Authored by the expert who managed and guided the team behind the Philippines Property Pack

Get all the data you need about the real estate market in Central Luzon

We constantly update this blog post so buyers can follow the Central Luzon property market with fresh 2026 data, not old market noise.

Central Luzon is one of the most watched residential property markets in the Philippines because Pampanga, Bulacan, Clark, Tarlac, Subic and Bataan are all tied to jobs, transport and Metro Manila spillover.

The simple question is whether buying a house, townhouse, condo or apartment in Central Luzon in June 2026 still makes sense, or whether prices already include too much future growth.

And if you’re planning to buy a property in this place, you may want to download our pack covering the real estate market in Central Luzon.

So, is now a good time?

As of June 2026, Central Luzon is a rather yes for buying residential property, but only if you buy in a real job corridor and avoid paying too much for future infrastructure promises.

The strongest signal is that Central Luzon has real demand from population growth, Clark expansion, logistics parks, industrial jobs and Metro Manila households looking north.

Another strong signal is that high mortgage rates are keeping buyers careful, which gives patient buyers more room to negotiate than during the boom years.

Other strong signals are the North-South Commuter Railway, New Manila International Airport, New Clark City, Subic and the Luzon Economic Corridor, which all support long-term housing demand.

The best strategy is to target liquid houses, townhouses or well-located condos in Pampanga, Bulacan, Clark, Angeles, San Fernando, Malolos, Marilao, Meycauayan, Subic, Balanga or Tarlac City, then hold for the medium or long term.

This is not financial or investment advice, we do not know your personal situation, and you should always do your own research before buying property in Central Luzon.

Is it smart to buy now in Central Luzon, or should I wait as of 2026?

Do real estate prices look too high in Central Luzon as of 2026?

As of 2026, residential property prices in Central Luzon look about 5% to 15% above what local incomes alone would justify, but they look closer to fair value in areas where jobs, schools, hospitals and transport are already visible.

This is why the most useful listing signal is not the headline asking price, but the fact that buyers can often negotiate around 5% to 12% on resale homes in Central Luzon when the seller is not in a prime Clark, Angeles, San Fernando, Malolos or Marilao location.

A second signal is that developer projects in Pampanga and Bulacan still sell the infrastructure story hard, which means the buyer should check whether the price is based on today’s access or on a promise that may arrive years later.

You can also read our latest update regarding the housing prices in Central Luzon.

Does a property price drop look likely in Central Luzon as of 2026?

As of 2026, the risk of a meaningful property price decline in Central Luzon looks medium for weak condo and fringe subdivision projects, but low for good homes near Clark, Angeles, San Fernando, Malolos, Marilao, Meycauayan and Subic.

Over the next 12 months, a realistic Central Luzon price range is roughly 3% down to 5% up in real terms, with individual overpriced units sometimes falling 10% to 15% if the seller needs cash.

The most important macro factor is mortgage affordability, because the BSP target reverse repurchase rate was still 4.50% in early June 2026 and actual home loan rates remain high enough to slow buyers.

A sharp rate shock looks less likely than a slow affordability squeeze, so a broad Central Luzon crash would probably need a bigger jobs, remittance or credit problem than the market currently shows.

Finally, please note that we cover the price trends for next year in our pack about the property market in Central Luzon.

Could property prices jump again in Central Luzon as of 2026?

As of 2026, the chance of a renewed price surge in Central Luzon looks medium in the best nodes, but low across the whole region because financing costs still limit how much buyers can pay.

A plausible upside range for good Central Luzon residential property over the next 12 months is about 5% to 9% in nominal terms, while ordinary homes away from jobs and transport may rise only 2% to 5%.

The biggest demand trigger would be easier credit, because lower mortgage rates would immediately help families, OFWs and Metro Manila spillover buyers compete for homes in Pampanga, Bulacan and Clark-linked areas.

Please also note that we regularly publish and update real estate price forecasts for Central Luzon here.

Are we in a buyer or a seller market in Central Luzon as of 2026?

As of 2026, Central Luzon is a mixed market, with seller-leaning conditions for good houses and townhouses in prime Pampanga and Bulacan areas, but buyer-leaning conditions for weaker condos, remote subdivisions and expensive developer inventory.

A fair market proxy is around 4 to 7 months of saleable supply in the better family-home areas and more than 8 months in weaker or premium inventory, which means bargaining power depends heavily on the exact property type.

We estimate that about 15% to 25% of active resale listings in normal Central Luzon areas show some price flexibility, while the best land-backed homes near jobs often have less visible discounting.

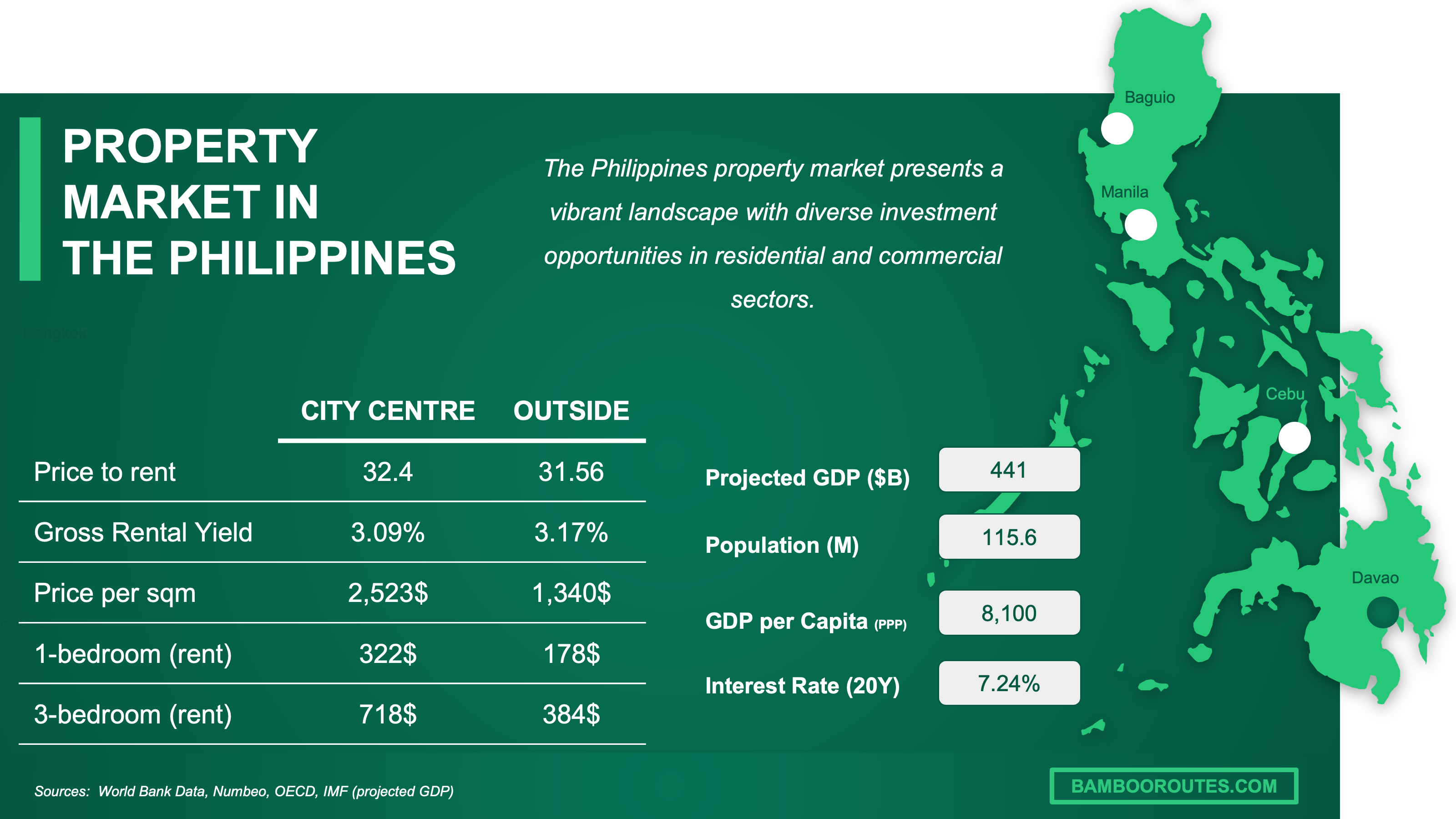

We have made this infographic to give you a quick and clear snapshot of the property market in the Philippines. It highlights key facts like rental prices, yields, and property costs both in city centers and outside, so you can easily compare opportunities. We’ve done some research and also included useful insights about the country’s economy, like GDP, population, and interest rates, to help you understand the bigger picture.

Are homes overpriced, or fairly priced in Central Luzon as of 2026?

Are homes overpriced versus rents or versus incomes in Central Luzon as of 2026?

As of 2026, homes in Central Luzon look mildly expensive versus rents and stretched versus local incomes, but still workable for dual-income families, OFWs, business owners and Metro Manila buyers with equity.

The estimated Central Luzon price-to-rent ratio is roughly 15 to 22 for normal homes and condos, while a balanced market is often closer to 14 to 18, so rental yield is acceptable only when the rent is strong.

The estimated price-to-income multiple is roughly 13 to 24 times average annual family income for homes priced from PHP 5 million to PHP 9 million, which is far above a comfortable affordability range for many local households.

Finally please note that you will have all the indicators you need in our property pack covering the real estate market in Central Luzon.

Are home prices above the long-term average in Central Luzon as of 2026?

As of 2026, Central Luzon home prices are probably 10% to 25% above their long-term trend in ordinary provincial areas and 20% to 40% above 2019 levels in prime Pampanga and Bulacan nodes.

The recent 12-month price change appears flat to mildly positive in many Central Luzon submarkets, which is slower than the post-pandemic infrastructure excitement but still firmer than a weak market would be.

After inflation, the price position looks less extreme, so the main risk is not a region-wide bubble but buying a specific project where the future rail, airport or township premium is already too high.

Get fresh and reliable information about the market in Central Luzon

Don't base significant investment decisions on outdated data. Get updated and accurate information.

What local changes could move prices in Central Luzon as of 2026?

Are big infrastructure projects coming to Central Luzon as of 2026?

As of 2026, the single biggest infrastructure project for Central Luzon residential prices is the North-South Commuter Railway, because it can make Bulacan, Pampanga and Clark feel much closer to Metro Manila jobs and airports.

The rail project has already moved through years of funding, right-of-way and construction work, but buyers should still treat full delivery as staged, with the biggest price impact likely near actual stations once travel times become real.

For the latest updates on the local projects, you can read our property market analysis about Central Luzon here.

Are zoning or building rules changing in Central Luzon as of 2026?

The most important rule issue in Central Luzon in 2026 is not one single region-wide zoning shock, but the continued conversion of land around Bulacan, Pampanga, Tarlac and Clark from agricultural or low-density use into housing, logistics and township use.

As of 2026, these changes should support prices in well-planned growth corridors, but they can also create flood, traffic and permitting risks when residential projects move faster than roads, drainage and public services.

The areas most affected are Malolos, Bulakan, Marilao, Meycauayan, San Fernando, Mexico, Mabalacat, Capas, Tarlac City and the edges of Clark and New Clark City, where land-use change is part of the property story.

Are foreign-buyer or mortgage rules changing in Central Luzon as of 2026?

As of 2026, there is no clear foreign-buyer liberalization that would strongly lift Central Luzon prices, while mortgage conditions remain the bigger short-term force because borrowing costs still limit buyer budgets.

The most likely foreign-buyer rule change is not a new open-door policy, but continued enforcement of the existing system where foreigners generally cannot own land directly and usually access the market through condominium ownership.

The most likely mortgage change is gradual rate easing rather than a sudden rule shift, which would help monthly affordability in Central Luzon but would not instantly make overpriced homes cheap.

You can also read our latest update about mortgage and interest rates in The Philippines.

Buying real estate in Central Luzon can be risky

An increasing number of foreign investors are showing interest. However, 90% of them will make mistakes. Avoid the pitfalls with our comprehensive guide.

Will it be easy to find tenants in Central Luzon as of 2026?

Is the renter pool growing faster than new supply in Central Luzon as of 2026?

As of 2026, renter demand is probably growing faster than quality rental supply in Clark, Angeles, Mabalacat, San Fernando and selected Bulacan commuter nodes, but not in every Central Luzon subdivision or condo project.

The best demand signal is that Central Luzon reached about 13 million people in 2024 and continues to benefit from Metro Manila spillover, industrial hiring, airport activity, schools and healthcare demand.

Supply is also rising through new townships, subdivisions and condos, so landlords should focus on furnished, internet-ready homes near jobs, malls, transport, hospitals and schools rather than assuming every rental will fill quickly.

Are days-on-market for rentals falling in Central Luzon as of 2026?

As of 2026, rental days-on-market in Central Luzon look stable to falling in the best areas, with good furnished rentals near Clark and Angeles often leasing in about 20 to 45 days.

The gap is wide, because strong rentals in Clark, Angeles, San Fernando, Malolos and Subic can move in 20 to 60 days, while weak or overpriced rentals in remote subdivisions can sit for 60 to 120 days.

One local reason time-to-let can fall is that corporate tenants, BPO workers, aviation workers and relocating families often need ready-to-live homes, not empty units that still need appliances, internet and basic furniture.

Are vacancies dropping in the best areas of Central Luzon as of 2026?

As of 2026, rental vacancy looks to be dropping in Clark, Angeles, Mabalacat, San Fernando, Malolos, Marilao, Meycauayan, Subic and Balanga when units are clean, furnished and close to jobs or transport.

We estimate vacancy at about 5% to 10% for quality Clark and Angeles rentals, 7% to 12% for good San Fernando and Malolos rentals, and 10% to 18% for more ordinary or remote Central Luzon rentals.

A practical tightening sign is that landlords with furnished two-bedroom units near Clark, Angeles, San Fernando or Malolos can reject weak tenants instead of cutting rent quickly, which is not true in weaker locations.

By the way, we’ve written a blog article detailing what are the current rent levels in Central Luzon.

Make a profitable investment in Central Luzon

Better information leads to better decisions. Save time and money. Download our data.

Am I buying into a tightening market in Central Luzon as of 2026?

Is for-sale inventory shrinking in Central Luzon as of 2026?

As of 2026, for-sale inventory in Central Luzon is hard to measure officially, but we estimate good resale houses in prime nodes are down about 5% to 10% from last year while developer inventory is flat to up.

A reasonable supply proxy is about 4 to 6 months for attractive houses and townhouses in strong areas, against 7 to 10 months or more for weaker condos, remote projects and premium inventory.

The most likely reason good inventory is shrinking is seller caution, because owners of well-located land-backed homes in Pampanga and Bulacan are not eager to sell before rail, airport and Clark demand become clearer.

Are homes selling faster in Central Luzon as of 2026?

As of 2026, well-priced Central Luzon homes in strong Pampanga and Bulacan locations are selling faster than average, with a realistic median time-to-sell of about 75 to 140 days across normal resale homes.

Compared with last year, median selling time looks roughly flat to 10% shorter for good homes, but longer for overpriced premium properties or units competing against many similar developer offers.

Are new listings slowing down in Central Luzon as of 2026?

As of 2026, we estimate new resale listings in strong Central Luzon nodes are flat to down about 5%, while developer-led available inventory in Pampanga, Bulacan and township areas is up about 5% to 12%.

The usual seasonal pattern is more buyer activity around school, work and family relocation periods, and the current resale level does not look extremely low, but prime homes are not plentiful either.

The most plausible reason new resale listings are slower is that owners expect future infrastructure to lift values, so many prefer to hold rather than sell before stations, airport jobs or Clark projects mature.

Is new construction failing to keep up in Central Luzon as of 2026?

As of 2026, new construction is not failing across every part of Central Luzon, but affordable homes below about PHP 4 million near jobs and transport are not keeping up with real household demand.

Recent construction trends show active township, subdivision and condo supply in Pampanga and Bulacan, while the hardest shortage is still practical, well-located housing for families with normal local incomes.

The biggest bottleneck is land and infrastructure quality, because Central Luzon has land on paper, but buyers need flood-safe lots, road access, drainage, schools, hospitals and reliable transport.

Get to know the market before buying a property in Central Luzon

Better information leads to better decisions. Get all the data you need before investing a large amount of money.

Will it be easy to sell later in Central Luzon as of 2026?

Is resale liquidity strong enough in Central Luzon as of 2026?

As of 2026, resale liquidity in Central Luzon is strong enough for practical homes in good locations, but weak for remote lots, overpriced luxury houses, unclear-title properties and units far from jobs.

The estimated median days-on-market for normal resale homes is about 75 to 140 days, compared with a healthy liquidity benchmark of about 60 to 120 days for a market where buyers still have choices.

The property feature that most improves resale liquidity in Central Luzon is simple and specific: a flood-safe house or townhouse below PHP 8 million within daily reach of Clark, Angeles, San Fernando, Malolos, Marilao or Meycauayan.

Is selling time getting longer in Central Luzon as of 2026?

As of 2026, selling time in Central Luzon is not clearly getting longer for good homes, but it is getting longer for properties priced above local affordability or located far from proven demand.

The realistic current range is about 45 to 90 days for well-priced homes in strong nodes, 90 to 150 days for ordinary homes, and more than 180 days for expensive or poorly located properties.

The clearest reason selling time can lengthen in Central Luzon is affordability pressure, because a PHP 8 million to PHP 12 million home becomes much harder to buy when mortgage payments stay high.

Is it realistic to exit with profit in Central Luzon as of 2026?

As of 2026, the likelihood of selling with a profit in Central Luzon is medium to high for a typical long-term owner who buys below market in a job-linked area and avoids overpaying for a marketing story.

The minimum holding period that most often makes profit realistic is about 5 years, because the buyer needs time for infrastructure, rent growth and normal appreciation to overcome transaction costs.

A realistic round-trip cost drag is often about 6% to 10% of the property value, which is roughly PHP 360,000 to PHP 600,000 on a PHP 6 million home, about USD 5,900 to USD 9,800, or about EUR 5,500 to EUR 9,100 at mid-June 2026 exchange rates.

The factor that most increases profit odds is buying a liquid property at a fair entry price, especially a practical house, townhouse or well-located condo near Clark, Angeles, San Fernando, Malolos, Marilao, Meycauayan, Subic or Balanga.

We made this infographic to show you how property prices in the Philippines compare to other big cities across the region. It breaks down the average price per square meter in city centers, so you can see how cities stack up. It’s an easy way to spot where you might get the best value for your money. We hope you like it.

What sources have we used to write this blog article?

Whether it’s in our blog articles or the market analyses included in our property pack about Central Luzon, we always rely on the strongest methodology we can, and we don’t throw out numbers at random.

We also aim to be fully transparent, so below we’ve listed the authoritative sources we used, and explained how we used them and the methods behind our estimates.

| Source | Why we trust it | How we used it |

|---|---|---|

| Bangko Sentral ng Pilipinas, Residential Property Price Index | BSP is the central bank and its RPPI is the main official house-price index. | We used it to judge the national residential price cycle. We treated it as the best official price anchor because Central Luzon has no public repeat-sales index. |

| BSP Property Price Indices statistics page | This is BSP’s official portal for property price tables and technical notes. | We used it to check the latest property price releases. We used it to separate official price movement from asking-price noise. |

| BSP Key Rates | BSP policy rates directly affect mortgage affordability and buyer budgets. | We used it to assess borrowing pressure in June 2026. We treated the 4.50% target RRP rate as a key affordability input. |

| Philippine Statistics Authority, 2024 Central Luzon population | PSA is the official statistics agency for population and census data. | We used it to size the long-term housing demand base. We used Central Luzon’s 2024 population of about 13 million as a demand anchor. |

| Philippine Statistics Authority, Family Income and Expenditure Survey | FIES is the official household income and spending survey. | We used it to compare home prices with local buying power. We used Central Luzon income and expenditure data to test affordability. |

| Philippine Statistics Authority, Gross Regional Domestic Product | PSA GRDP is the official measure of regional economic output. | We used it to check whether housing demand is backed by real economic activity. We compared output trends with infrastructure and job corridors. |

| Central Luzon Regional Development Plan 2023 to 2028 | This is the official regional planning roadmap for Central Luzon. | We used it to understand the region’s growth direction. We focused on transport, logistics, industry and gateway functions. |

| Presidential Communications Office, North-South Commuter Railway update | PCO reports official government infrastructure decisions and approvals. | We used it to verify the scale and route logic of the rail project. We treated station access as more important than general regional hype. |

| Public-Private Partnership Center, New Manila International Airport | The PPP Center is the official portal for major public-private projects. | We used it to verify the Bulacan airport as an official project. We framed Bulacan as a strong but execution-sensitive market. |

| BCDA Luzon Economic Corridor projects | BCDA is central to Clark, Subic and New Clark City development. | We used it to assess Clark, Subic and New Clark City demand drivers. We focused on projects that can create jobs and tenant demand. |

| Lawphil, 1987 Philippine Constitution | Lawphil republishes core Philippine legal texts used by lawyers and courts. | We used it to confirm the land ownership limits that affect foreign buyers. We separated land-backed homes from condominium access. |

| Lawphil, Republic Act No. 4726, Condominium Act | This is the main law governing condominium ownership in the Philippines. | We used it to assess foreign-buyer access to condos. We treated condos as the main practical route for many non-Filipino buyers. |

| Philippine News Agency, balanced housing compliance | PNA is the government newswire and reports official housing enforcement. | We used it to assess developer compliance pressure. We considered socialized housing requirements as a supply-side factor. |

| Colliers, Inside the Central Luzon boom | Colliers is a major real estate consultancy with local market coverage. | We used it only where official submarket data is limited. We cross-checked its commentary with BSP, PSA and infrastructure sources. |

Don't buy the wrong property, in the wrong area of Central Luzon

Buying real estate is a significant investment. Don't rely solely on your intuition. Gather the right information to make the best decision.

Related blog posts

- What are the best areas to buy a property in property in Central Luzon?