Authored by the expert who managed and guided the team behind the Philippines Property Pack

Everything you need to know before buying real estate is included in our The Philippines Property Pack

The Philippines property market in 2025 shows steady growth with strong residential demand but faces commercial sector challenges. Residential properties are performing well, driven by overseas Filipino remittances and improving infrastructure, while office spaces struggle with high vacancy rates.

If you want to go deeper, you can check our pack of documents related to the real estate market in the Philippines, based on reliable facts and data, not opinions or rumors.

The Philippines property market demonstrates resilience with 6.5% price growth in Manila and strong demand from overseas Filipino workers.

Commercial sectors face oversupply challenges with office vacancy rates reaching 30% in provincial areas, while residential demand remains robust.

| Market Segment | Current Status | 2025-2026 Outlook |

|---|---|---|

| Manila Residential | 6.5% price growth YoY | Moderate growth expected |

| Rental Yields | 4.5% - 7.2% nationwide | Slight improvement in secondary cities |

| Condominiums | 10.6% price increase Q1 2025 | Steady but slower supply growth |

| Office Spaces | High vacancy rates (up to 30%) | Continued oversupply challenges |

| Mortgage Rates | 5.75%-7.94% currently | Expected to drop to 4.75%-5% |

| New Construction | 8,600 new condo units in Manila | Moderating supply growth |

| Foreign Investment | Improved with 99-year lease options | Continued growth in key cities |

What's the current supply and demand situation for residential and commercial properties in the Philippines?

The Philippines residential property market shows strong demand driven by urbanization and a growing middle class.

Metro Manila is experiencing robust residential demand with approximately 8,600 new condominium units scheduled for completion in 2025, representing a 10% year-on-year increase. New residential building permits increased by 4.8% in the first quarter of 2025, indicating continued construction activity.

The Bay Area has emerged as the dominant residential hub in Metro Manila, attracting significant development interest. Secondary cities across the Philippines are also experiencing strong residential demand, particularly from overseas Filipino workers looking to invest in their home country.

Commercial property sectors face a different situation with clear oversupply challenges. Metro Manila's office stock has reached 8.6 million square meters, creating significant pressure on occupancy rates. Provincial areas are experiencing even more severe imbalances, with some locations reporting vacancy rates as high as 30%.

It's something we develop in our Philippines property pack.

How fast are property prices rising or falling in major cities like Manila, Cebu, and Davao?

Manila leads price growth with overall residential prices rising 6.5% year-on-year in 2025.

The Manila market shows mixed performance across segments. While overall residential prices increased significantly, luxury condominiums actually declined by 0.7% during the same period. The average cost for luxury 3-bedroom condominiums currently stands at PHP 203,360 per square meter.

Cebu demonstrates steady growth with townhouses averaging PHP 12 million and condominiums in technology corridors showing 3-7% annual price appreciation. Small flats of approximately 50 square meters are priced between PHP 4.12-4.28 million, reflecting the city's growing appeal to both residents and investors.

Davao remains the most affordable major city with most properties priced between PHP 2.5-6 million. The city shows stable to slightly rising prices, particularly for mid-market subdivisions that appeal to local buyers and returning overseas Filipino workers.

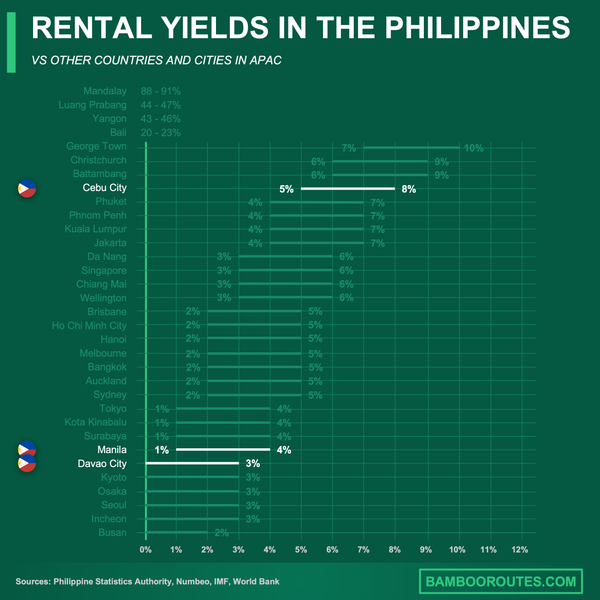

What are the average rental yields right now, and how do they compare across regions?

Rental yields in the Philippines currently range from 4.5% to 7.2% across different regions and property types.

Manila rental yields average 5.12% in the first quarter of 2025, representing a slight decrease from late 2024 levels. The highest yields are typically found in small, centrally located units that appeal to young professionals and students.

Regions with strong overseas Filipino worker demand tend to offer better yield opportunities. Cebu and other secondary cities provide slightly higher yields than Manila due to growing employment opportunities and ongoing infrastructure development projects.

Properties targeting overseas Filipino workers consistently deliver strong rental performance. These investors often seek properties in familiar neighborhoods or near family members, creating steady demand that supports rental income stability across multiple regions.

How is the condominium market performing compared to single-family homes and townhouses?

Condominiums are showing stronger price appreciation but facing supply moderation as developers respond to market conditions.

Condominium prices increased by 10.6% year-on-year in the first quarter of 2025, significantly outpacing other property types. This growth is particularly concentrated in central business districts where land availability is limited and demand from professionals remains strong.

Developers are showing more caution with new condominium supply, especially in central business districts where market saturation concerns are growing. This supply moderation is helping support price stability and preventing oversupply situations that have affected other markets.

Single-family homes and townhouses demonstrate steadier, more moderate growth patterns. These properties are increasingly attractive to both investors and end-users seeking value outside expensive city centers. Suburban and provincial houses offer better affordability and often come with land ownership rights that appeal to Filipino buyers.

What's the vacancy rate for office and retail spaces, and is it trending up or down?

Office vacancy rates remain problematically high, particularly in provincial cities where rates reach up to 30%.

| Location | Office Vacancy Rate | Trend Direction |

|---|---|---|

| Metro Manila | 15-20% | Stable to slightly rising |

| Provincial Cities | Up to 30% | Rising |

| Secondary Business Districts | 20-25% | Stable |

| Prime CBD Locations | 10-15% | Slightly rising |

| New Office Developments | 25-35% | Rising |

Metro Manila's new office supply continues to outpace demand, creating downward pressure on rents. Landlords are increasingly offering incentives such as rent-free periods and fit-out allowances to attract and retain tenants.

The retail sector shows better recovery prospects, fueled by tourism recovery and e-commerce integration strategies. However, retail occupancy levels remain below pre-pandemic levels, though the trend is gradually improving as consumer confidence returns.

How are foreign direct investments and overseas Filipino remittances impacting real estate demand?

Overseas Filipino remittances reached $38.3 billion in 2024, up 3% annually, providing strong support for residential property demand.

These remittances create consistent demand for residential properties as overseas Filipino workers invest in homes for their families or as retirement planning. Projects specifically targeting overseas Filipino workers often see strong sales performance due to this reliable income stream.

Foreign direct investment regulations have been eased with new 99-year lease options for foreigners, increasing demand from international buyers in top cities. This policy change has particularly benefited Manila, Cebu, and other major urban centers where foreign interest was already present.

The combination of remittance flows and improved foreign investment access creates a dual support system for the residential market. International buyers now have more options for long-term property ownership, while overseas Filipino workers continue their traditional role as key property purchasers.

It's something we develop in our Philippines property pack.

Don't lose money on your property in the Philippines

100% of people who have lost money there have spent less than 1 hour researching the market. We have reviewed everything there is to know. Grab our guide now.

What are the current mortgage interest rates, and how easy is it to get financing from banks?

Current mortgage interest rates range from 5.75% to 7.94%, with expectations of decreases to 4.75-5% by the end of 2025.

Banks are most actively granting residential loans in the National Capital Region, Calabarzon, and Central Luzon, where property values and borrower profiles are considered most favorable. The anticipated rate decreases should improve affordability and stimulate additional demand from local buyers.

Financing remains more accessible for Filipino citizens and residents compared to foreign buyers. Most banks require foreign buyers to establish local business entities or opt for long-term lease arrangements rather than direct ownership financing.

The improving interest rate environment is expected to support increased buying activity, particularly among middle-class Filipinos who have been waiting for more favorable financing conditions. Lower rates will also benefit property investors seeking to leverage their purchases for better returns.

How much new construction is in the pipeline, and will it add to oversupply or meet growing demand?

Metro Manila has 8,600 new condominium units scheduled for completion in 2025, with total condominium stock projected to reach 179,820 units by 2027.

Residential construction activity is climbing but at a more measured pace than previous years. Annual completions are moderating, suggesting less risk of oversupply for condominiums as developers respond more carefully to market signals.

The residential pipeline appears well-aligned with demand, particularly given continued urbanization and overseas Filipino worker investment. Most new residential projects are targeting middle-income buyers rather than the luxury segment, which shows better absorption rates.

Office construction continues to exceed demand, contributing to elevated vacancy rates across the commercial sector. This oversupply situation is expected to persist as buildings completed in 2024 and 2025 seek tenants in an already saturated market.

How are infrastructure projects like new airports, railways, and highways affecting property hotspots?

Major infrastructure developments including airport expansions, rail networks, and new highways are creating new property investment opportunities.

1. **Luzon Spine Expressway Network** - Connecting northern and southern regions, creating development corridors2. **Metro Manila Rail Transit Extensions** - Improving connectivity to suburban areas and boosting property values3. **Clark International Airport Expansion** - Establishing new commercial and residential hubs4. **Cebu Bus Rapid Transit** - Enhancing property accessibility in the Visayas region 5. **Davao Public Transport Modernization** - Supporting property development in Mindanao's economic centerThese infrastructure projects are making provinces and growth areas increasingly attractive for both residential and logistics investments. Properties near new transport corridors are experiencing increased investor interest and price appreciation.

The infrastructure improvements are particularly beneficial for overseas Filipino workers who can now access more areas while maintaining connectivity to urban employment centers. This expanded accessibility is driving residential demand in previously less accessible regions.

We did some research and made this infographic to help you quickly compare rental yields of the major cities in the Philippines versus those in neighboring countries. It provides a clear view of how this country positions itself as a real estate investment destination, which might interest you if you're planning to invest there.

What are analysts predicting for the property market over the next 12 to 24 months?

Analysts predict steady growth for residential segments while commercial properties face continued challenges.

Residential prices are expected to rise moderately as demand remains supported by improving affordability through lower interest rates and continued migration to urban areas. The pace of growth may moderate from current levels as the market matures.

Commercial property, especially office space, faces ongoing risks due to oversupply and evolving work models including hybrid arrangements and business process outsourcing expansion. Recovery in this sector is expected to be slower and more selective.

Rental yields may improve slightly as new demand emerges in secondary markets where infrastructure improvements create opportunities. The combination of lower interest rates and infrastructure development should support investment activity across multiple regions.

How are government housing policies, taxes, and foreign ownership rules shaping investment opportunities?

Government policies remain generally stable with transaction costs of 8-10% and recent easing of foreign property investment rules.

Recent policy changes allow foreigners to access 99-year lease options, providing more security for international investors while maintaining restrictions on outright land ownership. This compromise approach helps attract foreign capital without completely opening land ownership to non-Filipinos.

Foreign investors must still navigate restrictions on direct land ownership, typically investing through condominium purchases within specific developer projects or establishing local business entities. These requirements create additional complexity but remain manageable for serious investors.

The government's housing policies continue to support middle-income segments through various financing programs. These initiatives help maintain steady domestic demand that provides stability for the overall residential market.

It's something we develop in our Philippines property pack.

What risks could derail the market outlook, such as inflation, political changes, or global economic slowdowns?

Several risks could impact the Philippines property market outlook over the coming years.

| Risk Factor | Impact Level | Mitigation Factors |

|---|---|---|

| Worsening Inflation | High | Central bank monetary policy |

| Global Economic Instability | Medium | Domestic demand resilience |

| Political Changes | Medium | Stable institutional framework |

| Commercial Oversupply | High | Limited to specific sectors |

| Interest Rate Volatility | Medium | Expected rate decreases |

| Remittance Flow Disruption | High | Diversified OFW destinations |

Persistent oversupply in select commercial segments poses immediate risks to office and retail property performance. This situation could worsen if economic conditions reduce business expansion and hiring.

The residential market benefits from some protection through overseas Filipino remittances and local home buyer demand. These factors provide a buffer against external economic shocks that might otherwise severely impact property demand.

Conclusion

This article is for informational purposes only and should not be considered financial advice. Readers are advised to consult with a qualified professional before making any investment decisions. We do not assume any liability for actions taken based on the information provided.

The Philippines property market in 2025 demonstrates resilience with strong residential fundamentals supported by overseas remittances and infrastructure development.

While commercial sectors face oversupply challenges, residential properties offer steady growth opportunities for both investors and owner-occupiers seeking exposure to one of Southeast Asia's most dynamic economies.

Sources

- Inquirer Business - Philippines Real Estate Rally

- BambooRoutes - Philippines 5-Year Real Estate Forecast

- Santos Knight Frank - Office Market Oversupply Analysis

- Vista Land - Housing Market Outlook

- Global Property Guide - Philippines Price History

- Inquirer Business - Real Estate Growth Dynamics

- Philippine Star - Property Price Growth Report

- Manila Magazine - Real Estate Resilience