Authored by the expert who managed and guided the team behind the Philippines Property Pack

Get all the data you need about the real estate market in The Philippines

We constantly update this blog post so buyers can follow the Philippine property market with fresh public data, not old opinions.

As of June 2026, the residential property market in The Philippines is soft in some condo districts, but still supported by population growth, remittances and real housing need.

The main point is simple: buying property in The Philippines in 2026 can make sense, but only if the price, building, location and rental demand are checked carefully.

And if you’re planning to buy a property in this place, you may want to download our pack covering the real estate market in The Philippines.

So, is now a good time?

Rather yes, June 2026 is a decent time to buy residential property in The Philippines, but mainly for selective buyers who can negotiate and avoid weak condo buildings.

The strongest signal is that BSP’s latest RPPI shows Philippine residential price growth slowing to only 1.6% in Q4 2025, which means the broad market is no longer hot.

Another strong signal is Colliers’ Q1 2026 warning that Metro Manila condo vacancy could reach 25.6% by end 2026, with Bay Area close to 60%, which gives buyers bargaining power.

Other strong signals are high inflation, a 4.5% BSP policy rate, flat condo rents, weaker new permit activity and continuing demand for affordable end-user housing.

The best strategy in The Philippines in 2026 is to negotiate hard on resale or ready-for-occupancy condos, target liquid areas near jobs and transport, and hold for the long term rather than flip quickly.

This is not financial or investment advice, because we do not know your personal situation, financing, tax position or risk tolerance, so you should do your own research.

Is it smart to buy now in The Philippines, or should I wait as of 2026?

Do real estate prices look too high in The Philippines as of 2026?

As of 2026, Philippine residential property prices look about 5% to 10% above fair value nationally, but some prime Metro Manila condos look 10% to 20% too expensive when compared with rents, incomes and vacancy risk.

The clearest on-the-ground signal is that many ready-for-occupancy condos in Metro Manila now need discounts, flexible payment terms or rent-to-own offers, especially in investor-heavy areas such as Bay Area, parts of Makati CBD, BGC, Ortigas and Quezon City.

Another signal is that affordable and economic projects are moving better than luxury condos, which suggests that real household demand is still there but buyers are pushing back against prices that feel too high.

You can also read our latest update regarding the housing prices in the Philippines.

Does a property price drop look likely in The Philippines as of 2026?

As of 2026, the risk of a meaningful nationwide residential price decline in The Philippines looks medium-low, while the risk of a local condo correction in oversupplied Metro Manila districts looks medium to high.

A realistic 12-month range for Philippine home prices is about -3% to +4% nationally, but weak Metro Manila condo pockets could see -5% to -10% if sellers need to clear inventory.

The macro factor that would most increase the chance of a Philippine property price drop is another rise in borrowing costs, because higher mortgage payments quickly reduce what local buyers can afford.

This risk is real in 2026 because BSP lifted its policy rate to 4.5% after inflation jumped, but a major new rate shock is not our base case unless inflation stays high for several more months.

Finally, please note that we cover the price trends for next year in our pack about the property market in The Philippines.

Could property prices jump again in The Philippines as of 2026?

As of 2026, the chance of a broad residential price surge in The Philippines over the next 12 months looks low to medium, because rents are flat in many condo areas and financing is still tight.

The plausible upside range is about +2% to +4% nationally in 2026, with stronger locations near real transport upgrades or job hubs reaching about +5% to +8% if buyer confidence improves.

The biggest demand-side trigger would be cheaper credit, because lower mortgage rates would quickly help local families and OFW-supported buyers qualify for better homes in The Philippines.

Please also note that we regularly publish and update real estate price forecasts for the Philippines here.

Are we in a buyer or a seller market in The Philippines as of 2026?

As of 2026, The Philippines is a mixed residential market, but it is buyer-leaning for many Metro Manila condos and seller-leaning for affordable homes in job-connected growth areas.

The closest local inventory signal is Colliers’ Metro Manila condo inventory life, which improved to about 6.8 years but still remains far above what a tight seller’s market would look like.

The share of formal price cuts is hard to measure nationally, but the need for developer incentives, resale discounts and longer payment plans shows that many condo sellers have less leverage in 2026.

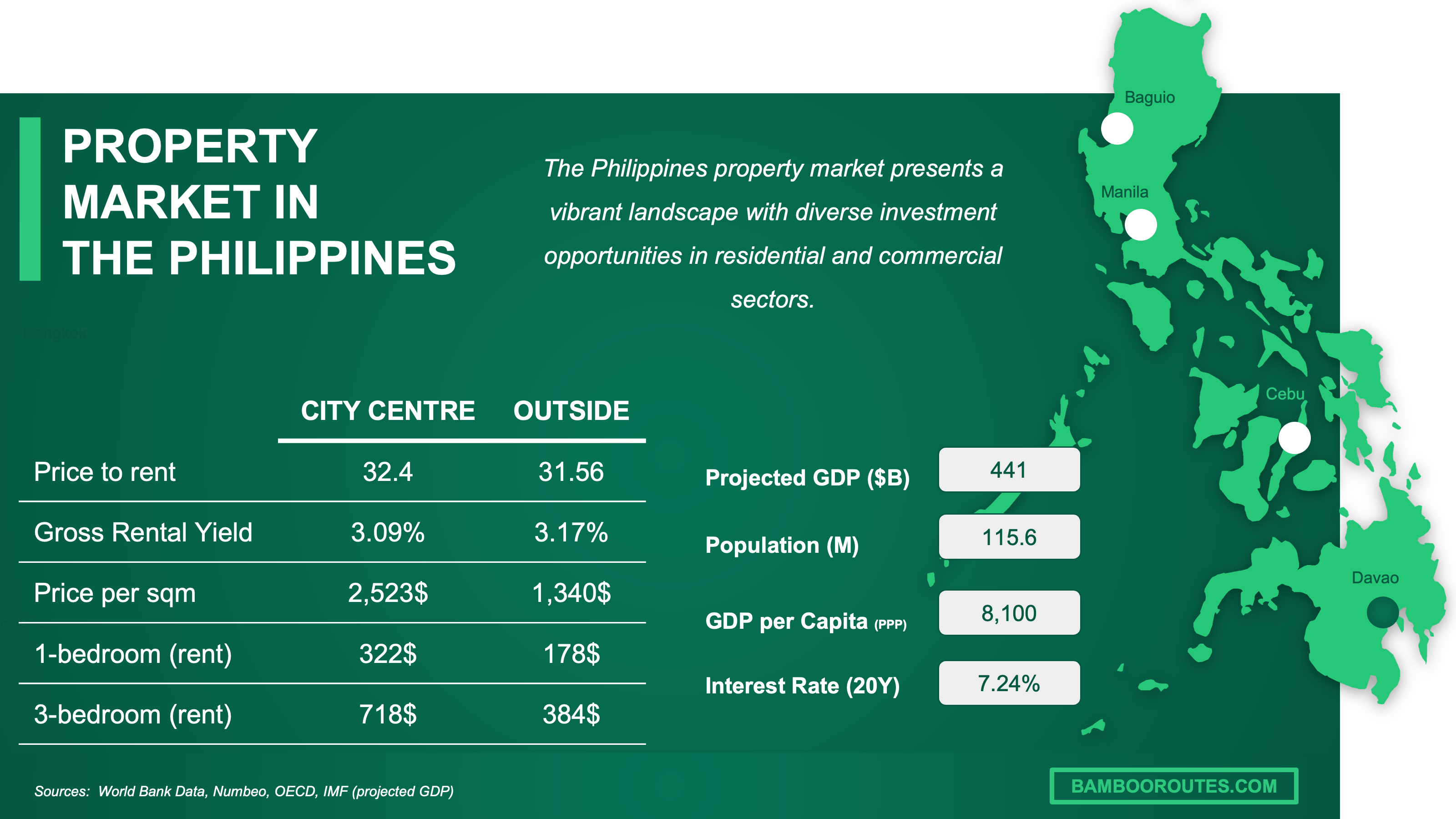

We have made this infographic to give you a quick and clear snapshot of the property market in the Philippines. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Are homes overpriced, or fairly priced in The Philippines as of 2026?

Are homes overpriced versus rents or versus incomes in The Philippines as of 2026?

As of 2026, homes in The Philippines look fairly priced nationally but expensive in many urban condo projects when purchase costs are compared with rents and household incomes.

A simple price-to-rent check suggests that many Metro Manila condos trade at about 18 to 28 years of gross rent, while a more balanced market would usually feel safer around 14 to 18 years.

A simple price-to-income check is also stretched, because a PHP5 million condo is about 10 years of average NCR family income and about 14 years of average national family income before loan costs and taxes.

Finally please note that you will have all the indicators you need in our property pack covering the real estate market in The Philippines.

Are home prices above the long-term average in The Philippines as of 2026?

As of 2026, Philippine home prices are above their long-term nominal average, but not dramatically above trend after inflation is considered.

The latest 12-month price change was only 1.6% in Q4 2025, which is much slower than the post-pandemic rebound and also slower than many buyers expected from a growing economy.

In real terms, Philippine residential prices look roughly flat to 5% above their prior cycle trend, while the clearest above-trend risk remains in prime condos with weak leasing demand.

Get fresh and reliable information about the market in the Philippines

Don't base significant investment decisions on outdated data. Get updated and accurate information.

What local changes could move prices in The Philippines as of 2026?

Are big infrastructure projects coming to The Philippines as of 2026?

As of 2026, the biggest infrastructure driver for residential prices in The Philippines is the combined rail pipeline, especially the Metro Manila Subway and North-South Commuter Railway, which can lift well-located areas by about 2 to 5 percentage points per year once stations become usable.

The timeline is still uneven, because these projects are approved and under construction in stages, but the price impact should be strongest when buyers can see actual stations, shorter commutes and better links to job centers.

For the latest updates on the local projects, you can read our property market analysis about the Philippines here.

Are zoning or building rules changing in The Philippines as of 2026?

The most important rule change for the Philippine residential market is not classic zoning, but RA 12001, the Real Property Valuation and Assessment Reform Act, because it can gradually make assessed values closer to market values.

As of 2026, the likely net effect is a small to moderate increase in holding costs over time, especially in cities where old assessed values are far below real market prices.

The areas most affected are likely higher-value urban LGUs in Metro Manila, Cebu, Davao, Iloilo, Cavite, Laguna, Pampanga and Bulacan, where market values have moved faster than official assessment systems.

Are foreign-buyer or mortgage rules changing in The Philippines as of 2026?

As of 2026, foreign-buyer rules in The Philippines are only slightly more supportive, while mortgage conditions are tighter, so the net price effect is limited and probably less important than affordability.

The main foreign-buyer change is RA 12252, which liberalizes long-term leases of private land for qualifying foreign investors, but ordinary foreign individual buyers still face land ownership restrictions and usually focus on condos.

The main mortgage change is the higher BSP policy rate of 4.5%, which makes borrowing more expensive and keeps speculative demand cautious in 2026.

You can also read our latest update about mortgage and interest rates in The Philippines.

Buying real estate in the Philippines can be risky

An increasing number of foreign investors are showing interest. However, 90% of them will make mistakes. Avoid the pitfalls with our comprehensive guide.

Will it be easy to find tenants in The Philippines as of 2026?

Is the renter pool growing faster than new supply in The Philippines as of 2026?

As of 2026, the renter pool in The Philippines is growing in job-dense cities, but new condo supply is growing faster than renter demand in several Metro Manila submarkets.

The best demand signal is long-term household formation, urban employment and remittance support, because many Filipino families still need practical homes near offices, schools, hospitals and transport.

The clearest supply signal is Colliers’ forecast that almost 13,000 Metro Manila condo units could be completed in 2026, which is almost double the 2025 delivery level.

Are days-on-market for rentals falling in The Philippines as of 2026?

As of 2026, rental days-on-market in The Philippines are stable to slightly falling in the best areas, but rising in oversupplied condo districts where tenants have many similar choices.

A well-priced unit in Makati, BGC, Ortigas, Quezon City near universities, Cebu IT Park, Cebu Business Park, Clark or Davao can often lease in about 30 to 60 days, while a weak Bay Area condo can take about 90 to 180 days.

The reason rental time falls in the best Philippine areas is not only low supply, but also the daily pain of commuting, which makes tenants pay faster for practical locations near work, school and transport.

Are vacancies dropping in the best areas of The Philippines as of 2026?

As of 2026, vacancies are likely firmer in Makati CBD, Rockwell, BGC, Ortigas Center, Cebu IT Park, Cebu Business Park, Clark, Angeles, Iloilo Business Park and Davao’s Lanang and Bajada areas, but the wider Metro Manila condo market is still under pressure.

Best-area vacancy is likely around 8% to 15%, while Metro Manila condos overall could reach about 25.6% and Bay Area could approach 60% by the end of 2026.

A practical landlord signal in The Philippines is whether tenants ask first about internet reliability, commute time and building rules before negotiating rent, because that shows real end-user demand rather than bargain-hunting only.

By the way, we’ve written a blog article detailing what are the current rent levels in the Philippines.

Make a profitable investment in the Philippines

Better information leads to better decisions. Save time and money. Download our data.

Am I buying into a tightening market in The Philippines as of 2026?

Is for-sale inventory shrinking in The Philippines as of 2026?

As of 2026, for-sale inventory is not clearly shrinking across The Philippines, because Metro Manila condo inventory is improving from a weak point but remains high, while affordable end-user housing remains tight.

The closest months-of-supply proxy is Colliers’ 6.8 years of remaining Metro Manila condo inventory life, which is better than the 2025 peak but still far above a balanced level.

Are homes selling faster in The Philippines as of 2026?

As of 2026, homes in The Philippines are selling faster only in selected affordable and economic segments, while many luxury or investor-style condos still need longer selling periods.

The year-over-year change is mixed: Colliers reported a strong rebound in preselling net take-up from a weak base, but the resale market still feels selective because buyers are cautious about rates, rents and vacancy.

Are new listings slowing down in The Philippines as of 2026?

As of 2026, we are not confident in a national new-listings estimate for The Philippines, but formal construction signals show future supply is slowing in weaker segments.

The seasonal pattern is usually stronger around project launches and major selling campaigns, but the current environment is unusually cautious because inflation, financing costs and weak condo rents are making developers more selective.

The most plausible reason new supply is slowing is developer caution, because high vacancy and expensive credit make it harder to launch large investor-condo projects at old prices.

Is new construction failing to keep up in The Philippines as of 2026?

As of 2026, new construction in The Philippines is failing to keep up with affordable housing demand, but it is not failing to keep up in investor-heavy Metro Manila condo districts.

The latest permit signal is soft, because PSA reported approved constructions down 25% year on year in September 2025, with residential building value also lower than a year earlier.

The biggest bottleneck is affordability, because many households need homes but cannot comfortably buy the type of formal private housing that developers prefer to build.

Get to know the market before buying a property in the Philippines

Better information leads to better decisions. Get all the data you need before investing a large amount of money.

Will it be easy to sell later in The Philippines as of 2026?

Is resale liquidity strong enough in The Philippines as of 2026?

As of 2026, resale liquidity in The Philippines is strong enough for well-priced homes in proven areas, but weak for generic condos in buildings with many similar units for sale or rent.

A realistic resale time is about 3 to 6 months for a good unit in a liquid area, while a weak investor condo can take 9 to 18 months or need a 10% to 20% discount.

The property trait that most improves resale liquidity in The Philippines is practical location, especially near major jobs, transport, schools, hospitals and established shopping areas.

Is selling time getting longer in The Philippines as of 2026?

As of 2026, selling time in The Philippines is getting longer for weak condos, but not necessarily for affordable homes in good commuter locations.

The realistic current resale range is about 60 to 180 days for good properties, and about 9 to 18 months for less liquid condos in oversupplied buildings.

The clearest reason selling time can lengthen in The Philippines is affordability pressure, because buyers face higher living costs, higher loan costs and more choice in the condo market.

Is it realistic to exit with profit in The Philippines as of 2026?

As of 2026, the chance of exiting with a profit in The Philippines is medium for disciplined buyers and low for buyers who pay full developer prices in oversupplied condo districts.

The minimum holding period that usually makes profit realistic is about 5 to 7 years, because transaction costs, taxes, broker fees and slow early appreciation can eat short-term gains.

A reasonable round-trip cost drag is about 8% to 12% of the property price, so on a PHP5 million home that is roughly PHP400,000 to PHP600,000, about USD6,600 to USD9,900, or about EUR6,100 to EUR9,200 at mid-2026 exchange rates.

The factor that most increases profit odds is buying below market in a liquid location, because the discount gives you protection if rents stay flat or resale competition stays high.

We made this infographic to show you how property prices in the Philippines compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it’s in our blog articles or the market analyses included in our property pack about The Philippines, we always rely on the strongest methodology we can, and we don’t throw out numbers at random.

We also aim to be fully transparent, so below we’ve listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why we trust it | How we used it |

|---|---|---|

| Bangko Sentral ng Pilipinas RPPI | BSP is the central bank and publishes the official residential property price index. | We used it as the main national price benchmark. We treated it as stronger than listing portals because it is based on bank-reported real estate loans. |

| BSP Q4 2025 RPPI release | This is the official interpretation of the latest RPPI release available before June 2026. | We used it to anchor the 1.6% national price growth figure. We also used its location and property-type breakdowns. |

| Colliers Q1 2026 Residential Philippines | Colliers is a major property consultancy with a long-running Philippine residential database. | We used it for Metro Manila condo supply, vacancy, rents and inventory life. We treated it as private-sector evidence, not official statistics. |

| PSA construction permits | PSA is the official statistics agency and permits are a clean signal of future supply. | We used it to judge whether new housing supply is accelerating or slowing. We focused on residential permits and construction value. |

| PSA population and housing data | PSA runs the official census and population statistics for The Philippines. | We used it to estimate long-term housing demand. We also used it to check demand claims from private property sources. |

| PSA Family Income and Expenditure Survey | FIES is the core official source for household income and affordability. | We used it to compare home prices with family incomes. We separated NCR from the national average because Manila affordability is different. |

| BSP overseas remittances | BSP is the official compiler of remittance data, a key housing-demand driver. | We used it to judge support from OFW buyers and families. We treated remittances as a stabilizer, not a guarantee of price growth. |

| BSP policy rate and inflation data | BSP is the official source for monetary policy and inflation context. | We used it to assess mortgage pressure and buyer confidence. We paid special attention to the 4.5% policy rate in 2026. |

| IMF Philippines country page | IMF provides independent macro forecasts used by governments and investors. | We used it to cross-check growth and inflation expectations. We used macro forecasts to avoid relying only on local property sources. |

| World Bank Philippine Economic Updates | The World Bank is a high-quality external source for growth and investment context. | We used it to verify the broader economic backdrop. We mainly used it for growth, resilience and investment-risk context. |

| Lawphil Condominium Act, RA 4726 | Lawphil publishes primary Philippine legal texts. | We used it to explain why condos matter to foreign buyers. We separated condo demand from land-and-house demand. |

| Lawphil 1987 Constitution | This is the primary source for Philippine land-ownership restrictions. | We used it to confirm that ordinary foreign buyers cannot directly own land. We applied this to houses, lots and townhouses. |

| Lawphil RA 12252 | This is the official text of the 2025 foreign-investor lease reform. | We used it to assess whether foreign-buyer rules changed in 2026. We treated it as more relevant to projects than normal home buying. |

| Lawphil RA 12001 | This is the primary legal source for real property valuation reform. | We used it to judge tax and assessment risks. We treated it as a medium-term cost risk, not an immediate crash trigger. |

| PIA/NEDA infrastructure updates | PIA reports official government announcements and NEDA Board decisions. | We used it to identify large infrastructure catalysts. We focused on projects that can change commuting times and residential demand. |

| PNA/DHSUD housing reform rollout | PNA is the government news agency and reports DHSUD housing policy directly. | We used it to track 4PH and affordable-housing policy. We separated real housing need from investor-condo demand. |

Don't buy the wrong property, in the wrong area of the Philippines

Buying real estate is a significant investment. Don't rely solely on your intuition. Gather the right information to make the best decision.