Authored by the expert who managed and guided the team behind the Burma (Myanmar) Property Pack

Get all the data you need about the real estate market in Myanmar

We constantly update this blog post so buyers can follow the Burma (Myanmar) property market with fresh data, not old assumptions.

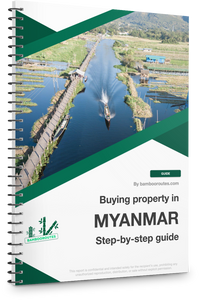

In June 2026, buying property in Burma (Myanmar) is not a simple yes or no decision because prices, rents, inflation, conflict risk, and resale liquidity all point in different directions.

The safest way to read the Burma (Myanmar) real estate market in 2026 is to separate prime Yangon homes from weaker homes in secondary or risky locations.

And if you’re planning to buy a property in this place, you may want to download our pack covering the real estate market in Burma (Myanmar).

So, is now a good time?

As of June 2026, it is rather no for a normal individual buyer to buy property in Burma (Myanmar), unless the buyer is a cash buyer targeting a very good Yangon apartment or condominium.

The strongest signal is that Myanmar’s economy is still fragile, inflation is still high, and household purchasing power remains weak.

Another strong signal is that Yangon property prices are sticky in kyat terms, but that does not mean homes are cheap after political, currency, legal, and liquidity risk.

Other strong signals are conflict risk, electricity problems, earthquake damage, limited mortgage depth, and the lack of a reliable public house price index in Myanmar.

The best strategy is to buy only a legally clean, well managed, generator backed apartment or condominium in prime Yangon, rent it out long term, and avoid speculative short term flipping.

This is not financial or investment advice because we do not know your personal situation, so you should do your own research before buying property in Burma (Myanmar).

Is it smart to buy now in Burma (Myanmar), or should I wait as of 2026?

Do real estate prices look too high in Burma (Myanmar) as of 2026?

As of 2026, Burma (Myanmar) residential property prices look slightly overpriced nationally on a risk adjusted basis, but selected Yangon condominiums can still look fair if bought below asking price and rented well.

The clearest on the ground signal is that current Yangon listings still show many condos and apartments asking tens of millions of kyats, while buyer credit and local incomes remain under pressure.

A second signal is that Myanmar property prices look stronger in nominal kyat terms than in real hard currency terms, which means inflation can make prices look high even when real value is weak.

You can also read our latest update regarding the housing prices in Myanmar.

Does a property price drop look likely in Burma (Myanmar) as of 2026?

As of 2026, the chance of a meaningful property price decline in Burma (Myanmar) is medium in real terms, but low to medium in nominal kyat terms for decent Yangon homes.

Over the next 12 months, we would consider a 0% to 10% nominal fall and a 10% to 20% real fall plausible for good Yangon apartments and condos, while weaker assets could fall more.

The single macro factor that would most increase the odds of a Burma (Myanmar) property price drop is a deeper hit to household income and business cash flow.

This factor is fairly likely in the next months because Myanmar still faces conflict, power shortages, weak demand, high prices, and earthquake related disruption.

Finally, please note that we cover the price trends for next year in our pack about the property market in Burma (Myanmar).

Could property prices jump again in Burma (Myanmar) as of 2026?

As of 2026, the chance of a renewed property price surge in Burma (Myanmar) is medium in nominal kyat terms, but low in real hard currency terms.

For prime Yangon homes, a 10% to 25% nominal rise over the next 12 months is plausible if inflation stays high, construction costs rise, or buyers use property as a store of value.

The biggest demand side trigger would be investor and cash buyer return to prime Yangon property, especially in Bahan, Yankin, Kamaryut, Sanchaung, Hlaing, Ahlone, and Kyauktada.

Please also note that we regularly publish and update real estate price forecasts for Myanmar here.

Are we in a buyer or a seller market in Burma (Myanmar) as of 2026?

As of 2026, Burma (Myanmar) is a selective buyer leaning market overall, but scarce central Yangon homes with clean title and reliable power still give sellers some leverage.

Myanmar does not publish a reliable months of inventory series, but our closest proxy suggests weak stock may sit for many months while strong Yangon stock clears faster.

We cannot verify an official share of price reduced listings, but repeated portal checks suggest negotiation is common outside the best Yangon buildings, which reduces seller power.

We have made this infographic to give you a quick and clear snapshot of the property market in Myanmar. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Are homes overpriced, or fairly priced in Burma (Myanmar) as of 2026?

Are homes overpriced versus rents or versus incomes in Burma (Myanmar) as of 2026?

As of 2026, homes in Burma (Myanmar) look expensive versus normal local incomes, but some Yangon condos can look fairly priced versus rents if the buyer gets a real discount.

The estimated Yangon price to rent ratio for well bought condos can be around 4 to 8 years, which is below many balanced market benchmarks, but this low ratio mainly reflects high risk.

The estimated price to income multiple is much less comfortable, because even a mid market Yangon condo can cost far more than what ordinary households can finance safely.

Finally please note that you will have all the indicators you need in our property pack covering the real estate market in Burma (Myanmar).

Are home prices above the long-term average in Burma (Myanmar) as of 2026?

As of 2026, Burma (Myanmar) home prices are almost certainly above long term averages in nominal kyat terms, but not clearly above prior peaks in real hard currency terms.

The estimated recent 12 month price change for good Yangon condos is roughly flat to up 10% in kyat terms, which is not strong once inflation is considered.

In inflation adjusted terms, many Myanmar homes are probably below their prior cycle peak, especially outside prime Yangon, because the kyat has lost purchasing power.

Get fresh and reliable information about the market in Myanmar

Don't base significant investment decisions on outdated data. Get updated and accurate information.

What local changes could move prices in Burma (Myanmar) as of 2026?

Are big infrastructure projects coming to Burma (Myanmar) as of 2026?

As of 2026, the single most important infrastructure project for residential prices in Burma (Myanmar) is the Yangon Circular Railway upgrade, which can support selected station areas but should not be treated as a national price catalyst.

The project has been in implementation for years, and the realistic price impact depends on operating reliability, service frequency, safety, and whether nearby townships get better daily access.

For the latest updates on the local projects, you can read our property market analysis about Myanmar here.

Are zoning or building rules changing in Burma (Myanmar) as of 2026?

The most important rule issue in Burma (Myanmar) is not one simple national zoning change, but the growing importance of Yangon permits, inspections, completion certificates, and post earthquake building safety checks.

As of 2026, stricter attention to permits and building completion rules can support safer supply in Yangon, but it can also raise development costs and slow weaker projects.

The most affected areas are dense Yangon townships such as Bahan, Sanchaung, Kamaryut, Yankin, Hlaing, Ahlone, Kyauktada, Tamwe, and Mingalar Taung Nyunt, where building quality and legal paperwork matter most.

Are foreign-buyer or mortgage rules changing in Burma (Myanmar) as of 2026?

As of 2026, foreign buyer and mortgage rules in Burma (Myanmar) do not show a clear liberalization that would lift national prices, so the impact on residential demand remains narrow.

The most likely foreign buyer issue is enforcement of existing condominium rules, because foreigners are generally focused on compliant condominium units and the foreign share is capped.

The most likely mortgage issue is not a new LTV boom, but continued shallow housing finance, which means cash buyers still matter more than ordinary leveraged buyers in Myanmar.

Buying real estate in Myanmar can be risky

An increasing number of foreign investors are showing interest. However, 90% of them will make mistakes. Avoid the pitfalls with our comprehensive guide.

Will it be easy to find tenants in Burma (Myanmar) as of 2026?

Is the renter pool growing faster than new supply in Burma (Myanmar) as of 2026?

As of 2026, renter demand for safe and serviced homes in Burma (Myanmar) is probably growing faster than good quality rental supply, especially in central and western Yangon.

The best renter demand signal is displacement and urban safety seeking, but only part of that demand can pay market rent in Yangon apartments and condos.

The best supply signal is that new high quality completions are constrained by financing, permits, materials, power issues, and stricter buyer attention after the 2025 earthquake.

Are days-on-market for rentals falling in Burma (Myanmar) as of 2026?

As of 2026, good Yangon rentals in Burma (Myanmar) probably take around 30 to 60 days to rent, and time to let looks stable or falling for the best managed units.

In best areas like Bahan, Yankin, Kamaryut, Sanchaung, Hlaing, Ahlone, and Kyauktada, good furnished units may rent in one to two months, while weaker units can take three to six months.

One reason rental days can fall in Yangon is that tenants are not only choosing by price, but also by power reliability, building management, security, and access to hospitals, schools, and offices.

Are vacancies dropping in the best areas of Burma (Myanmar) as of 2026?

As of 2026, vacancies are likely dropping first in Bahan, Yankin, Kamaryut, Sanchaung, Hlaing, Ahlone, Kyauktada, and selected Thanlyin projects, while weaker areas remain loose.

Our estimate is that prime Yangon condo vacancy is around 5% to 10%, acceptable mid market units are around 10% to 18%, and weak or remote stock can be above 20%.

A practical landlord signal in Myanmar is that tenants ask early about generators, water pressure, lifts, security, and internet before negotiating rent, because livability is now a rental filter.

Make a profitable investment in Myanmar

Better information leads to better decisions. Save time and money. Download our data.

Am I buying into a tightening market in Burma (Myanmar) as of 2026?

Is for-sale inventory shrinking in Burma (Myanmar) as of 2026?

As of 2026, it is hard to estimate total for sale inventory in Burma (Myanmar), but clean, well managed, generator backed Yangon stock appears much tighter than ordinary listings suggest.

The closest months of supply proxy suggests prime Yangon homes may have moderate supply, while ordinary or weak location homes can remain available for many months.

The most likely reason prime inventory is tight is that owners of good Yangon property often prefer holding a hard asset rather than selling into inflation and currency uncertainty.

Are homes selling faster in Burma (Myanmar) as of 2026?

As of 2026, well priced Yangon homes in Burma (Myanmar) may sell in around 60 to 120 days, but the broader market is not clearly speeding up.

Compared with last year, median selling time is probably flat or longer for ordinary homes, while discounted central Yangon condos can still move faster than the market average.

Are new listings slowing down in Burma (Myanmar) as of 2026?

As of 2026, we are not confident enough to give a precise year over year change in new for sale listings in Burma (Myanmar), but new quality supply looks slower than normal.

The seasonal listing pattern is also hard to read because conflict, inflation, power problems, and the 2025 earthquake matter more than normal seasonality in Myanmar.

The most plausible reason new quality listings are slowing is seller caution, because many owners of good Yangon assets do not want to convert property into cash during inflation.

Is new construction failing to keep up in Burma (Myanmar) as of 2026?

As of 2026, new construction in Burma (Myanmar) is failing to keep up with demand for safe, serviced, affordable urban housing, especially in Greater Yangon.

The recent trend in permits and completions is hard to measure publicly, but YCDC permit and completion requirements show that formal new supply faces more procedural and quality hurdles.

The biggest bottleneck is not only permitting, but also financing, imported materials, power reliability, and buyer fear after the 2025 earthquake.

Get to know the market before buying a property in Myanmar

Better information leads to better decisions. Get all the data you need before investing a large amount of money.

Will it be easy to sell later in Burma (Myanmar) as of 2026?

Is resale liquidity strong enough in Burma (Myanmar) as of 2026?

As of 2026, resale liquidity in Burma (Myanmar) is only strong enough for prime Yangon homes that are legally clean, well maintained, fairly priced, and easy to rent.

The estimated median days on market for good resale homes in Yangon is around 90 to 180 days, which is slower than a very liquid market but workable for patient sellers.

The property characteristic that most improves resale liquidity in Myanmar is a clean condominium or apartment title in a central Yangon township with reliable power and good building management.

Is selling time getting longer in Burma (Myanmar) as of 2026?

As of 2026, selling time in Burma (Myanmar) is likely longer than the last normal period for ordinary homes, because buyers face weak incomes, weak credit, and high uncertainty.

The current realistic range is around 3 to 6 months for good Yangon condos, 6 to 12 months for ordinary homes, and more than 12 months for large luxury or weak location homes.

A clear reason selling time can lengthen in Myanmar is that many buyers like the idea of owning property, but fewer buyers can safely pay cash or access usable housing finance.

Is it realistic to exit with profit in Burma (Myanmar) as of 2026?

As of 2026, the chance of exiting with a nominal kyat profit in Burma (Myanmar) is medium for a well bought Yangon condo, but the chance of a real hard currency profit is low to medium.

The minimum holding period that makes profit more realistic is usually at least five years, because resale liquidity, currency risk, fees, and negotiation can eat short term gains.

For a MMK 100 million property, a rough round trip cost drag can easily reach MMK 5 million to MMK 10 million, which is about USD 1,100 to USD 2,400 or EUR 1,000 to EUR 2,200 at a rough MMK 4,200 per USD reference rate.

The clearest factor that improves profit odds in Myanmar is buying below comparable listings in a prime Yangon area where tenants pay for safety, power reliability, and convenience.

We made this infographic to show you how property prices in Myanmar compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it’s in our blog articles or the market analyses included in our property pack about Burma (Myanmar), we always rely on the strongest methodology we can, and we don’t throw out numbers at random.

We also aim to be fully transparent, so below we’ve listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why this source matters | How we used it |

|---|---|---|

| World Bank Myanmar Economic Monitor | It is one of the strongest public sources for Myanmar macro conditions. | We used it to frame growth, inflation, poverty, conflict risk, power shortages, and household stress. We treated it as macro evidence, not a property price index. |

| ADB Asian Development Outlook April 2026 Myanmar | ADB gives a regional check on Myanmar’s economic outlook. | We used it to cross check weak growth, high inflation, and downside risk. We used it as a confidence check beside the World Bank. |

| World Bank June 2025 earthquake assessment | It explains the economic damage from the 2025 earthquake. | We used it to judge reconstruction pressure and buyer caution. We did not assume reconstruction demand automatically lifts prices. |

| Central Statistical Organization Myanmar | It is Myanmar’s official statistics agency. | We used it for national economic and demographic context. We used it to avoid relying only on real estate portals. |

| 2024 Population and Housing Census highlights | It is the official housing structure source for Myanmar. | We used it to understand common residential property types. We used it to separate national housing reality from urban investment stock. |

| OCHA Myanmar Humanitarian Needs and Response Plan 2026 | It is the main UN planning source for 2026 humanitarian needs. | We used it to assess displacement, shelter pressure, and household stress. We treated shelter need separately from paying rental demand. |

| UNHCR Myanmar displacement data | UNHCR is a key source for displacement data. | We used it to understand renter pressure and urban safety seeking. We did not treat displacement alone as prime rent demand. |

| Central Bank of Myanmar interest rate data | CBM is Myanmar’s official monetary authority. | We used it to understand credit and mortgage conditions. We treated housing finance as shallow compared with cash buying. |

| Myanmar Condominium Law 2016 | It is the legal base for condominium ownership and foreign eligibility. | We used it to distinguish condos from ordinary apartments and land backed homes. We used it to explain the 40% foreign ownership cap. |

| Yangon Building Permit System, YCDC | YCDC controls formal building permits in Yangon. | We used it to understand permits, inspections, and completion certificates. We treated it as supply and quality evidence. |

| Myanmar National Portal city development documents | It lists official planning and development documents. | We used it to check Yangon zoning and development permit context. We focused on Yangon because rule changes matter most there. |

| JICA Yangon Circular Railway project | JICA is a major infrastructure planner and financier in Myanmar. | We used it to assess transport led value potential in Yangon. We treated it as a location factor, not a price guarantee. |

| JICA Greater Yangon strategic plan | It is one of the clearest public sources on Greater Yangon planning. | We used it for long term housing demand and township pressure. We cross checked it with infrastructure and permit sources. |

| ShweProperty Yangon sale listings | It is a major Myanmar property portal with current asking prices. | We used it for live Yangon sale price benchmarks. We discounted asking prices because they are not completed transaction prices. |

| ShweProperty Yangon rental listings | It shows current rental asking levels in Yangon. | We used it to estimate rent bands and gross yields. We reduced the weight because posted rents can be negotiated. |

| iMyanmarHouse Yangon condo listings | It is another large Myanmar property portal. | We used it to cross check sale price ranges and township coverage. We used it with caution because listings can be duplicated or stale. |

Don't buy the wrong property, in the wrong area of Myanmar

Buying real estate is a significant investment. Don't rely solely on your intuition. Gather the right information to make the best decision.