Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

Pre-selling condos in the Philippines offer potential savings of 10-20% compared to ready-for-occupancy units but come with significant risks including project delays, developer bankruptcy, and hidden costs.

While strict laws like Presidential Decree 957 and the Maceda Law provide buyer protections, delays averaging several months to over a year are common in Metro Manila, and around 10-20% of projects experience notable setbacks or construction halts.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

Pre-selling condos in the Philippines are protected by comprehensive laws but carry substantial risks including delays, quality issues, and potential developer bankruptcy.

Buyers typically pay 10-30% upfront and may wait several months to over a year beyond promised delivery dates, especially outside prime locations like Makati and BGC.

| Risk Factor | Level of Risk | Mitigation Strategy |

|---|---|---|

| Project Delays | High (10-20% of projects) | Choose established developers, verify DHSUD registration |

| Developer Bankruptcy | Medium (5-10% of projects) | Research developer financial history, check track record |

| Quality Issues | High (common complaint) | Include detailed specifications in contract, inspect thoroughly |

| Hidden Costs | Very High (almost universal) | Budget extra 15-25% for association dues, taxes, turnover fees |

| Title Transfer Delays | Medium | Verify developer compliance, understand title issuance timeline |

| Location-Based Risks | Variable | Focus on established areas like Makati, BGC for lower risk |

| Loan Approval Issues | Medium | Ensure unit has individual CCT before expecting bank financing |

What legal protections exist for pre-selling condo buyers in the Philippines?

The Philippines has comprehensive legal frameworks protecting pre-selling condo buyers through three major laws.

Presidential Decree 957 (PD 957), known as the Subdivision and Condominium Buyers' Protective Decree, requires all developers to obtain a License to Sell from the Department of Human Settlements and Urban Development (DHSUD). This law mandates full disclosure of project timelines and financial status, protects buyers from fraudulent practices, and provides clear mechanisms for filing complaints when developers fail to meet obligations.

The Maceda Law (Republic Act 6552) grants significant protections to installment buyers by providing statutory grace periods before contract cancellation. If you've paid installments for at least two years, you're entitled to partial refunds ranging from 50% to 90% of total payments made, depending on the length of your payment history. This law prevents developers from arbitrarily cancelling contracts and seizing all payments.

The Condominium Act (Republic Act 4726) establishes the legal framework for condominium corporations, project registration requirements, and individual unit owner rights. These laws work together to create multiple layers of buyer protection, though enforcement can vary depending on the specific circumstances and the buyer's diligence in following proper procedures.

It's something we develop in our Philippines property pack.

How can you assess a developer's financial stability and track record?

Developer financial stability is crucial since around 5-10% of projects face serious financial difficulties or bankruptcy before completion.

DHSUD requires developers to submit financial documents and maintain a License to Sell, but detailed financial audits aren't always publicly available. You can verify a developer's track record by checking their DHSUD registration status, reviewing their history of on-time project completions, and researching any legal disputes or complaints filed against them through DHSUD records and industry reports.

Established developers like Ayala Land, SM Development Corporation, and Robinsons Land have stronger track records with better completion rates and fewer delays. These major developers typically deliver projects closer to promised timelines and have better financial backing to weather market downturns. Smaller or newer developers may offer lower prices but carry significantly higher risks of delays, quality issues, or project cancellation.

You should also examine the developer's current portfolio - if they have multiple ongoing projects simultaneously, this could strain their resources and increase the risk of delays. Ask for references from previous buyers and visit completed projects to assess build quality and actual delivery timelines versus original promises.

What are typical delay periods for condo delivery in Metro Manila?

Project delays are extremely common in the Philippines, with average delays ranging from several months to over a year beyond promised completion dates.

In Metro Manila and surrounding cities, established developers typically experience delays of 3-12 months, while smaller developers often face delays exceeding one year. Weather conditions, permit processing delays, material supply issues, and labor shortages contribute to these extended timelines. The rainy season from June to November frequently causes additional construction delays.

Leading developers in prime locations like Makati and Bonifacio Global City tend to have better completion records, often delivering within 6-12 months of promised dates. However, projects in outer Metro Manila areas or those handled by less established developers commonly experience delays of 12-24 months or more.

As of September 2025, it's estimated that 10-20% of pre-selling projects experience notable delays, while outright cancellations or permanent construction halts affect approximately 5-10% of projects. These statistics vary significantly based on market conditions, developer reputation, and project location.

What upfront payments are required and what happens if projects are cancelled?

Pre-selling condos typically require substantial upfront payments that put buyer funds at risk.

Reservation fees usually start at ₱25,000 and are generally non-refundable once you sign the reservation agreement. The downpayment typically ranges from 10-30% of the total contract price, which can be paid in installments over several months or years before construction completion. For a ₱5 million condo, you might pay ₱50,000-150,000 as a reservation fee and ₱500,000-1,500,000 as downpayment installments.

If the developer fails to deliver the project, the Maceda Law and PD 957 provide refund protections. Buyers who have made payments for at least two years are entitled to refunds of 50-90% of total payments made, depending on how long they've been paying installments. However, recovering these funds requires filing complaints with DHSUD and going through their adjudication process, which can take months or years to resolve.

The recovery process involves presenting payment receipts, contracts, and evidence of developer non-compliance to the Human Settlements Adjudication Commission (HSAC). While legal protections exist, buyers should be prepared for lengthy legal procedures and potential partial losses if developers become insolvent.

Don't lose money on your property in the Philippines

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

Which government agencies oversee pre-selling projects and how to verify registration?

The Department of Human Settlements and Urban Development (DHSUD) is the primary regulatory body overseeing pre-selling projects in the Philippines.

DHSUD replaced the Housing and Land Use Regulatory Board (HLURB) as the main regulatory authority and issues the mandatory License to Sell that all developers must obtain before marketing pre-selling units. The Human Settlements Adjudication Commission (HSAC) under DHSUD handles disputes and complaints between buyers and developers.

You can verify project registration and developer licenses through the DHSUD official website or by visiting their regional offices. The verification process should confirm that the developer holds a valid License to Sell, the project is properly registered, and all required permits are in place. You should also check if there are any pending complaints or violations against the developer.

Other relevant agencies include the local government units (LGUs) that issue building permits and occupancy certificates. The Securities and Exchange Commission (SEC) regulates the corporate aspects of development companies, while the Bureau of Internal Revenue (BIR) handles tax compliance issues.

It's something we develop in our Philippines property pack.

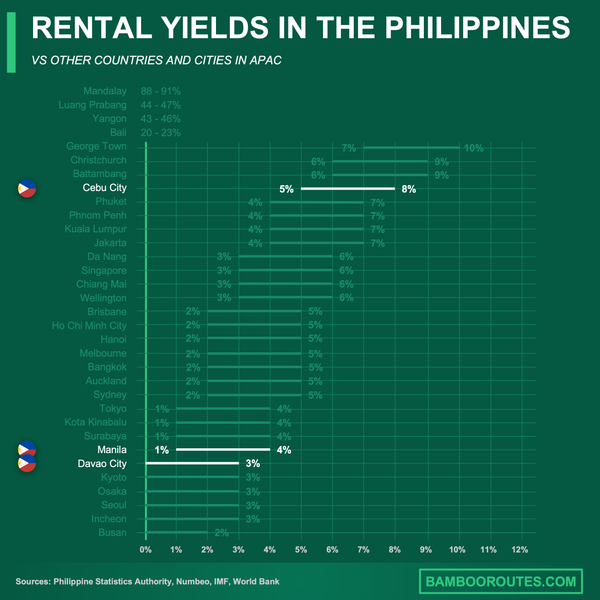

How do resale values and rental yields compare between pre-selling and ready units?

Pre-selling condos are typically priced 10-20% lower than ready-for-occupancy (RFO) units in the same area, offering potential capital appreciation upon completion.

However, the actual realized value depends heavily on market conditions during the 2-4 year construction period, final build quality, and whether promised amenities are delivered as specified. In strong markets like Makati and BGC, pre-selling buyers often see 15-25% appreciation by turnover, while weaker locations may show minimal gains or even losses if market conditions deteriorate.

Rental yields for completed pre-selling condos generally range from 4-7% annually in Metro Manila, which aligns with or falls slightly below yields for comparable RFO units. The key difference is that pre-selling buyers face additional risks of cost escalation through construction price adjustments, association due increases, and unexpected fees that can erode projected returns.

Pre-selling units also cannot generate rental income during the construction period, while RFO units can immediately provide cash flow. This opportunity cost, combined with potential delays, means the effective return on pre-selling investments may be lower than initial projections suggest, especially when factoring in inflation and alternative investment returns over the extended timeline.

What hidden costs should buyers expect in pre-selling projects?

Pre-selling condo buyers face numerous hidden costs that can add 15-25% to the total investment beyond the contract price.

| Cost Category | Typical Amount | When Due |

|---|---|---|

| Association Dues | ₱70-100 per sqm monthly | Upon turnover, ongoing |

| Value Added Tax (VAT) | 12% of contract price | During payment schedule |

| Turnover/Move-in Fees | ₱10,000-50,000 | Upon unit delivery |

| Utilities Connection | ₱15,000-30,000 | After turnover |

| Documentary Stamp Tax | ₱15 per ₱1,000 of contract | Upon contract signing |

| Fire/Property Insurance | 0.1-0.3% of unit value annually | Upon turnover, annually |

| Title Transfer Fees | ₱20,000-80,000 | Upon title issuance |

How does location affect pre-selling investment risks?

Location significantly impacts pre-selling risks, with established central business districts offering the lowest risk profiles.

Makati and Bonifacio Global City (BGC) represent the safest pre-selling markets due to strong developer presence, established infrastructure, consistent demand, and better regulatory oversight. Projects in these areas typically experience shorter delays and have higher completion rates, though they also command premium prices that may limit upside potential.

Quezon City, Manila, and Parañaque show moderate risk levels with mixed developer quality and varying infrastructure development. These areas offer better price points but require more careful developer selection and due diligence on specific project locations and surrounding development plans.

Provincial cities like Cebu, Davao, and Iloilo carry higher risks due to greater developer variability, potentially weaker consumer recourse mechanisms, and less predictable market conditions. While these markets may offer higher potential returns, they also face greater risks of project delays, quality issues, and difficulties in dispute resolution.

Areas undergoing rapid development or those dependent on future infrastructure projects carry additional risks if promised improvements are delayed or cancelled, potentially affecting both completion timelines and long-term property values.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

What happens if the developer goes bankrupt before turnover?

Developer bankruptcy represents one of the most serious risks in pre-selling investments, affecting approximately 5-10% of projects during market downturns.

Under PD 957 and the Maceda Law, buyers have legal rights to recover portions of their payments if developers fail to deliver, but bankruptcy proceedings can significantly complicate and delay recovery efforts. When developers become insolvent, secured creditors and construction lenders typically have priority claims on project assets, potentially leaving pre-selling buyers as unsecured creditors with limited recovery prospects.

DHSUD maintains project escrow accounts and developer bonds that provide some financial buffer, but these protections are often insufficient to fully compensate all buyers in large projects. The recovery process involves filing claims through both DHSUD adjudication and court bankruptcy proceedings, which can take several years to resolve.

Some buyers may recover 30-70% of payments made, while others may lose most of their investment. The outcome depends on the developer's asset base, the number of creditors, and the stage of project completion when bankruptcy occurs. Projects closer to completion have better asset recovery potential than those in early construction phases.

How do banks treat pre-selling condos for home loan approval?

Philippine banks have strict requirements for financing pre-selling condos that significantly limit buyer flexibility.

Banks typically refuse to approve home loans for pre-selling units until physical completion and issuance of individual Condominium Certificate of Title (CCT). This means buyers must complete all payments during construction using personal funds, savings, or alternative financing, then apply for bank loans only upon unit turnover for refinancing purposes.

Pre-selling units cannot serve as loan collateral until they have individual titles and physical existence. Some banks offer construction-to-permanent financing programs, but these require substantial documentation, higher down payments (typically 30-40%), and often carry higher interest rates than standard housing loans.

The lack of immediate bank financing means buyers need substantial liquid capital to complete payments during the 2-4 year construction period. This payment structure increases buyer risk exposure and limits the pool of qualified buyers who can manage large upfront investments without bank support during construction.

It's something we develop in our Philippines property pack.

What are the most common buyer complaints after turnover?

Post-turnover complaints are extremely common, affecting the majority of pre-selling condo buyers in various forms.

Quality and workmanship issues top the complaint list, including substandard finishes, defective fixtures, water seepage, electrical problems, and poor construction materials that don't match promised specifications. Unit size discrepancies, known as "shrinkage," frequently occur where delivered units measure 5-15% smaller than floor plans due to thicker walls or revised layouts during construction.

Unfinished or substandard amenities represent another major complaint category, with promised facilities like swimming pools, gyms, landscaping, or parking areas delivered incomplete or significantly different from marketing materials. Delays in title issuance can extend months or years beyond turnover, preventing buyers from securing financing or selling units.

Association turnover delays cause ongoing problems when developers retain control of building management beyond reasonable periods, leading to poor maintenance, excessive fees, and lack of transparency in building operations. Hidden move-in costs, documentation discrepancies, and difficulty enforcing warranty claims round out the most frequent post-turnover disputes that buyers face.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

Pre-selling condos in the Philippines offer potential savings but require careful risk assessment and thorough due diligence on developer reputation and project registration.

While legal protections exist through PD 957 and the Maceda Law, buyers should budget for delays, hidden costs, and potential quality issues that commonly affect pre-selling investments.

Sources

- Respicio & Co. Law - Pre-selling Condo Buyer Rights

- Lawyer Philippines - Required Documents for Pre-selling

- Respicio & Co. Law - Turnover Delay Legal Guidance

- Philippines Judiciary - Presidential Decree 957

- Respicio & Co. Law - Contract Cancellation and Refunds

- LawPhil - Condominium Act RA 4726

- Lawyer Philippines - Contract Cancellation Due to Delays

- UProperty PH - Pre-selling Condos Guide

- Torre Lorenzo - Condo Investment Analysis

- Real.ph - Payment Terms and Upfront Costs