that are negotiable in the Philippines include who pays Documentary Stamp Tax, who pays LGU transfer tax, who pays registration and annotation fees, broker commission allocation between buyer and seller, and legal and notary fee rates and scope.

Closing costs that are fixed by law and cannot be negotiated in the Philippines include the actual tax rates (1.5% DST rate, the LGU transfer tax percentage set by the locality, and registration fee schedules), though you can negotiate who bears the cost rather than the rate itself.

The typical discount or reduction buyers can realistically achieve on negotiable fees in the Philippines is getting the seller to cover DST and transfer tax (saving you 2% to 2.25%) or negotiating 10% to 20% off legal fees by comparing quotes and limiting service scope.

Can I ask the seller to cover some closing costs in the Philippines?

The likelihood that a seller will agree to cover some closing costs in the Philippines is moderate to good, especially in a buyer's market or when the seller is motivated, though it is less common with developer sales where pricing is more fixed.

Specific closing costs that sellers in the Philippines are most commonly willing to cover include the capital gains tax (which is legally the seller's responsibility anyway), broker commission, and sometimes a credit toward DST or transfer tax as a price negotiation tool.

Sellers in the Philippines are more likely to accept covering closing costs when inventory is high in that micro-market, the property has been listed for a long time, there are condition issues, or the seller needs to close quickly for personal or financial reasons.

Is price bargaining common in the Philippines in 2026?

As of early 2026, price bargaining is common and expected in the Philippines resale property market, with buyers routinely making offers below the asking price and sellers building negotiation room into their listings.

Buyers in the Philippines typically negotiate 3% to 8% below the asking price in standard situations (₱300,000 to ₱800,000 or $5,300 to $14,000 or €4,900 to €13,000 off a ₱10 million listing), with discounts of 10% or more possible when the seller is motivated, the property has issues, or local inventory is high, particularly in active resale markets like Makati (Salcedo Village, Legazpi Village), BGC in Taguig, Ortigas fringe areas in Pasig, and Lahug in Cebu City.

Don't sign a document you don't understand in the Philippines

Buying a property over there? We have reviewed all the documents you need to know. Stay out of trouble - grab our comprehensive guide.

What monthly, quarterly or annual costs will I pay as an owner in the Philippines?

What's the realistic monthly owner budget in the Philippines right now?

The realistic monthly owner budget for a residential property in the Philippines in 2026 is around ₱8,000 to ₱25,000 ($140 to $440 or €130 to €405) for a typical Metro Manila condo, covering association dues and utilities, though this varies significantly by property type and location.

The main recurring expense categories that make up this monthly budget in the Philippines are condominium association dues (the largest predictable cost for condo owners), utilities like electricity and water (heavily dependent on aircon usage), internet, and occasional special assessments or sinking fund contributions.

The realistic low-to-high range for monthly owner costs in the Philippines is around ₱5,000 to ₱12,000 ($88 to $210 or €81 to €195) at the low end for a small provincial condo or minimal-use property, up to ₱30,000 to ₱50,000 ($530 to $880 or €485 to €810) or more for a large Metro Manila condo or house with subdivision HOA fees and higher utility consumption.

The monthly cost that tends to vary the most in the Philippines is electricity, because aircon usage in the tropical climate can swing your power bill dramatically between a vacant unit and one in daily use.

You can see how this budget affect your gross and rental yields in the Philippines here.

What is the annual property tax amount in the Philippines in 2026?

As of early 2026, the annual property tax (Real Property Tax plus Special Education Fund levy) in the Philippines is approximately 2% of the assessed value in provinces or 3% of the assessed value in Metro Manila, which might translate to around ₱20,000 to ₱60,000 ($350 to $1,050 or €325 to €970) per year for a property with an assessed value of ₱1 to ₱2 million.

The realistic low-to-high range for annual property taxes in the Philippines depends heavily on your property's assessed value, with a provincial property assessed at ₱500,000 paying around ₱10,000 ($175 or €160) per year, while a Metro Manila property assessed at ₱5 million might pay around ₱150,000 ($2,630 or €2,430) per year.

Property tax in the Philippines is calculated based on the assessed value (not the market price), which is a percentage of the fair market value set by the local government, and then the basic RPT rate (up to 1% in provinces or 2% in Metro Manila) plus the 1% SEF levy is applied to that assessed value.

Exemptions or reductions on property tax in the Philippines are limited and typically apply to government-owned properties, charitable institutions, or properties used for religious or educational purposes, with no general exemptions for individual residential owners.

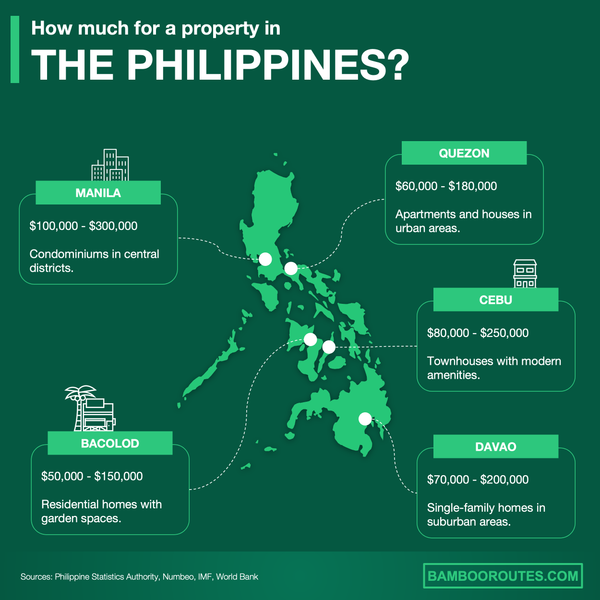

We created this infographic to give you a simple idea of how much it costs to buy property in different parts of the Philippines. As you can see, it breaks down price ranges and property types for popular cities in the country. We hope this makes it easier to explore your options and understand the market.

If I rent it out, what extra taxes and fees apply in the Philippines in 2026?

What tax rate applies to rental income in the Philippines in 2026?

As of early 2026, foreign property owners who are non-resident aliens not engaged in trade or business in the Philippines typically face a flat 25% final tax on gross rental income, while residents and those engaged in business may be subject to regular income tax rates with more complex filing requirements.

Whether landlords can deduct expenses from rental income taxes in the Philippines depends on their tax status: those under the 25% final withholding tax on gross income generally cannot deduct expenses, while those under regular income tax filing may deduct allowable expenses like repairs, depreciation, and property management fees.

The realistic effective tax rate range after deductions for typical landlords in the Philippines is 25% on gross for non-resident aliens (no deductions), or potentially 15% to 30% effective rate for resident landlords under graduated income tax after deducting allowable expenses, depending on total income levels.

Yes, foreign property owners in the Philippines often pay a different rental income tax rate than residents, with non-resident aliens commonly subject to the flat 25% final tax on gross rather than the graduated income tax rates available to residents.

Do I pay tax on short-term rentals in the Philippines in 2026?

As of early 2026, short-term rental income in the Philippines (such as Airbnb) is subject to income tax and may also trigger percentage tax or VAT obligations if your gross receipts exceed certain thresholds, plus you may need local permits (Barangay or city business registration) to operate legally.

Short-term rental income is not taxed differently than long-term rental income in terms of the base income tax rate, but the operational requirements differ because short-term rentals often require business registration, may be subject to percentage tax (3% on gross) or VAT (12% if above thresholds), and many condos have house rules restricting short-term stays that can result in penalties if violated.

If you want to optimize your rental strategy, you can read our complete guide on how to buy and rent out in the Philippines.

Get to know the market before buying a property in the Philippines

Better information leads to better decisions. Get all the data you need before investing a large amount of money. Download our guide.

If I sell later, what taxes and fees will I pay in the Philippines in 2026?

What's the total cost of selling as a % of price in the Philippines in 2026?

As of early 2026, the total cost of selling a residential property in the Philippines is typically around 8% to 12% of the sale price, covering capital gains tax, broker commission, and small documentation or administrative costs.

The realistic low-to-high percentage range for total selling costs in the Philippines is about 6% at the minimum (if you sell without a broker and have minimal paperwork) to 14% or more at the high end (if broker fees are at the upper range and you have complex documentation needs).

The specific cost categories that make up the total selling cost in the Philippines typically include capital gains tax (often 6% for capital assets), broker commission (2.5% to 5%), small legal or notary costs for document preparation, and potentially early mortgage repayment fees if the property is still financed.

The single largest contributor to selling expenses in the Philippines is usually the capital gains tax at 6%, followed closely by the broker commission which can range from 2.5% to 5% of the sale price.

What capital gains tax applies when selling in the Philippines in 2026?

As of early 2026, the capital gains tax on the sale of real property classified as a capital asset in the Philippines is typically 6% of the gross selling price or the current fair market value, whichever is higher.

Exemptions to capital gains tax in the Philippines are limited, but a notable one applies to the sale of a principal residence if the proceeds are fully used to purchase a new principal residence within 18 months, subject to specific conditions and a once-in-a-lifetime limit.

Foreigners do not pay extra capital gains taxes when selling property in the Philippines simply because they are foreign, as the tax is based on the property's location and classification rather than the seller's nationality.

The capital gain in the Philippines is calculated using the gross selling price or fair market value (whichever is higher) as the tax base, not the difference between sale price and purchase price, which means the 6% applies to the full value rather than just your profit.

We made this infographic to show you how property prices in the Philippines compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it's in our blog articles or the market analyses included in our property pack about the Philippines, we always rely on the strongest methodology we can … and we don't throw out numbers at random.

We also aim to be fully transparent, so below we've listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why it's authoritative | How we used it |

|---|---|---|

| Bureau of Internal Revenue (BIR) | The Philippine government's official tax authority. | We used it to anchor Documentary Stamp Tax rates and confirm DST is a core national tax. We then translated that into buyer-focused closing cost checklists. |

| BIR Revenue Memorandum Circular 99-2023 | An official BIR issuance clarifying real estate tax treatment. | We used it to explain withholding mechanics and the ordinary vs capital asset distinction. We flagged how this affects which taxes appear at closing. |

| BIR Revenue Regulations 1-2024 | The official regulation setting VAT-exempt thresholds. | We used it to confirm the ₱3.6 million VAT threshold for residential dwellings. We converted that into a simple decision tree for buyers. |

| DILG Local Government Code | The official law empowering LGUs to levy transfer and property taxes. | We used it to ground transfer tax and annual RPT as LGU-based costs. We translated the legal framework into practical steps. |

| Land Registration Authority (LRA) | The national agency overseeing land title registration fees. | We used it to anchor that registration fees are part of the title-transfer pipeline. We paired it with market data for realistic budget ranges. |

| PwC Worldwide Tax Summaries | A major global tax firm with regularly reviewed public guidance. | We used it to cross-check withholding treatment for non-residents. We verified our rental income tax section with this source. |

| Grant Thornton Philippines | A Big 4 firm explaining how BIR regulations apply in practice. | We used it to confirm the exact VAT threshold and effective date mechanics. We presented the rule in plain English for non-professionals. |

| Bureau of Local Government Finance (BLGF) | The national bureau interfacing with LGU tax administration. | We used it to verify LGUs actively collect RPT and SEF in practice. We warned buyers to confirm local billing cycles. |

| Lamudi Philippines | A long-running property marketplace with consistent market guidance. | We used it to triangulate typical broker commission ranges. We adapted it into guidance on who pays in Philippine transactions. |

| Malaya Business Insight | A national business publication with market reporting. | We used it for practical condo association dues ranges in Metro Manila. We built a realistic monthly owner budget template from it. |

| DMCI Homes | A major listed developer with direct guidance on condo operations. | We used it to explain how dues are computed per sqm. We warned buyers about turnover and assessment timing surprises. |

| BIR Form 1706 Guidelines | A BIR primary document for capital gains tax returns. | We used it to confirm CGT filing requirements in property sales. We explained why sellers need clean documentation before buyers can register. |

Get fresh and reliable information about the market in the Philippines

Don't base significant investment decisions on outdated data. Get updated and accurate information with our guide.