Authored by the expert who managed and guided the team behind the Philippines Property Pack

Yes, the analysis of Cebu's property market is included in our pack

Cebu's property market offers diverse investment opportunities across condos, townhouses, and house-and-lot properties, with prices ranging from ₱1.7M for budget options to ₱40M+ for luxury units as of September 2025.

The city's real estate landscape spans from prime areas like IT Park and Business Park commanding ₱150k+ per square meter, to emerging neighborhoods in Mandaue and Lapu-Lapu offering better value at ₱90k-₱120k per square meter, making it accessible for various investment strategies and budgets.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

Cebu's property market offers condos from ₱900k for studios to ₱40M for luxury units, townhouses from ₱2.5M to ₱32M, and house-and-lot properties from ₱3M to ₱32M, with rental yields of 4-7% and annual price growth of 5-7%.

Prime areas like IT Park and Business Park command premium prices above ₱150k/sqm, while emerging areas like Mandaue and Lapu-Lapu offer better value at ₱90k-₱120k/sqm for investors seeking growth potential.

| Property Type | Price Range (₱) | Best Areas | Rental Yield |

|---|---|---|---|

| Studio Condo | 900k - 1.5M | IT Park, Lahug | 6-8% |

| 1-2BR Condo | 2M - 15M | Business Park, Banilad | 5-7% |

| Townhouse | 2.5M - 32M | Guadalupe, Mandaue | 3.5-5.5% |

| House & Lot | 3M - 32M | Banawa, Talisay | 3.5-5% |

| Luxury Units | 20M+ | Maria Luisa, Banawa Heights | 3-4% |

| Land Only | Variable | Minglanilla, Danao | N/A |

What property types are available in Cebu right now?

Cebu's property market offers four main types of residential real estate as of September 2025.

Condominiums are the most accessible option for foreigners and provide the highest rental yields, particularly in business districts like IT Park and Cebu Business Park. Studio units start at ₱900k while luxury 3-bedroom units can reach ₱40M. These properties typically offer amenities like swimming pools, gyms, and 24/7 security.

Townhouses appeal to small families seeking more privacy and space, with prices ranging from ₱2.5M in budget areas like Danao to ₱32M for premium units in established subdivisions. Most townhouses include 3-4 bedrooms, private parking, and small garden areas within gated communities.

House-and-lot properties cater to families wanting maximum space and privacy, with new single detached homes in inner city areas costing ₱13M-₱32M, while suburban options in Talisay or Consolacion range from ₱3M-₱10M. These properties typically feature 3-5 bedrooms, multiple parking spaces, and larger yards.

Land-only purchases serve investors focused on development or land banking strategies, offering the lowest holding yields but potential for future development profits in emerging areas like Minglanilla and outer Mandaue.

Should you buy to live in, rent short-term, rent long-term, or flip?

Your investment strategy determines which property type and location will maximize your returns in Cebu's current market.

Buy-to-live investors should focus on condos in central locations like Lahug, IT Park, or Business Park for convenience to work and amenities. Studio to 2-bedroom units (₱900k-₱15M) work best for singles and couples, while families should consider 3-bedroom townhouses in Banawa, Guadalupe, or suburban Mandaue (₱6.5M-₱17M).

Short-term rental investors achieve the highest yields with studio and 1-bedroom condos near business districts, universities, and tourist areas. Prime locations include IT Park, Lahug, and Mactan/Lapu-Lapu near resorts and beaches, where net yields can reach 7-8% annually after all costs.

Long-term rental strategies work best with 1-2 bedroom condos in residential areas like Banilad and Talamban, or family townhouses in central barangays. These properties typically generate 4.8-6% net yields for condos and 3.5-5.5% for townhouses and houses.

Property flipping opportunities exist in pre-selling developments in emerging areas like Mandaue, Minglanilla, and Talisay, or through renovation of older properties in established areas like Banilad and Guadalupe. Successful flips can generate 10-25% returns but require 6-18 months for ready units or 2-4 years for off-plan properties.

Which neighborhoods offer the best value in different price segments?

| Segment | Key Areas | Price per sqm | Property Types Available |

|---|---|---|---|

| Prime (Luxury) | IT Park, Business Park, Maria Luisa, Banawa Heights | ₱150k+ per sqm | High-end condos, luxury houses |

| Up-and-Coming | Mandaue, Lapu-Lapu/Mactan, Guadalupe, Talamban, Banilad | ₱90k-₱120k per sqm | All property types |

| Budget-Friendly | Tipolo (Mandaue), Bakilid, Danao, Talisay, Minglanilla | ₱50k-₱80k per sqm | Condos, townhouses, house-and-lot |

| Tourist/Resort | Mactan Island, Lapu-Lapu coastal areas | ₱100k-₱140k per sqm | Resort condos, vacation homes |

| University Areas | Near USC, UP Cebu, University belt | ₱80k-₱110k per sqm | Studio condos, boarding houses |

What should you budget for total acquisition costs?

Your all-in budget must include purchase price plus additional costs that typically add 15-25% to the base property price.

For a mid-range condo costing ₱4M, expect total costs of ₱4.6M-₱5.2M including transfer taxes (1.5%), documentary stamps (1.5%), notary fees, registration costs, and first year association dues. Furnishing a rental-ready unit adds ₱200k-₱800k depending on quality and size.

Townhouses and house-and-lot properties in the ₱8M-₱15M range require ₱9.2M-₱17.5M total budget, with higher annual property taxes and maintenance reserves. Association fees for gated communities range from ₱2k-₱8k monthly depending on amenities.

Financing scenarios typically require 20% down payment for bank loans, with the balance payable over 10-20 years at 5.5-7% interest rates. A ₱4M property would need ₱800k down payment and monthly payments of approximately ₱29k for 20 years at 6% interest.

Pre-selling developments often allow 10-20% down payment spread over 18-48 months, making initial cash requirements lower but with delivery risk 2-4 years out.

What financing options and terms are available right now?

Cebu property financing in September 2025 offers several pathways depending on your buyer profile and property type.

Bank financing requires 20% down payment with interest rates ranging from 5.5% to 7% for the first 1-5 years, then adjusting to prevailing rates. Loan terms extend up to 20 years for condos and 25 years for house-and-lot properties. Monthly payments on a ₱4M loan at 6% over 20 years equal approximately ₱29k.

Pag-IBIG housing loans offer government-backed financing with slightly lower rates (around 5-6%) and longer terms up to 30 years, but with stricter income requirements and property value limits. Maximum loanable amount is ₱6M, making it suitable for budget to mid-range properties.

Developer financing allows more flexible terms, particularly for pre-selling units. Down payments can be as low as 10% spread over construction period, with balance due on turnover. Interest rates vary but typically match or slightly exceed bank rates.

Foreign buyers face additional requirements including proof of dollar income, local co-borrower for some banks, and compliance with foreign ownership restrictions. Condominiums remain the most accessible option as foreigners can own individual units but not land titles directly.

Don't lose money on your property in Cebu

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What sizes and configurations should you target?

Property size and configuration significantly impact both purchase price and rental potential in Cebu's current market.

Studio condos ranging from 22-30 square meters suit single professionals and generate highest yields per square meter, with prices from ₱900k-₱1.5M. These units work best for short-term rentals near business districts and universities.

One-bedroom condos (28-40 sqm) accommodate couples and small families, priced ₱2M-₱6M depending on location and building quality. Two-bedroom units (45-65 sqm) serve growing families and professionals needing home office space, typically costing ₱4M-₱15M in prime locations.

Parking spaces add ₱800k-₱1.2M to condo purchases but increase rental marketability and resale value significantly. Most tenants and buyers prioritize covered parking, especially in business districts.

Townhouses typically offer 3-4 bedrooms across 80-120 square meters of floor area, with 1-2 parking spaces and small private gardens. House-and-lot properties range from 160-320+ square meters with 2+ parking spaces and larger yards suitable for families with children.

Essential amenities include reliable internet connectivity, backup water systems, and professional security. Swimming pools, gyms, and function halls in condo buildings command rental premiums but also increase monthly association dues.

Should you buy pre-selling or ready-for-occupancy properties?

Pre-selling and ready-for-occupancy properties each offer distinct advantages depending on your investment timeline and risk tolerance.

Pre-selling units cost 10-15% less than comparable ready properties and allow staggered down payments over 18-48 months during construction. Capital appreciation potential is higher as you benefit from market growth during the 2-4 year development period. However, delivery delays and construction quality issues pose risks.

Ready-for-occupancy properties command premium pricing but allow immediate rental income or personal use. You can inspect actual units, verify build quality, and avoid construction delays. Established buildings often have proven rental histories and functioning amenities.

Developer reputation is crucial for pre-selling purchases. Established names like Cebu Landmasters, Ayala Land, and Filinvest have strong track records, while unknown developers may offer lower prices but higher default risk. Research completion timelines, previous projects, and financial stability before committing.

Payment structures differ significantly - pre-selling typically requires 10-20% down payment during construction with balance due on turnover, while ready properties need 20% down payment and 80% financing or cash at closing.

It's something we develop in our Philippines property pack.

What are actual selling prices by area and property type?

Current market prices in September 2025 show clear segmentation across Cebu's various districts and property types.

Cebu City and Lahug condos average ₱157k per square meter, with Be Residences Lahug offering 1-3 bedroom units from ₱5M-₱40M. The Median Flats near IT Park provides studios to lofts priced ₱4M-₱15M. Mivela Garden Residences in Banilad offers studios and 1-bedroom units from ₱4M-₱10M.

Prime CBD resale condos command premium prices, with studios starting at ₱900k-₱1.5M and 1-bedroom units ranging ₱2M-₱5M. Luxury 2-3 bedroom units in premium buildings can reach ₱15M-₱40M depending on floor level, view, and building amenities.

Townhouse pricing varies significantly by location - new 3-4 bedroom units (80-111 sqm) in central areas cost ₱6.5M-₱11M, while pre-owned larger units with bigger lots range ₱14M-₱32M. Budget options in Mandaue start at ₱2.5M-₱3.5M, with Danao properties available from ₱1.7M-₱2.8M.

House-and-lot properties show the widest price range, with new single detached homes (3-5 bedrooms, 180-300 sqm) in inner city areas costing ₱13M-₱32M. Suburban family homes in Talisay and Consolacion offer better value at ₱3M-₱10M for comparable space and amenities.

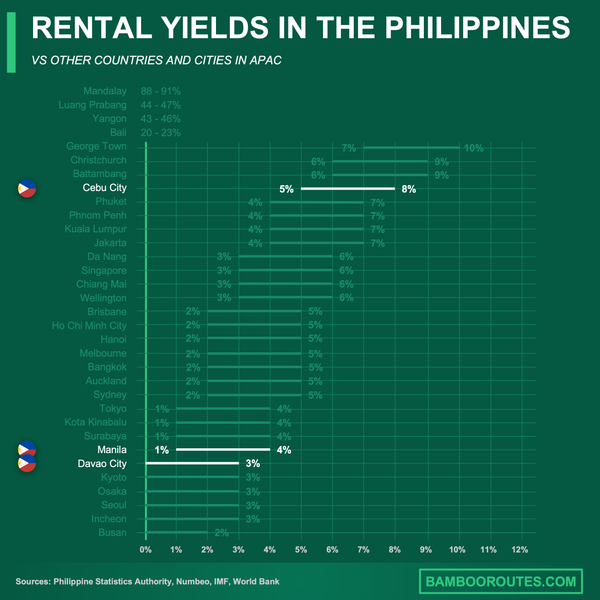

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

How have prices moved and what's the outlook?

Cebu property prices have shown consistent growth over the past five years with positive forecasts through 2035.

The overall market experienced 5-7% annual price appreciation from 2020-2025, outpacing inflation and most investment alternatives. Condos averaged ₱157k per square meter in 2025, representing significant increases from ₱120k-₱130k per square meter in 2020. Studios that cost ₱750k-₱1.2M in 2020 now start at ₱900k-₱1.5M.

Townhouses and subdivisions have seen 30-40% price increases over five years for new inventory, driven by land scarcity and construction cost inflation. The most recent 12-month trend shows 4-6% growth for condos and mid-market properties, while luxury segments remained stable and budget properties in Mandaue and Danao rose faster.

Five-year projections indicate 5-8% compound annual growth rates in urban and suburban Cebu, supported by BPO industry expansion, tourism recovery, and infrastructure development including new bridges and airport improvements. Transit-oriented development along future mass transport corridors will likely see above-average appreciation.

Ten-year outlook suggests continued compounding returns for well-located properties, though investors should consider macro risks including interest rate changes, foreign exchange fluctuations, and climate change impacts. Price appreciation will likely be strongest in transit-linked areas like Mandaue and Mactan, while luxury segments may lag unless foreign capital returns significantly.

What rental yields can you expect after all costs?

Net rental yields in Cebu vary significantly by property type, location, and management strategy after accounting for all operating expenses.

Condos operated as short-term rentals (Airbnb) in prime locations like IT Park, Lahug, and Lapu-Lapu generate 5-7% net yields annually, with exceptional properties reaching 8-9% during peak occupancy periods. These yields account for association dues (₱80-₱120 per sqm monthly), vacancy periods, utility costs, and management fees.

Long-term condo rentals produce more predictable 4.8-6% net yields with lower management overhead but also lower gross rental rates. Properties in business districts typically achieve higher occupancy rates and can command premium rents from BPO employees and expatriate workers.

Townhouses and house-and-lot properties generate 3.5-5.5% net yields for long-term rentals, with returns varying based on property age, location accessibility, and maintenance requirements. Family-oriented properties in good school districts and safe neighborhoods typically achieve higher occupancy rates.

Budget and lower-mid-tier properties often outperform luxury units on yield metrics due to stronger tenant demand and lower relative operating costs as percentage of gross income. However, luxury properties may appreciate faster in capital value over time.

It's something we develop in our Philippines property pack.

What about property flipping - timeline, costs, and margins?

Property flipping in Cebu can generate attractive returns but requires careful planning and market timing for optimal results.

Ready-for-occupancy properties in prime locations typically sell within 6-18 months if priced competitively, while off-plan purchases require waiting 2-4 years until project completion before potential resale. Central Cebu, Mandaue, and Lapu-Lapu units usually have the fastest absorption rates when priced fairly for current market conditions.

Total costs for flipping include renovation expenses (₱10k-₱20k per square meter for quality upgrades), closing costs and agent fees (3-5% of sale price), capital gains tax (6%), documentary stamps (1.5%), and miscellaneous administrative expenses. These costs can significantly impact net profits if not budgeted properly.

Successful flips in the right micro-markets after light renovation typically generate 10-15% returns on total invested capital. Off-plan purchases in surging submarkets can potentially yield up to 25% on leveraged deals, though average returns are more modest at 7-12% due to increased competition and occasional delivery delays.

The most profitable flip strategies focus on mid-market properties with proven end-user demand rather than ultra-luxury units that may have limited buyer pools. Properties requiring cosmetic improvements rather than major structural work typically offer the best risk-adjusted returns.

Market absorption rates vary by location and price point, with well-priced units in established areas typically selling within 3-6 months while overpriced or poorly located properties may take 12+ months to find buyers.

What are the smartest investment choices by strategy?

The optimal property choice depends entirely on your primary investment objective and risk tolerance in Cebu's current market environment.

Live-in buyers should prioritize ready-for-occupancy 1-2 bedroom condos in Lahug, Banilad, or IT Park for convenience to business districts and urban amenities. Families benefit more from 3-bedroom townhouses in Banawa, Guadalupe, or suburban Mandaue that offer more space, privacy, and potential for customization.

Short-term rental investors achieve highest returns with studio and 1-bedroom condos in IT Park, Lapu-Lapu/Mactan near resorts, or areas close to major universities where transient demand remains strong year-round. Properties with amenities like pools and gyms command rental premiums.

Long-term rental strategies work best with townhouses or lower-mid-tier condos in residential areas like Talamban, Guadalupe, Banilad, or Mandaue where families and professionals seek stable housing. These locations offer good tenant quality with reasonable vacancy rates.

Property flippers should focus on pre-selling condos in emerging areas like Mandaue, Talisay, or CBD edge locations, or identify renovation opportunities in established areas like Guadalupe and Banilad where improvements can add significant value.

It's something we develop in our Philippines property pack.

How does Cebu compare to other major cities?

Cebu's property market positioning offers distinct advantages compared to other major Philippine and Southeast Asian cities as of September 2025.

Within the Philippines, Cebu's 5-7% annual price appreciation outpaces most secondary cities while maintaining lower entry costs than Metro Manila. Studio condos in Cebu (₱900k-₱1.5M) cost significantly less than comparable Manila units (₱2M+), while generating higher rental yields of 6-8% versus Manila's 4.5-6%.

Compared to Davao, Cebu offers stronger yields and appreciation potential driven by more diverse economic drivers including BPO, tourism, and manufacturing. The city's established infrastructure and international connectivity provide advantages over smaller regional centers.

On the broader ASEAN scale, Cebu remains more affordable than Bangkok, Kuala Lumpur, and Singapore while offering competitive net yields. However, capital gains potential may be smaller than Thai resort destinations or Indonesian growth markets that benefit from stronger foreign investment flows.

Cebu's unique advantages include its position as the Philippines' second city, established BPO industry, growing tourism sector, and relative political stability. The combination of affordability, yield potential, and growth prospects makes it attractive for both regional and international property investors seeking portfolio diversification in Southeast Asia.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

Cebu's property market offers compelling opportunities across all investment strategies, with studio condos and budget townhouses providing the highest yields and most flexible options for domestic and foreign investors.

The combination of affordable entry points, strong rental demand from BPO workers and tourists, and projected 5-8% annual price growth makes Cebu one of the Philippines' most attractive secondary property markets for 2025 and beyond.