Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

The Philippines presents a mixed investment landscape for American property buyers in 2025, with stable economic growth averaging 5.5-6% GDP annually but complex foreign ownership restrictions that limit Americans to condominium units and land leases.

While rental yields in prime areas like Makati reach 4.5-7%, Americans face significant legal constraints including the inability to directly own land, a 40% foreign ownership cap in condo projects, and transaction costs totaling 13-16% for complete buy-sell cycles.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

The Philippines offers moderate investment potential for Americans, with GDP growth of 5.5-6% and rental yields up to 7% in prime areas, but foreign ownership restrictions limit investment to condos only.

Legal risks include property scams, title fraud, and high transaction costs, while market liquidity remains reasonable with 3-6 months average selling time in Metro Manila.

| Investment Factor | Rating (1-10) | Key Details |

|---|---|---|

| Economic Stability | 7/10 | 5.5-6% GDP growth, stable inflation |

| Foreign Ownership Rights | 4/10 | Condos only, 40% cap, no land ownership |

| Rental Yields | 6/10 | 4.5-7% in prime areas like Makati/BGC |

| Legal Security | 5/10 | Title fraud risks, complex due diligence needed |

| Market Liquidity | 6/10 | 3-6 months average selling time |

| Transaction Costs | 3/10 | 13-16% total roundtrip costs |

| Overall Investment Appeal | 5/10 | Moderate potential with significant restrictions |

How stable is the Philippine economy right now, and what's the average GDP growth rate over the past five years?

The Philippine economy maintains solid stability as of September 2025, with GDP growth reaching 5.5% in Q2 2025 and forecasts projecting 5.6-6% growth for 2025 overall and 6.1% in 2026.

Over the past five years, the Philippines has averaged 5.5-6% annual GDP growth, making it one of Asia's faster-growing economies despite the 2020 pandemic disruption. The economy recovered strongly from that temporary setback, driven by robust household consumption, sustained employment growth, and ongoing infrastructure investment.

The country's economic resilience stems from strong domestic demand that shields it from global trade tensions and external shocks. Inflation remains moderate, and the job market continues expanding, creating a stable foundation for property investment.

Key economic indicators show the Philippines consistently outperforming many regional peers, with the Asian Development Bank highlighting it as a "bright spot" in Southeast Asia for 2025-2026. This economic stability provides a reasonable backdrop for property investment, though external risks from global trade disputes remain the primary concern rather than domestic instability.

What are the current property price trends in Manila, Cebu, and Davao, and how do they compare to five years ago?

Metro Manila residential property prices increased 6.5% year-on-year in 2025, with mass-market properties driving growth while luxury condos experienced a slight 0.7% decline.

Cebu property prices have shown consistent annual growth of 3-7%, with a typical 50-square-meter investment condo costing ₱4.12-4.28 million in 2025. The Cebu market demonstrates steady appreciation without speculative bubbles.

Davao remains the most affordable major city, with most homes priced between ₱2.5-6 million and residential lots starting at ₱4 million. Price growth in Davao stays stable and non-speculative, making it attractive for budget-conscious investors.

Compared to five years ago, property prices across all three cities have increased 15-30% since 2020, with secondary cities like Cebu and Davao experiencing faster growth rates than Metro Manila. This represents moderate appreciation rather than bubble-like conditions.

It's something we develop in our Philippines property pack.

What are the laws on foreign ownership of real estate in the Philippines, and what exact restrictions apply to Americans?

Americans cannot directly own land in the Philippines under any circumstances, but can lease land for up to 99 years under new 2025 legislation that extended the previous 50+25 year limit.

| Property Type | Can Americans Buy? | Key Restrictions |

|---|---|---|

| Condominium Unit | Yes | Maximum 40% of total project owned by foreigners |

| Land | No (except lease) | Up to 99-year lease; no title ownership |

| House/Building Only | Yes | Must lease land beneath; own only structure |

| Corporate Entity | Yes (indirect) | Corporation must be at least 60% Filipino-owned |

| Agricultural Land | No | Strictly prohibited for all foreigners |

For condominium ownership, Americans can purchase units directly only in projects where foreign ownership remains below 40% of total units. Once a project reaches the 40% foreign ownership cap, no additional units can be sold to foreigners.

Americans can own houses or buildings constructed on leased land, but the land lease arrangement requires careful legal structuring. Alternatively, Americans can gain indirect land ownership through a Philippine corporation with maximum 40% foreign equity, though this requires Filipino business partners.

What kinds of properties can foreigners legally buy, and are there clear differences between condos, land, and houses?

Foreigners can legally purchase condominium units with full ownership rights, provided the entire condominium project maintains less than 40% foreign ownership.

Land ownership remains completely prohibited for foreigners, with leasing being the only legal option. Americans can secure 99-year renewable land leases, which provide long-term control without actual ownership rights.

Houses present a hybrid scenario where Americans can own the physical structure but must lease the underlying land. This arrangement requires separate contracts for the building and land lease, creating more complex legal documentation.

The key practical differences are that condos offer the simplest ownership structure with full property rights, land requires lease arrangements that don't provide ownership security, and houses involve split ownership that complicates financing and resale. Condos also typically provide better liquidity and easier financing options for foreign buyers.

Corporate ownership through a Filipino-majority company remains technically possible but requires trusted local partners and ongoing compliance with foreign investment regulations.

How high are property taxes, capital gains taxes, and rental income taxes for foreigners, and what's the total effective rate?

Property taxes in the Philippines are relatively modest at 1-2% annually based on assessed value (not market value), which typically runs 10-20% below actual market prices.

Capital gains tax hits 6% of gross selling price or fair market value, whichever is higher, and is legally payable by the seller but often factored into negotiated sale prices. This creates an effective 6% cost for sellers to recover.

Rental income faces up to 25% tax for foreigners not engaged in trade or business in the Philippines, or 20% if the foreigner is engaged in local business activities. These rates apply to gross rental income after standard deductions.

Transaction costs for buying property total 8-10% of purchase price, including stamp tax (1.5%), transfer fees (0.5-0.75%), registration costs (1%), notary fees, and real estate agent commissions (3-5%). Selling costs add another 5-6%.

The complete roundtrip transaction cost (buying plus selling) typically reaches 13-16% of property value, making short-term investment strategies financially challenging due to high entry and exit costs.

How easy is it for an American to open a local bank account and secure financing or a mortgage for property purchases?

Americans can open Philippine bank accounts with proper documentation including passport, immigration documents, and proof of address, though some banks require an ACR (Alien Certificate of Registration) for long-term residents.

Mortgage financing for Americans is available from select Philippine banks and developers, typically requiring 20-30% down payment with interest rates currently ranging 5-8.5%. Approval becomes easier with documented local income or a Filipino co-borrower.

Most Philippine banks prefer applicants with established local income sources or business operations. Americans working remotely for US companies may face additional scrutiny regarding income verification and currency exchange risks.

Developer financing often provides more flexible terms than traditional banks, particularly for condominium purchases in new projects. Some developers offer in-house financing with lower down payment requirements but higher overall interest rates.

The financing process typically takes 30-60 days for approval, and Americans should expect more extensive documentation requirements compared to domestic borrowers, including proof of overseas income sources and currency stability assurances.

Don't lose money on your property in the Philippines

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

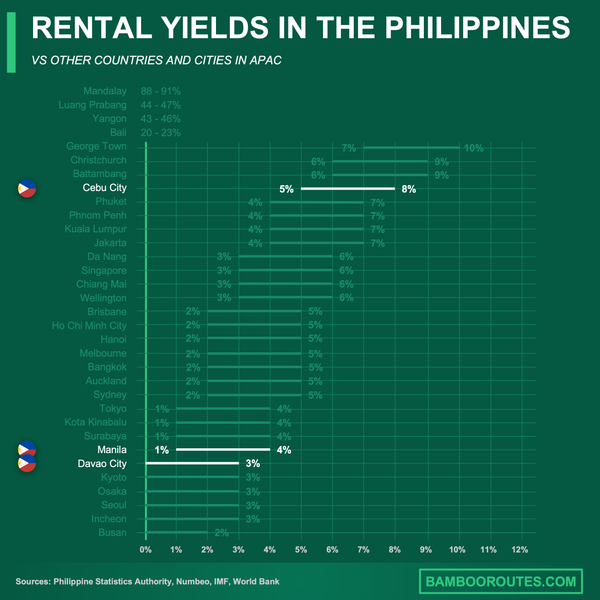

What's the average rental yield in prime areas like Makati or Bonifacio Global City, and how does it compare to U.S. cities?

Prime areas like Makati and Bonifacio Global City (BGC) currently deliver gross rental yields averaging 4.5-7%, with newer, smaller, and more centrally located condominiums achieving the higher end of this range.

These yields compare favorably to major U.S. cities where prime area rental yields often fall below 4%. Cities like Manhattan, San Francisco, and central Los Angeles typically generate 2-4% gross yields, making Philippines prime locations competitive from a yield perspective.

The rental market in BGC particularly benefits from the concentration of multinational corporations, IT companies, and expatriate workers willing to pay premium rents for modern amenities and convenient locations. Makati maintains strong demand from business executives and professionals working in the central business district.

However, these gross yields don't account for vacancy periods, property management fees, maintenance costs, and taxes that can reduce net returns to 3-5% in practice. Property management and maintenance costs tend to be higher in prime locations due to premium building amenities and services.

What are the risks of overbuilding or housing bubbles in the Philippines' major urban centers?

Metro Manila faces localized condominium oversupply, particularly in the Bay Area, with approximately 81,400 vacant condo units and elevated vacancy rates in neighboring zones as of 2025.

The oversupply primarily affects the luxury and mid-market condominium segments rather than the broader housing market. Despite condo oversupply, the Philippines maintains a massive affordable housing deficit of 6.5 million units, indicating the oversupply is concentrated in higher price tiers.

Cebu and Davao show healthier supply-demand balance with new projects typically absorbing quickly without creating significant inventory buildup. These secondary cities demonstrate more sustainable development patterns compared to Metro Manila.

Broad property bubble indicators remain absent, but price corrections are possible in saturated luxury segments of Metro Manila. The disconnect between high-end oversupply and affordable housing shortages suggests market distortions rather than systematic bubble conditions.

Investors should exercise particular caution in new Bay Area developments and luxury projects in Metro Manila, while secondary cities present lower oversupply risks for property investment.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

How safe is it legally to hold property in the Philippines—are there common scams, land title disputes, or fraud risks to watch for?

Property fraud risks in the Philippines include fake or "dead" titles (TCT/OCT), unlicensed subdivision sales, "tax declaration" sales instead of properly titled land, and premature agricultural land conversion schemes.

Americans should demand the seller's Original Certificate of Title (OCT/TCT), verify authenticity at the Registry of Deeds, and confirm developer License to Sell (LTS) status before any purchase. Title verification requires physical inspection of original documents, not photocopies.

The Torrens title system provides strong legal protection when registration is legitimate, but fraud through paper title manipulation and insider collusion remains possible. Double sales of the same property to multiple buyers represent a recurring fraud pattern.

Common warning signs include sellers reluctant to show original titles, properties priced significantly below market rates, developments lacking proper permits, and transactions pushed to complete quickly without adequate due diligence time.

Legal counsel specializing in Philippine real estate law is essential for all property transactions. Professional title searches, surveyor verification, and comprehensive due diligence provide the best protection against fraud, though they cannot eliminate all risks entirely.

It's something we develop in our Philippines property pack.

What is the political stability outlook, and how might changes in government affect property rights for foreigners?

The Philippines maintains political stability in 2025 with property rights for foreigners remaining unchanged under current law and no indication of major policy shifts affecting existing ownership structures.

Government changes in the Philippines typically involve extensive political debate and regulatory input before implementing major foreign investment policy modifications. Retroactive elimination of legitimate property rights remains extremely unlikely given constitutional protections and economic considerations.

Recent policy changes have actually favored foreign investment, such as the 2025 extension of land lease terms from 50+25 years to 99 years, indicating government intent to attract rather than restrict foreign property investment.

Political risks center more on bureaucratic inefficiency and regulatory complexity rather than fundamental changes to foreign ownership rights. The Philippines continues attracting foreign investment as a key economic strategy.

Any future liberalization of foreign ownership rules would likely benefit existing foreign property owners rather than create disadvantages. Current ownership rights established under existing law maintain strong legal protection regardless of political transitions.

How liquid is the property market—how long does it usually take to resell a condo in Metro Manila or Cebu?

Condominiums in Metro Manila and Cebu typically take 3-6 months to resell, depending on pricing, unit size, location, and market conditions as of 2025.

Well-priced properties in prime locations like Makati, BGC, or central Cebu can sell within 2-4 months, while overpriced or poorly located units may require 6-12 months or longer to find buyers.

The Metro Manila market has become more selective due to high supply levels, with buyers having numerous options and taking time to compare properties. Cebu maintains slightly faster absorption rates due to better supply-demand balance.

New condominium projects in Cebu and Davao often absorb quickly, but resale units face more competition from new developments offering modern amenities and flexible payment terms. Older buildings require competitive pricing to attract buyers.

Market liquidity varies significantly by price segment, with mass-market properties (₱3-8 million) showing better liquidity than luxury units above ₱15 million, which may require 6+ months to sell even in prime areas.

What are the main costs beyond the purchase price—closing fees, association dues, maintenance costs, and insurance premiums?

Closing fees typically total 8-10% of property purchase price, including transfer tax (0.5-0.75%), documentary stamp tax (1.5%), registration fees (1%), notary costs, and real estate agent commissions (3-5%).

1. **Transfer and Registration Costs**: Transfer tax, documentary stamps, and registration fees combine for approximately 3-4% of purchase price2. **Professional Fees**: Legal fees, surveyor costs, and notary services add 1-2% to transaction costs 3. **Agent Commissions**: Real estate broker fees typically range 3-5% of sale price4. **Due Diligence Costs**: Title searches, property inspections, and legal reviews cost ₱50,000-150,0005. **Financing Fees**: Mortgage origination, processing, and insurance fees add 1-2% if financing is usedHomeowners Association (HOA) dues for typical condominiums range ₱100-180 per square meter monthly, with luxury towers charging significantly higher rates for premium amenities and services.

Property insurance costs remain modest at ₱3,000-6,000 annually for standard coverage, though luxury properties and high-value units require proportionally higher premiums for adequate protection.

Maintenance responsibilities for condo owners cover interior repairs and improvements, while exterior maintenance and common area upkeep are included in HOA dues. New home construction averages ₱10,919 per square meter, with condominiums costing approximately ₱32,000 per square meter.

It's something we develop in our Philippines property pack.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

The Philippines presents a challenging but potentially rewarding property investment environment for Americans, with economic stability and competitive rental yields balanced against significant legal restrictions and fraud risks.

Success requires careful due diligence, legal counsel, and realistic expectations about ownership limitations, transaction costs, and market liquidity constraints that differ substantially from U.S. property markets.

Sources

- Trading Economics - Philippines GDP Growth

- OECD Economic Outlook - Philippines Report

- BambooRoutes - Philippines 5-Year Real Estate Forecast

- Asian Development Bank - Philippines Economic Outlook

- Cushman & Wakefield - Philippines Real Estate Q2 2025

- BambooRoutes - Average House Price Philippines

- Bloomberg - Philippines 99-Year Land Lease

- Global Property Guide - Philippines Taxes and Costs

- BambooRoutes - Americans Buying Houses Philippines

- Housing Interactive - BGC Market Analysis Q1 2025